The Internet of Things in the banking market is paving the way to digitizing the overall services that would require bank specialists’ intervention. It’s anticipated to grow to $134,014.3 mln by 2030 with a CAGR of 11.9% (from 2024 to 2030), as presented by Grand View Research.

When interacting with IoT in banking services, businesses can benefit from contactless payments and regulatory compliance, while clients can receive personalized service, secure fund operations. In this article, we’ll describe what benefits IoT brings to banking along with the challenges.

-

IoT contributes to smart banking through service automation using devices to generate a personalized and secure user experience.

-

Integrating smart ATMs, biometric scanners, and wearable technology can optimize banking operations by reducing operational costs.

-

Efficient IoT adoption requires strong strategic planning, a robust focus on security, and the selection of the right development partner to navigate development complexities.

Examples of Connected Devices Used in Banks

IoT in banking goes beyond a single embedded device to provide client services. It’s about a chain of technologies that enhance the accessibility of bank-relevant services.

Smart ATMs

Unlike traditional banks that enable limited cash-associated capabilities, smart ATMs focus on customer-centric self-service actions.

-

Biometric Access Capabilities: smart ATMs integrate biometric authentication that enable users to withdraw funds without using a physical card. This verification method strengthens identity checks, helps prevent fraud, can trigger alerts in case of suspicious activity, and improve reliability of the banking institution.

-

Touchscreens: smart ATMs extend the capabilities of their traditional counterparts by enabling clients to authorize documents digitally. For instance, through digital signatures or biometric authentication. When received, the banking institutions can consider these documents legally valid if they comply with digital signature regulations.

Wearable Banking

Wearable banking refers to digital devices such as smartwatches or smart bracelets that allow users to perform financial operations. This IoT innovation enhances payment accessibility and broadens banking services to meet more diverse customer needs.

Smartphones

Last but not least, smartphones are not new to banking services. Nevertheless, they significantly streamline banking operations, accessible worldwide. Payments, online top-up options, real-time fraud detection, and location-based promotion are those functions that enable traditional banking to foster personalized services through their mobile applications.

Key Benefits of IoT in the Banking Sector

Despite the above-mentioned cases of IoT’s support of bank-client relationships, it’s essential to shed light on the encompassing spectrum of benefits of IoT in banking.

Delivering Personalized Services via Behavior Tracking

IoT supports the delivery of personalized banking services by gathering clients’ real-time information from the connected devices and analyzing their behavior. This data can be assessed to provide client-centric recommendations that address user’s specific needs. How IoT does it:

-

Data Collection

IoT devices including smartphones, wearable bracelets, smart home appliances can constantly generate user’s data on their location, activities, and identify client-specific activity patterns. When using the application, the user provides the bank with permission to process their personal data. Then, the bank’s application can access their data to build a detailed image of their life, or to create a so-called individualized ICP.

-

Behavioral Analysis

Then, the application analyzes the collected data through AI and machine learning algorithms to evaluate current needs and predict future needs. A bank can learn that a client is saving for a specific goal or favor certain activities.

-

Personalized Recommendations

Finally, after collecting and analyzing the essential details, banks can move beyond the standard credit card offers and send notifications with a unique offering. For instance, the client is fond of traveling. Just before they leave, the application analyzes their geolocation and sends push notifications with a travel insurance offer.

Personalized recommendations go far beyond simple automated advice. In advanced digital banking applications, users who want to save more can be interested in AI-driven insights. By analyzing spending patterns and transaction history, AI can provide practical strategies for savings including which category of spending to cut back on.

Automating Operations for Cost Efficiency

IoT devices are embedded in banking ecosystems that enable streamlining banking operations and provide insights on the equipment conditions.

Smart Branches

Smart branches represent the concept that leveraging IoT in the traditional banking institutions can significantly streamline their operations. The IoT-powered sensors can track foot traffic and customer wait times to optimize workforce allocation and optimize banking operations.

Another case of smart branches IoT represents providing client-centric services based on real-time analytics. For instance, by analyzing client banking history, digital kiosks can generate advice applicable to the client’s specific case.

Asset & Equipment Management

Banks can leverage IoT to track and monitor valuable assets and equipment promoting ATM modernization. Vehicles with integrated sensors for cash transportation can provide data on the real-time location. The banking institution can check the overall maintenance status for their smart ATMs. Smart ATMs can include technology for remote management and predictive analytics on potential issues before they emerge. This proactive approach gives banks a strategic advantage by reducing downtime, improving security, and ensuring smoother operations.

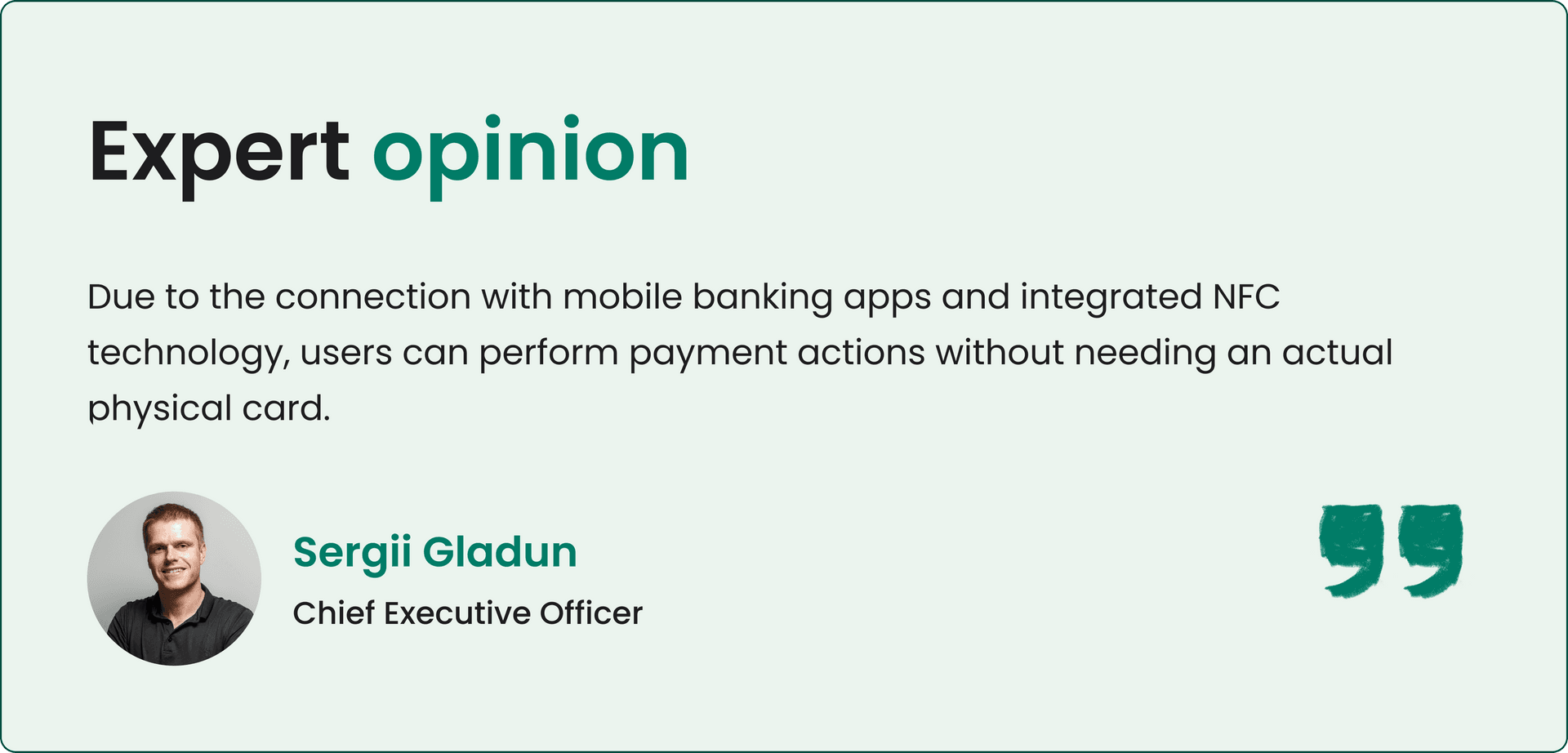

Enabling Contactless and Secure Transactions

IoT fosters contactless transactions by applying wireless communication protocols and advanced security measures. Payment technology is integrated directly into smart devices. This approach boosts transaction speed and brings more protection by minimizing the need to use a physical card.

Wireless Connectivity

Wireless communication technology enables payment without using a physical card by allowing devices such as smartphones or wearable technology to integrate directly with the POS terminals. The most common examples include:

-

NFC (Near-Field Communication): users can make secure payments by holding a smartphone or wearable near the point-of-sale terminal. The payment application uses NFC to transfer encrypted and tokenized data, guaranteeing security during the transaction.

-

BLE (Bluetooth Low Energy): this technology can be used in location-based payment systems, where beacons detect when a client steps into a specific location. Then, the payment occurs automatically without any need for device proximity to the POS.

Enhanced Security Measures

IoT integrates with already existing security systems by adding an extra security layer of protection. Here’s how IoT enhances security:

-

Tokenization

The device replaces card-sensitive information with a unique one-time token. So, in the case of any interception, the token cannot be reversed to obtain the original card-specific information.

-

Real-Time Fraud Detection

IoT is about continuous monitoring of users’ behavior and location. Combined with real-time analytics, this provides banks with the following strategic advantages. They can detect anomalies in behavior such as frequent payment procedures, atypically large transactions, or spot activities performed from a sanctioned country. These insights help financial institutions block suspicious transactions and maintain security.

Driving Continuous Innovation in Banking Industry

By integrating IoT-powered software, banks can automate the performance of repetitive tasks, boost the speed of payment initiation, and simplify account management. These reduce the manual workload, enabling workers to focus on high-value activities including customer service and strategic decision-making.

As an outcome, the banking institutions can complete more tasks in less time. The automated payment systems can be accessible 24/7 anywhere around the world. Automated tools can facilitate regulatory compliance through the prompt and accurate delivery of required data.

IoT can support the automation of loan-related processes by supplying real-time data on collateral, such as connected vehicles or equipment. This enables lenders to monitor asset condition and usage remotely, reducing the need for physical inspections at bank branches.

Learn how to create an effective loan application.

Learn how to create an effective loan application.

Top Use Cases of IoT in Banking

IoT streamlines banking operations by powering its strategic capabilities in service provision. This leads to the extensive client coverage, improved accessibility, optimized security, and regulatory compliance.

IoT in Insurance: Usage-Based Policies

Historically, insurers primarily relied on past data to evaluate risks and set insurance premiums. In the case of a vehicle, factors such as type, location, driver’s age, mileage represented the primary source of information taken into account to generate a fair premium.

IoT streamlines data processing by collecting real-time information from the client’s connected device. Sensors integrated into the connected cars can detect, record, and transmit data such as driver’s behavior, driving speed, mileage, braking patterns directly to the insurance companies for usage-based insurance (UBI). While linked specifically to the insurance companies, banks can leverage those data indirectly for vehicle loan risk assessment or partnerships with insurers.

AI algorithms analyze IoT-collected data to assess the safety of each trip and calculate risk levels. This usage-based model helps identify high-risk drivers to set more accurate insurance premiums. While still centered around insurers, the collaboration with them enables banks to leverage IoT-driven risk insights for insurance cross-selling, especially for the high-risk drivers.

Voice Assistants and Chatbots for Banking

A voice bot is an AI-powered assistant deployed in the banking application to interact with clients by interpreting the voice commands. When the user speaks, the bot processes requests by implementing natural language processing and Speech-to-Text (STT) to recognize speech patterns. Once the command is interpreted and understood, the bot can provide a response in either text or audio format.

Voice bots streamline banking operations by presenting alternative and functional ways to process customer requests. By integrating with smart home devices or wearables that support speech recognition, the user can check their balance, transaction history, and in some cases, process payments. Thanks to their cloud-based nature, voice bots operate 24/7 and can be accessed globally, offering round-the-clock customer support.

A chatbot represents an AI and NLP-powered software program that simulates a human-like conversation with clients on their needs all within the messaging interface. Chatbots can provide services, including:

-

Transaction Assistance: chatbots can assist clients in performing basic financial tasks such as transferring funds between accounts and paying bills. Usually, it can require OTP and PIN.

-

Customer Support: chatbots respond to the clients’ basic questions, including ‘What’s my account balance?’

-

Personalized Advice: advanced chatbots can apply AI algorithms to analyze user behaviors and tailor personalized advice on spending patterns and saving strategies.

Blockchain Smart Contracts + IoT Devices

While traditional banking institutions rely heavily on the centralized systems that process and collect data, blockchain provides significant benefits even for this industry. Transaction settlement, permissioned data sharing are some of the future trends in blockchain technology that affect a bank's performance as an enterprise. Blockchain and IoT function as a cohesive organism that complement each other’s operations to streamline banking operations.

-

Blockchain is a decentralized, distributed, and immutable digital ledger that through the means of cryptography encrypts the recorded information on the blocks that are linked chronologically.

-

Blockchain records IoT-collected data, in an immutable and transparent ledger, ensuring it cannot be changed while stored. Then, smart contracts take the lead when it comes to executing the specific action.

-

The key is that smart contracts will be triggered and automatically execute the action only if the predefined conditions are met. Custom blockchain smart contract development might be essential for building a high-complexity bespoke IoT project, especially for private and permissioned blockchain for bank’s operability with partners.

Automated Payments

For instance, the user leaves a parking lot. IoT sensors in the vehicle or smart parking garage record the data on the client's behavior. Then, the data triggers smart contracts on the blockchain to automatically withdraw parking fees from the client’s digital wallet. The whole process is secure, automated, and doesn’t even require users’ activity through their mobile banking application.

Trade Finance

IoT and blockchain improve shipment processing, stimulating fair payment for services. Here's how banking and supply chain intertwine. An IoT device is placed in the container to track the shipment’s location and temperature. This data is then recorded and stored on the distributed ledger.

A smart contract that holds payment for the goods is programmed and will automatically release funds when the client receives the parcel within the maintained temperature. That’s how IoT and blockchain benefit both industries by ensuring payments aren’t released if the predefined container measures were not met. Additionally, IoT resolves unfair disputes on the product quality by presenting evidence on its conditions, preventing banks from refunds.

Gain insights into the applicability of blockchain in banking.

Gain insights into the applicability of blockchain in banking.

IoT and Regulatory Standardization

Regulatory compliance is mandatory for both traditional banking institutions and their digital applications. Banks are obliged to guarantee and maintain security, financial stability of the cardholder’s sensitive data at rest and in transit to prevent financial crimes. Additionally, regular audits are required to demonstrate reliability and resilience of a bank's digital infrastructure.

KYC/AML Compliance

IoT can capture client’s biometrical and geolocational data through smartphones or wearables in order to intensify customer identity verification. Regulators require strict compliance with Anti-Money Laundering and Know Your Customer initiatives to prevent money laundering financial manipulation. Dynamic behavioral data and biometrics can strengthen a bank's regulatory compliance and overall security layer than focusing on static information alone.

IoT and Standardization of Data for Audits

IoT devices generate data in machine-readable formats that, if integrated with blockchain systems to be stored immutably and securely. While relevant, this data can be structured or mapped to align with financial messaging standards, such as ISO 20022, supporting interoperability and compliance. If a permissioned blockchain is applied, smart contracts can automatically validate predefined conditions linked to IoT data, while regulators can be granted real-time access to enhance compliance oversight.

Challenges and Risks of IoT Adoption in Finance

Regardless of the plethora of benefits, IoT adoption still presents a spectrum of challenges needed to be considered when integrated into the banking systems.

Privacy Compliance

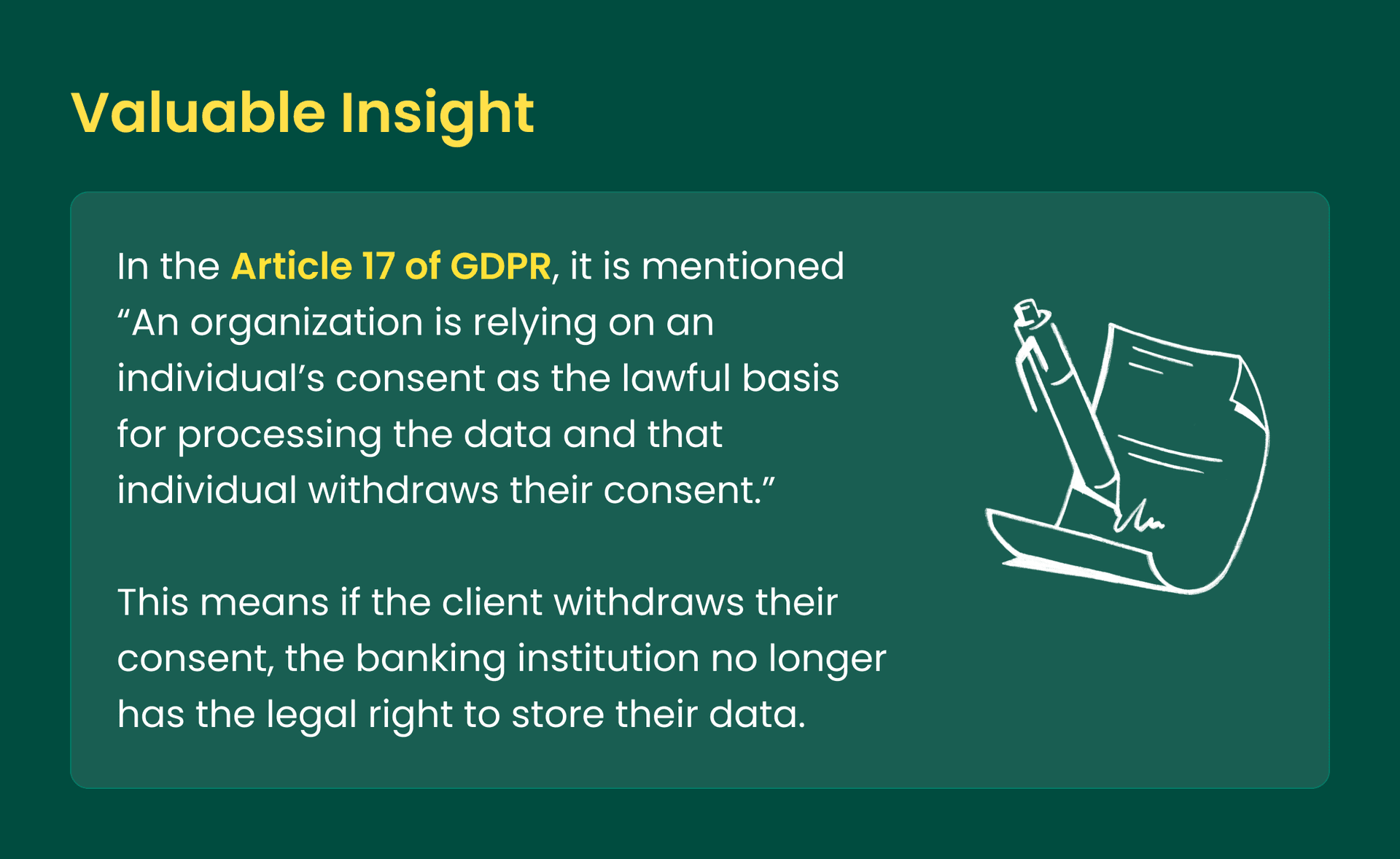

Despite regulatory standardization, data privacy & compliance remains one of the most critical issues for IoT adoption based on the data removal from the system. Banking institutions are obliged to comply with General Data Protection Regulation (GDPR), a European set of standards requiring financial institutions to make clients’ data storage and processing clear and transparent.

One of GDPR rules is called ‘The Right to Be Forgotten,’ which implies that if the client requests data deletion, all stored info has to be removed. This is problematic for IoT in banking, because the data is collected from multiple sources: smart ATM, wearables, mobile banking app and transferred to the different channels: local servers, cloud platforms, and third-party analytics services. This causes data fragmentation, as the banking institution has to erase pieces of information from all the systems.

Source: GDPR.

Device Authentication and Network Visibility

IoT devices lack robust built-in security characteristics, which is challenging for the banking system. It relates specifically to the smart IoT-powered devices within the banking institution systems, like smart air conditioners or smart branch sensors. Once unauthenticated or compromised, the device turns into a gateway for the attackers to manipulate the overall banking network from the inside. This needs robust consideration since having access to the internal system, the hackers can observe the connectivity between IoT devices within the banking institutions that undermine their transparency.

Security Risks from Uncertified Hardware

The IoT market is fragmented, which can present devices with a low certification level or those that embed weak security measures. Hardcoded passwords, unpatchable vulnerabilities, insecure communication protocols can be easily exploited by hackers, leading to compromising the whole corporate network. As a result, cybercriminals can launch a DDoS attack to gain access to sensitive data.

Integration Complexity and Legacy System Barriers

A vast number of traditional banks operate via old-fashioned legacy systems. So, when it comes to IoT integration, there might be a conflict in compatibility affecting the overall performance. IoT requires new technologies for the overall overhaul of the existing infrastructure. Banking institutions have to invest in the development of custom integration layers because of the lack of standardized protocols for IoT devices. This provokes project delays and increases risks within their performance.

How to Start Your IoT Banking Project

The overall start of the IoT banking project refrains from traditional requirements for mobile banking development and simple IoT device purchase. It’s about strategic and proactive planning on what deliverables to implement, strategies to integrate them with cloud and legacy systems to bring maximized efficiency to problem-solving.

Goal-Definition

The goal must be clearly defined and be narrow-specific, since the IoTdevice is an additional tool to fuel the performance of the banking institution. For instance, an IoT sensor within a smart ATM to optimize the maintenance process.

In-Depth Research

The next point is to identify the target audience and provide competitor analysis on how they integrate IoT. Additionally, the banking representatives have to analyze the overall IoT market to define strong and weak IoT solutions to detect what devices will cover the needs at the maximum.

A Solution Architecture Plan

Then, it’s time to craft a solution architecture plan, or, in other words, the ways to promote connectivity and accurate performance between IoT devices, cloud platforms, and user-facing applications.

Dive into the project discovery stage and examine its key components.

Dive into the project discovery stage and examine its key components.

Considerations Before Implementation

Just before starting the IoT development project, it’s essential to keep in mind the aspects of scalability, security, data privacy, and integration with the banking institution's legacy system.

Scalability

The scalability for IoT projects is about maintaining the underlying system’s infrastructure so that it can handle a growing number of devices and expanding flow of sensitive data without performance compromising. This implies the selection of the strategically functional tech stack including cloud service that would add more storage and processing power by applying databases built for large-scale data influx.

Security and Data Privacy

Emphasis on ‘Zero Trust’ architecture, robust IoT device authentication measures, and data encryption channels are principal measures that should be undertaken to decrease IoT vulnerability to the cyberattacks. Additionally, legal considerations on regulatory compliance may be beneficial to ensure the overall sensitive data protection, as well as conduct and submit regular audits.

Integration with Legacy Systems

Another element to keep in mind, is to implement an IoT solution so that it could integrate with the banking legacy system without compromising its performance. Some of the minor aspects to include are API gateways and message brokers.

API gateways will receive data from the IoT devices and transform it into the format the banking core system could be able to manage. The message broker platforms serve as intermediary in communication between the IoT and the bank's legacy system. This so-called middleman delivers data by maintaining an asynchronous and reliable information flow.

Choosing the Right IoT Development Partner

Selecting the right development partner is critical for an efficient IoT project development. The partner should be experienced in both financial technologies and present a proficiency in dealing with security audits, penetration testing, and other safety measures.

Financial and IoT Experts

The partner has to present a decent level of understanding in tech complexities of integration and management of physical devices that include:

-

Hardware: selecting the right sensors and gateways and streamlining the power consumption to make the devices last longer.

-

Software: capabilities to build secure firmware to handle massive data volume flow, set, and integrate seamless communication between the IoT device and the cloud.

-

Security: this involves a partner's knowledge and ability to implement security measures, like secure boot processes, encrypted data channels, and robust authentication to prevent the IoT device against cyber vulnerability.

When speaking about financial expertise, the partner must understand rigid banking regulations, such as KYC and AML to meet global security standards, such as PCI DSS and GDPR.

Additionally, the partner has to ensure adherence to the full project development lifecycle from hardware selection to cloud integration, which will reduce the risk of communication issues and deliver a full-fledged solution.

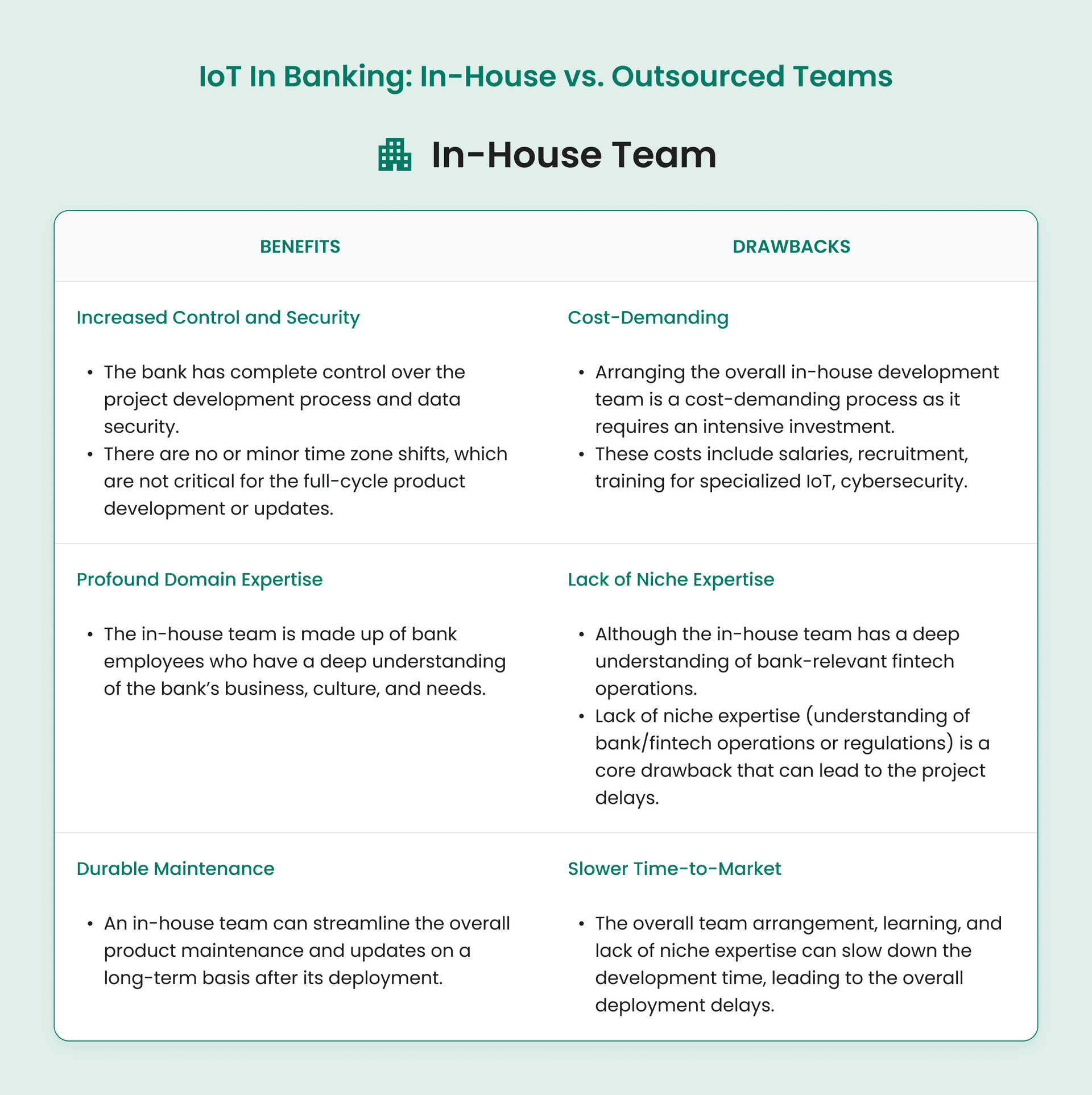

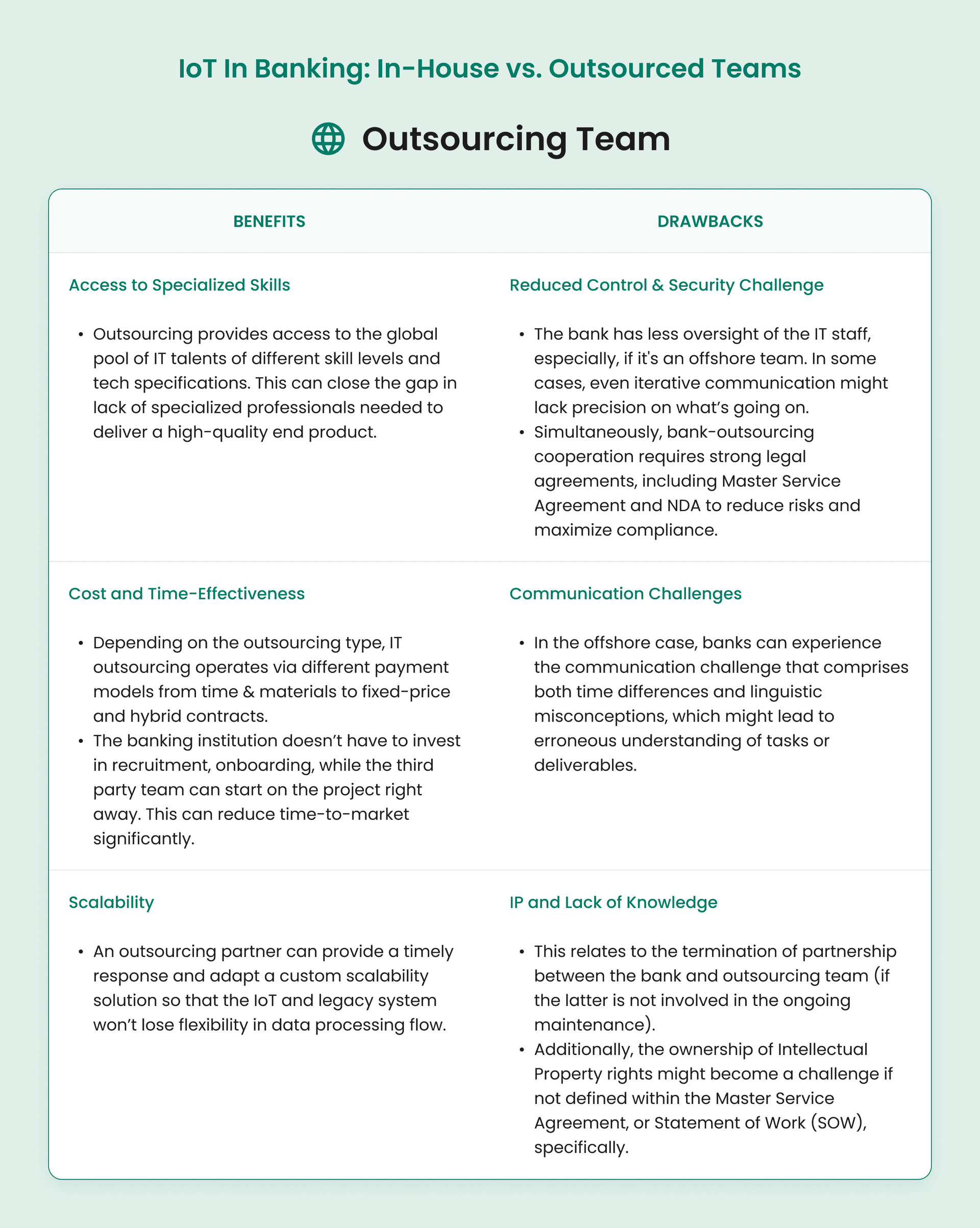

In-House Team vs. Outsourcing Team

Additionally, the right development partner is not only about the practical skillset, but about the overall team who will directly work in the bank or a third-party outsourcing provider, who’ll deliver the required services.

MVP-First Strategy for IoT in Finance

An MVP for the IoT banking project does not imply presenting a fully-fledged digital solution but rather the tiniest possible version to validate the core idea and collect feedback.

Testing Main Hypothesis

For instance, the banking representatives aim to check the effectiveness of a biometric physical scanner at a single bank branch to reduce transaction time by 35 seconds. The goal should be narrowly specialized to gather measurable feedback afterward.

Then, it’s time to create a small pilot group for testing purposes only. This scanner is integrated within 2-3 smart ATM branches to collect data on its functionality. The arranged professionals whether in-house or outsourcing team will have to build minimal backend logic to connect to the scanner to authenticate identity. Additionally, the backend should cover logging a simple data point (e.g., the speed of identity verification).

Collect & Analyze Real-World Feedback

After a few weeks, the bank representatives should analyze the collected data on the average time of user verification and whether the biometric authenticated scanner manages to reduce the transaction time. Additionally, it evaluates clients’ impressions, frustrations, pain points, and drop-offs.

Summary

IoT streamlines the operations of traditional banking by boosting the digitized service provision. Smart ATMs, smart branches, biometric scanners, all the facilities enable competitors to benefit from smart banking by boosting their performance speed, ensuring personalized services, without compromising the performance of the legacy systems. Hence, strategic goal definition, in-depth research, MVP-first approach can pave the way to smart banking as IoT adds to the strategic value of traditional institutions’ operations.