Digital banking is a powerful tool that serves to reshape and redefine traditional banking and competition. Banks should know the problems and hazards associated with this transformation to survive. Cybersecurity is the basis of digital banking trust and is the most needed tool to fight against cyber threats and develop the best fraud prevention strategies. The industry is simultaneously tackling unimaginable opportunities and impenetrable barriers, with success depending on innovation, consumer-oriented strategies, and information security. Agilie's team prepared the list of cyber threats for digital banks, prevention plans, as well as challenges to stay aware and run a successful digital bank.

-

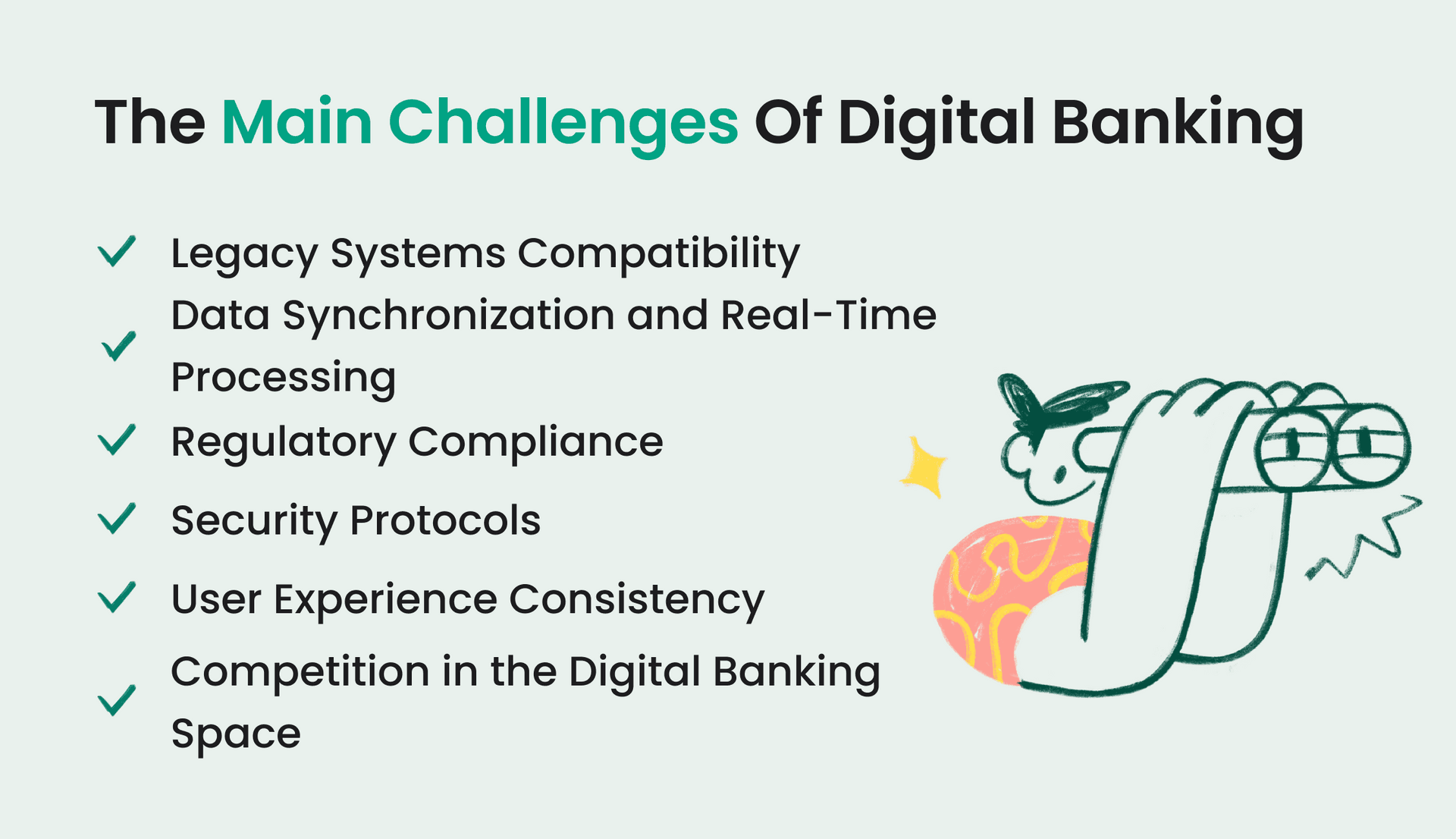

Digital banking has many challenges, such as cybersecurity, technical advancements, compliance, interoperability, and intense competitiveness.

-

Digital banks have to fight against phishing, malware, ransomware, data breaches, API security vulnerabilities, and the poor security of third-party services to keep their clients’ private information intact and to protect their reputations.

-

Digital banks have to innovate in terms of user experience and efficiencies in the operational tasks to get through the complex regulatory landscape and in synchronization of data and real-time processing without interrupting the standard operations.

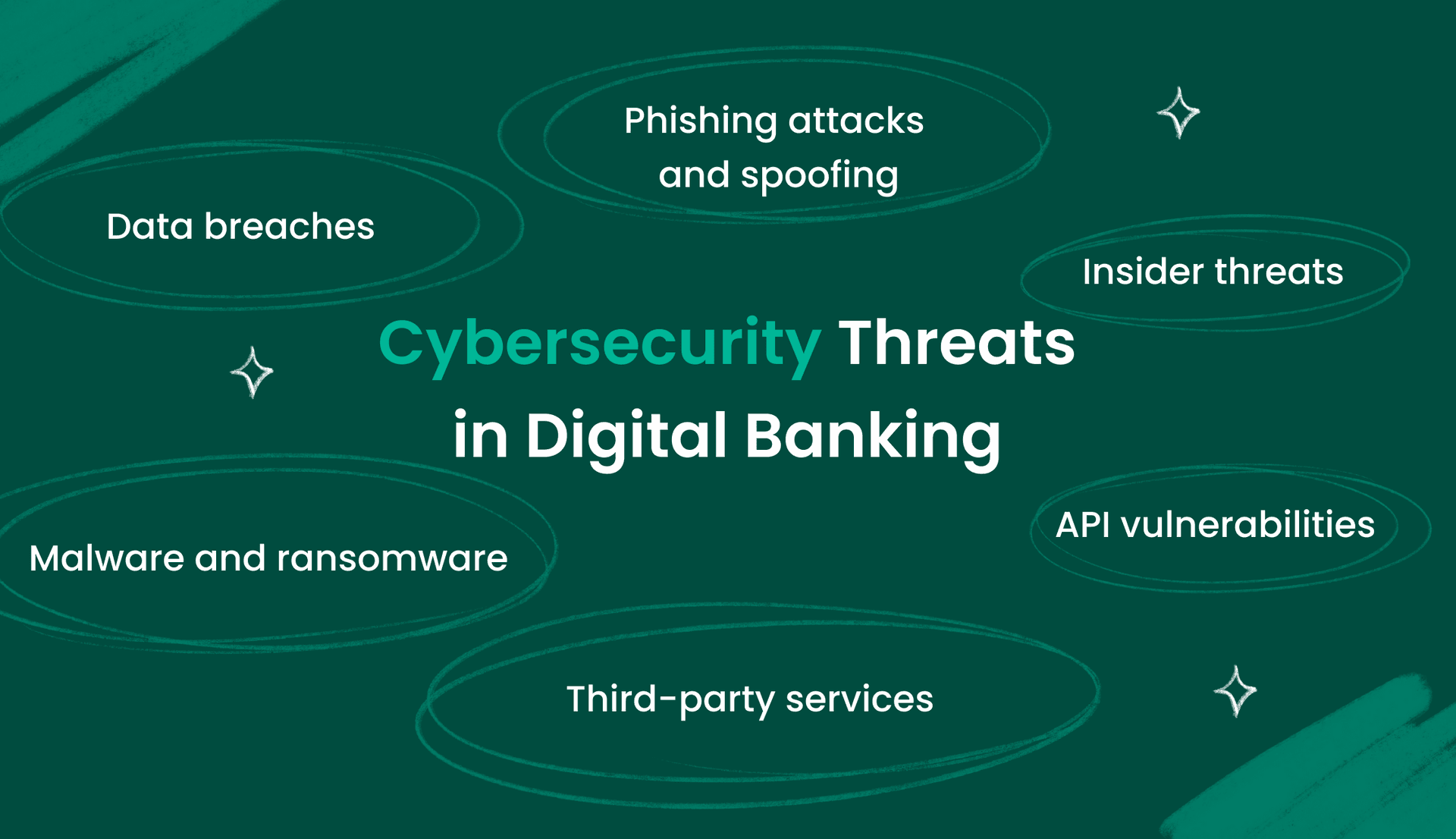

Cybersecurity and Fraud Risks and Prevention in Digital Banking

Safe digital banking is critically dependent on cybersecurity and fraud prevention. Let’s look into cyber threats and find out how to prevent them.

1. Phishing Attacks and Spoofing

Cybercriminals apply phishing as a form of the widely used trick aimed at social engineering to get personal and financial information. Fraudsters pretend to be the regular communication channels of financial organizations, directing unsuspecting customers to the websites where they enter their sensitive data. Digital banks make this threat impossible with the help of advanced email spam filtering, multi-factor authentication, and the continuous promotion of phishing awareness and readiness among consumers.

Spoofing, which is disguising, for example, as a bank and misleading users or systems, is another form of enormous threat. Spoofing can be a part of a phishing attack. It might simulate email addresses, phone numbers, or websites. Banks counter forgeries by implementing strong authentication tools such as SPF (Sender Policy Framework) and DKIM (DomainKeys Identified Mail), which are security protocols that ensure the legitimate use of communication channels.

2. Malware and Ransomware

These categories of threats incorporate hackers putting dangerous software to pierce banking systems, encrypt crucial data, and demand ransom. Digital banks counter the risks of malware using comprehensive tools, frequent software updates, and robust data backup processes, which involve restoring information without giving in to ransom demands.

3. Data Breaches and Insider Threats

Data breach is one of the most common cyber issues in the digital banking sector. Banks use sophisticated encryption tools, data anonymization techniques, and secure storage to reduce the risk of data breaches. Regular data security assessment and compliance with international data protection regulations are keys to data protection and customer confidence.

Insider threats, including the ones arising from negligence or deliberate attempts to obtain data, can cause disastrous data breaches. Banks attain this purpose by the use of sophisticated and filtered access controls, intensified employee checks, and rigorous monitoring of unusual activities.

4. API Security Vulnerabilities

APIs facilitate the performance and integration of virtual banking services, yet they are vulnerable to security breaches without proper safeguarding. Proper mechanisms against API weaknesses should involve regular information security inspections, deploying API gateways, and also enforcing strict authentication principles that grant only accredited entities access to APIs.

5. Third-Party Services

Many digital banks outsource services to other companies operating, which may result in service disruptions or security threats. Banks can have a strong security system in contrast to third-party services. That's why thorough inspection of third parties, consistent monitoring of their actions, and making security protocols an integral component of all third-party collaboration agreements are crucial in limiting the possibility of security gaps that could creep in through external partnerships.

Find out how to develop a secure and successful neobank in 2024.

Find out how to develop a secure and successful neobank in 2024.

Most Common Digital Banking Challenges

Financial institutions are going through a rapid digital transformation and the accomplishment of synchronized interaction with the existing banking systems is demanding, and involves complex technical and regulatory issues.

1. Legacy Systems Compatibility

Traditional banks implement outdated systems through programming languages and designs which are often incompatible with current digital banking technologies. The challenge is about how we can bring about secure, resilient technologies together with a user-friendly and interactive interface.

2. Data Synchronization and Real-Time Processing

Data synchronization and real-time processing among banks constitute another challenge. They are important for the customers as they give access to their financial information anywhere. A robust and scalable data processing system can have lots of transactions processing at the same time and synchronizing among its different parts. Technology like microservices architecture and event-driven data management can facilitate this by providing efficient messaging and simultaneous updates across platforms.

3. Regulatory Compliance

Interoperability also poses the question of dealing with regulatory issues, which can differ from one jurisdiction to another. Digital banks must be sure that the integration satisfies all necessary regulatory requirements, for instance, data privacy laws, AML directives, and banking secrecy acts.

Compliance becomes especially complicated if the digital banks need to be integrated with systems from other countries. Banks are required to invest in advanced RegTech solutions which will enable them to comply with different regulatory environments and embed secure cross-border data flows in all local compliance requirements.

4. Security Protocols

The integration of different banking systems cannot lead to the weakening of platform security. Every system has its security procedures, and their alignment will be a complicated task. Building an architecture for security requires incorporating the good practices of each system and other features that will cover the functional gaps caused during the integration. Authenticating by the OAuth procedure and end-to-end encryption should be the top priority of integrity and user convenience.

5. User Experience Consistency

Banks encounter the challenges of ensuring a consistent user experience when they deploy both old and new systems. Improper integration of different systems often leads to disjointed customer intervention when they are combined. Utilization of user experience (UX) principles uniformly throughout all the platforms will help in providing customers with a consistently smooth experience regardless of where they interact with the brand.

Learn more about neobanking trends in 2024.

Learn more about neobanking trends in 2024.

Competition in the Digital Banking Space

Competition in the digital banking industry is fierce, as more fintech companies enter the market and traditional banks investigate how to enrich their digital offerings. The increased competition can result in lower profits and a loss of market share for the traditional banks that fail to adapt fast and offer innovative and user-friendly digital banking services.

Since competing in the digital banking space is dynamic and multi-directional, new players must offer exceptional value to survive the initial market entry. Success in this sector is dictated by the ability to match or exceed the features provided by industry pioneers. For a deep-dive into the current competitive landscape, it is useful to analyze the top 5 alternatives to Monzo mobile banking app, as these platforms represent the gold standard in real-time payments and active fraud prevention. Evaluating these benchmarks allows developers to identify the specific innovation gaps - such as AI-driven wealth management or frictionless cross-border transfers—that are required to capture market share from dominant fintech incumbents.

Learn more about Agilie’s cases and introduce our diverse innovative solutions.

Learn more about Agilie’s cases and introduce our diverse innovative solutions.

Digital banks make a huge push into the user experience (UX) and user interface (UI) design offerings to attract and retain users. It encompasses account opening convenience, transaction simplicity, and the ability to get financial advice through digital channels, allowing being in the market's leading class.

Digital banks with their flexible approaches can enter new markets very quickly and skip traditional banks, having the advantage of updating to changing regulatory environments. They propose many different financial services and customize them for particular communities. The creation of strategic partnerships between fintech enterprises, software development companies, traditional banks, and non-financial entities is a key factor in multiplying gains. Digital banks provide a cost advantage by operating with fewer operational expenses due to the non-maintenance of physical branch offices and providing services at competitive prices.

Discover our fintech software development services to create a skyrocketing neobank.

Discover our fintech software development services to create a skyrocketing neobank.

Conclusion

The digital banking setting is developing through technology, risks and challenges, requisite regulation, and a high level of market competition. The expansion and transformation of this industry bring to view an urgent need for strong digital solutions that consider security, improve the quality of the client experience, and assist in smooth and reliable integration with the existing tools. Embracing risks, challenges, and opportunities is a must-have element for any bank that wants to sustain success in the digital era.

Getting through this complex landscape requires the knowledge of how to create a mobile banking app and master financial technologies and their advancement, implementation, and use. Agilie, a fintech software development company, is an expert in cybersecurity, compliance, customer experience, and innovative technology integration. We can customize unique offerings to revolutionize digital banking, ensuring security, reliability, and efficiency. Partnering with Agilie will grant financial institutions a chance to surpass their competitors, turning their concerns into a springboard to growth and success.