Blockchain is one of the pillars of digital transformation worldwide due to the simplification of transaction processing, fraud detection, etc. But have you wondered how banking and blockchain are intertwined? As we know, banks are financial institutions with centralized control, which brings some skepticism about the opportunities a distributed ledger can bring to it.

Blockchain, on the contrary, ensures decentralized peer-to-peer transaction processing by being a time- and cost-effective alternative to traditional cross-border banking payment. In this article, we explore what is blockchain technology in banking and its benefits, challenges, and opportunities.

-

Blockchain transforms the banking industry due to a permissioned network, cryptographic protection, and permanent records.

-

The distributed ledger technology can significantly reduce the time for cross-border payment, enhance AML and KYC compliance, and improve syndicated loan processing.

-

The future of blockchain in banking technology is about considering operations with Central Bank Digital Currencies and crypto, as well as AI integrations.

Source: The Business Research Company

How Blockchain Works in Banking

Blockchain technology in the banking sector improves the overall institutions’ service provision because the transactions are recorded on the decentralized computer network. There are the following principles of blockchain the banks benefit from:

-

Decentralization

The core idea of blockchain decentralization is that no single entity can have full control over the transactions, and multiple parties can validate them.

The banking industry refrains from the aforementioned essence of decentralization by applying permissioned blockchain. Permissioned blockchain in banking is partially decentralized as only authorized agents can validate financial transactions or data transmission, and the trusted network of validators has control over these actions, not a single bank.

One of the use cases of blockchain in banking is JPMorgan’s initiative to utilize Liink, a permissioned blockchain, to economize time and enhance the security of information exchange, like verifying account information, among financial institutions

-

Security

Security is about advanced cryptographic techniques such as SHA-256 to protect clients’ data, encrypt transactions, and prevent unauthorized access.

-

Immutability

Immutability is about the permanent record of transactions, because once recorded on the blockchain, it will not be altered or deleted.

Now, let’s move further and discuss the work of blockchain technology in banking. First, the client initiates a transaction, such as making a payment. The bank steps in and creates a digital transaction request by defining the sender, recipient, and sum of the transaction. Then, it is signed using cryptographic keys to prove the transaction's authenticity.

The next step is broadcasting the transaction to the node network or computers involved in the blockchain. Their task is to validate the transaction by confirming the identity and verifying funds.

But how does the transaction confirmation work? That’s about the consensus mechanism the nodes apply. For instance, in a Proof-of-Stake consensus mechanism, the number of coins will determine what node will validate the transaction. As soon as the consensus is reached, the client’s transaction gets approved and added to the new block.

Note: Proof-of-Work is another type of consensus mechanism used mainly for Bitcoin transactions, but it isn’t a common practice among banking institutions because solving complex mathematical problems requires high energy consumption.

Banking institutions are less interested in integrating PoW-based blockchain as, according to the 2015 Paris Agreement, financial institutions are obliged to control the level of carbon emissions associated with their financed activities.

Once validated, the transaction is added to the new block. The block is encrypted and added to the previous block linked with the cryptographic hash. The blocks are added to the blockchain in chronological order. The added blocks create a tamper-proof ledger because they contain the hash of the previous blocks, which intensifies the blockchain’s immutability.

The transaction is irreversible and unchangeable when recorded on the blockchain. The recipient will get a notification about the finance transfer. The bank then can undertake additional actions like fraud detection or checks on compliance.

But what about smart contracts? Are they used in banking blockchain? Well, it's not obligatory. Banking indeed can benefit from smart contracts by applying them to automate transactions if the predefined conditions are met. For instance, monthly loan payments.

Nevertheless, banks apply blockchain due to decentralization, security, and immutability for cross-border payment and to secure transactions, which does not require smart contracts.

Key Benefits of Blockchain in Banking

What is blockchain in banking? Distributed ledger simplifies payment procedures and information exchange across banking institutions. Nevertheless, what are the practical benefits of blockchain in the banking system? Let’s dig in.

Transparency

Blockchain is about real-time visibility of the recorded transactions across banking institutions. Transaction history, recorded on the distributed ledger in a time-stamped manner, is visible to the trusted parties who are granted permission to the blockchain, denoting its benefit of transparency.

Immutability

Immutability is another principal blockchain advantage as it makes transactions immutable to tamper with. This is because blockchain operates within the principles of cryptography, decentralization, and consensus.

Once the data is structured into a block, it comprises its own cryptographic hash and the one of the previous block, formulating a cryptographic chain of blocks that is almost impossible to tamper with.

Decentralization excludes a single point of failure, as no individual can alter the record, while access is granted only to trusted parties, like affiliate bank representatives.

Faster Transactions

Blockchain can significantly improve transaction speed as it does not rely on traditional banks' hour-based work. The distributed technology is available 24/7, simplifying transaction initiation and reception.

Additionally, applying smart contracts is a favorable option, which presents the analyzed blockchain benefit as it will automate transaction processing if the predefined conditions are met. So, the client does not have to wait a few days for their transaction to be processed.

Cost Savings

Lastly, blockchain represents a favorable option for cutting expenses, especially in cross-border transactions. The distributed ledger system can eliminate intermediaries, improve settlement time, and reduce fees.

Blockchain promotes direct and peer-to-peer transaction processing by eliminating the dependency on intermediaries such as corresponding banks and SWIFT. As an outcome, the user won’t be charged $10-$50 for middlement service as well as won’t have to wait 1-5 days for the transaction settlement.

Additionally, you might be interested in how blockchain benefits accounting.

Additionally, you might be interested in how blockchain benefits accounting.

Applications of Blockchain in Banking

The distributed ledger technology presents an impressive range of benefits, including significantly improving banking performance. But how can blockchain be used in banking? Let’s find out.

KYC and AML Compliance

Improvements in customer identification is of major importance of blockchain in banking. Traditional banking usually adheres to manual processing relevant to verifying user’s identity, which is financially time-consuming.

Here’s when blockchain takes its move. The decentralized ledger can securely store the client’s verified Know Your Customer information, such as ID and proof of address.

When the identity verification is complete, the blockchain can share the data across the banks. The authorized parties can review the user’s information without re-verification.

Additionally, alleviated compliance to Anti-Money Laundering web of laws is another case opportunity of blockchain for banking. The traditional AML systems depend on batch processing which is time-consuming and might provoke delays in fraud detection.

Blockchain promotes real-time transaction monitoring and marks suspicious activities, economizing time for other bank-relevant operations.

Cross-Border Payments

We’ve already discussed how is blockchain used in banking for cross-border payment by improving settlement and minimizing fees. Nevertheless, there is another revolutionizing application of blockchain for cross-border banking transactions.

One of the critical blockchain use cases in banking is the activity of the consortium of banks such as Santander, HSBC, Barclays, and UBS supporting Fnality International, the initiative, which aims to craft a blockchain-based payment system network that will handle tokenized central bank money.

The initiative's Utility Settlement Coins serve as a digital representation of fiat currencies, which is anticipated to promote near-instant cross-border transaction settlement. Don’t confuse USCs with cryptocurrencies, as central banks’ reserves back the first and promote regulatory compliance.

Optimization of Syndicated Loan Operations

Another example of blockchain's application in banking is simplifying syndicated loan processing. Traditional banking relies on manual reconciliation between the involved parties, and loan settlement can take weeks as costs can move across multiple banking institutions.

Blockchain is about the automatic execution of payments through smart contracts, which promotes instant fund transfers. Near-instant loan disbursements can be represented as tokenized assets enhancing the transaction speed and security.

Challenges and Limitations of Blockchain in Banking Industry

Although distributed blockchain technology revolutionizes the performance of banking industries, you don’t have to forget about the challenges blockchain and banking encounter.

Scalability

As blockchain handles volumes of transactions within the shortest time period, showing a decent level of effectiveness and security, scalability becomes its principal limitation. Continuous rise in demand and influx of transactions processing time increases by slowing down blockchain performance and affecting the rise in transaction fees.

Interconnection with the Legacy Systems

Most traditional banking institutions have relied on centralized legacy systems for years, leading to the amassment of a vast amount of versatile information. Integrating blockchain technology might be challenging because it will require smooth data interoperability between the decentralized blockchain and the centralized bank’s database.

Finally, switching to the blockchain system might cause disruptions during transaction processing, requiring a hybrid approach in which the distributed ledger technology is interconnected with specific functions rather than the whole legacy system.

Dilemma of Regular Compliance

Although we touched on the theme of blockchain compliance with KYC and AML, its integration into the banking system might cause legal dilemmas based on territorial responsibilities and compliance. Blockchain does not have a ‘central administration,’ which implies that each subject node can be subject to different jurisdictions and, therefore, different legal requirements. Even in bank affiliations, some nodes can be the residents of a foreign country, which complicates implementing legal requirements.

Future of Blockchain in Banking

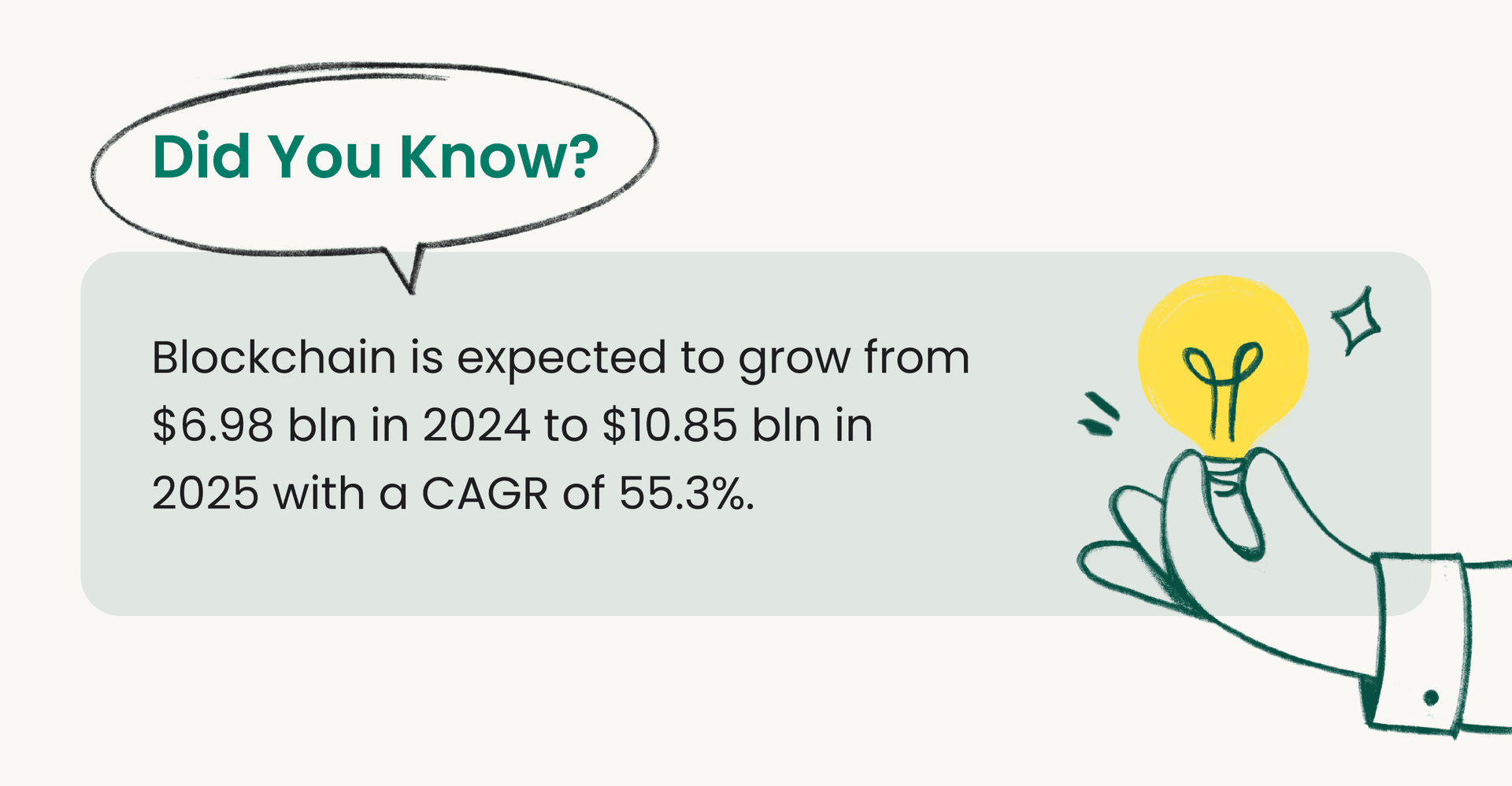

Now it’s time to explore the future trends, predictions, and statistics on blockchain in banking and finance. According to The Business Research Company, blockchain in the banking and finance sectors is anticipated to grow to $40.9 bn at a CAGR of 39.4%. The reasons behind include:

-

Increase in blockchain integration into banking institutions.

-

Intention to reduce fraudulent activities.

-

The growth of public demand for cryptocurrency.

Cryptocurrencies & CBDCs

The contemporary banking industry shows interest in cryptocurrencies, as this type of digital currency can be used to respond favorably to inflation. Additionally, cryptocurrencies can represent a new diversification tool for portfolios.

On the other hand, the growing demand for cryptocurrencies motivates the banking sector to search for effective alternatives. For instance, Central Bank Digital Currencies (CBDCs) are centralized crypto, representing a digital version of the national fiat currency.

Artificial Intelligence

Integrating Artificial Intelligence can boost the overall operability of the blockchain in the banking industry. First of all, AI is about service personalization. By handling data stored on the blockchain, its algorithms can tailor financial services directly to clients’ needs.

Additionally, AI can become an indispensable tool for fraud activity prevention. Artificial Intelligence algorithms analyze the piles of transaction data stored on the blockchain and detect anomalies or fraudulent actions in real-time, making it a potential trend in the banking blockchain.

Choose Agile as Your Reliable Partner

The theme of blockchain in banking is narrowly specialized and requires in-depth considerations to create a non-disruptive hybrid interconnection with the banking legacy system.

Nevertheless, distributed ledger technology can alleviate transaction processing and reduce single-point failure due to its cryptography-related immutability, making blockchain essential for the fintech industry.

So, if you’re interested in integrating blockchain into your business, you might be eager to consider hiring an outside team of developers to maintain quality without compromising cost-efficiency.

Agilie is a European IT outsourcing company that crafts custom digital solutions per the unique requirements of versatile industries such as fintech, real estate, logistics, healthcare, etc.

We offer a range of opportunities, among which custom blockchain development services that will reinforce your business projects:

-

Blockchain Crafting

-

NFT Development

-

Smart Contract Development

-

Decentralized Finance Development

Conclusion

Blockchain use in banking presents truly remarkable opportunities. Minimized fees and improved transaction speed in cross-border payments, immutability, and fraud prevention represent blockchain success in the banking industry. Nevertheless, the challenges of scalability and integration with legacy systems must be considered to boost bank operational efficiency without compromising the centralized database stability.