Fintech (which stands for financial technology) may seem like a very complex and confusing concept to an uninitiated person. But in fact, fintech solutions have long become a familiar part of our personal and professional life. And indeed, we manage finances using mobile applications, pay in the store with a smartphone or even a smartwatch, get loans without leaving the apartment, and much more...

All these are examples of the successful implementation of digital financial tools. However, you probably still have questions... say, what are fintech prospects in the coming years? How can businesses use innovation to thrive and prosper? How does fintech work? How to develop a fintech app?

Don't worry; no need to look for the answers yourselves. We've already done the job and covered the most important fintech-related issues. So just read our latest blog piece.

What is Financial Technology (Fintech)?

In simple terms, the concept covers financial products and services provided with the help of special innovative technologies. Fintech (financial technologies) - technologies that help financial services and companies manage the financial aspects of a business. These include software, applications, processes, and business models. It is also an industry where fintech companies use new financial trends, innovations, like the fintech app development, and solutions to compete with traditional financial institutions for the hearts and funds of customers. Most often, these are tech startups and companies that improve their services with the help of fintech tools. These technologies include artificial intelligence, blockchain, biometrics, and others. We’ll discuss the most popular ones later in the article.

Previously, the finance industry was perceived exclusively in the context of internal developments of financial organizations for entrepreneurs. Now it is as close as possible to the consumer of financial services since it underlies all online transactions - from credit cards to payment services - the options are huge.

The main principle of work is to increase the efficiency of providing financial services, expressed in their more comfortable perception by consumers. In addition, the integration of fintech products allows companies to minimize the human factor - the mistakes and inaccuracies that they make.

Fintech is aimed at improving the financial market and automating at least some of its processes. Among examples are payments via smartphones, mobile banking, online lending, and more.

Fintech Industry Statistics

Anthony Jenkins, ex-head of Barclays, one of the largest banks in the UK, announced back in 2015 that he expected revolutionary changes in the financial area, caused by high-tech startups entering the market. These start-ups, as he knew even then, should be able to work better and faster (sometimes cheaper) than traditional companies. The result was to be a decrease in the number of personnel in the banking sector and a total “uberization” of the financial industry (the emergence of Uber-like fintech platforms).

And Anthony Jenkins proved right. As recent history shows, the volume of investment in the industry is growing annually by more than 45% worldwide (research by Investment Bank). And according to EY's Fintech Adoption study, about 1/3 of users enjoy at least two innovative digital financial services (globally). As to fintech popularity, the United Kingdom is leading so far (42%), followed by Spain (37%) and Germany (35%). Despite such a promising indicator, the European fintech market is inferior to the American and Canadian ones in terms of investment volume and the number of transactions. Be that as it may, the fintech prospects are very bright.

The popularity of specific fintech services in numbers

- Mobile payments: 50% popularity rating;

- Online insurance: almost 25%;

- Fintech platforms for investment: 20%;

- Financial planning: 10%;

- Loan-oriented digital services: 10%.

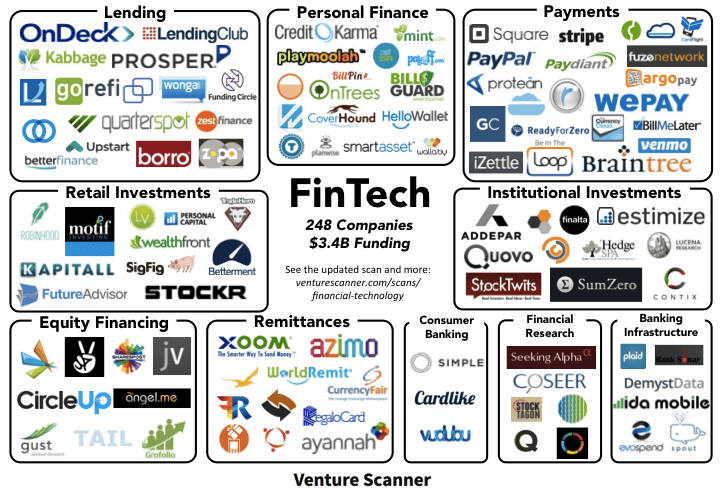

What Is a Fintech Company?

Any business, which provides financial services using digital technologies, can get the 'fintech' prefix. It includes both startups and institutions that have been on the market for a long time and want to keep up with the times.

On the one hand, the fintech approach has been developing rapidly, and new products are constantly appearing in it. Virtual cards, money transfer, online trading - opportunities that were simply not available before. Developers of such products quickly grow into unicorn companies and become successful.

On the other hand, fintech does not create new solutions, but takes existing ones and makes them more convenient. Banking, loans, and investment management have long existed in the offline market and are proving to be viable. Fintech companies are simply moving proven solutions online. This is how neobanks, credit services, and investment applications appear. You can check how to hire fintech software developers or consider fintech development outsourcing to build the projects you need.

Neobank is a financial organization that operates only in the online space. It communicates with clients and provides services without offices, branches, and affiliates.

Neobanks are:

- licensed financial institutions that independently conduct all transactions and perform all the functions of offline banks;

- intermediary organizations that cooperate with an offline financial institution and help to use their services remotely.

The success of such products is more predictable and often justifies expectations.

A company may choose to adopt innovative financial technology for a variety of betterment reasons, such as:

- improving the quality and expanding the range of services provided (after all, some services are only available online);

- increased transaction security and fraud protection (fewer risks involved);

- reduced overhead costs (since digitalization allows replacing part of the employees with robotic algorithms);

- ensuring competitiveness;

- minimization of the human factor, whether it be errors or inaccuracies;

- guarantee of stability of banking processes.

So let's recap: what is a fintech company? It is an organization that seeks to maximize the effectiveness of its services through innovation. It wants people to feel comfortable being among its loyal customers.

Who Uses Fintech Solutions?

Financial technology ecosystems utilize a combination of analytical tools and data-driven frameworks to optimize how consumers, investors, and organizations execute transactions. Modern personal finance application development implements automated budget tracking and real-time expense analysis, fundamentally altering consumer behavioral patterns regarding monetary management. These fintech-enabled solutions prioritize data encryption and high-availability architecture to ensure secure, cross-platform synchronization of sensitive financial data.

From mobile payment apps to insurance and investment companies, fintech has disrupted the traditional financial and banking industries. As its efficiency grows, it becomes a threat to the very existence of conventional financial institutions to build a fintech app.

Who are they, the users of these services? We’d like to distinguish 2 main types.

Fintech companies are constantly improving financial services to make them more accessible and focus on businesses and consumers. By making financial systems easier to use and more accessible, businesses and consumers will also improve their business.

There are two main types of fintech users: consumers and business users.

Financial technology growth has been slow in the past due to generally isolated, non-integrated fintech applications. However, the development of fintech apps has accelerated in recent years.

Central to this accelerated growth is the creation of opportunities for all user groups to interact more effectively with each other. Key drivers will be advances in decentralized access, more accurate analytics, big data, more information, and mobile banking.

B2B solutions

From time to time, businesses, like ordinary people, have no other choice but to turn to banks and other similar institutions for loans and various kinds of financing. Usually, all these procedures take a lot of time... or, rather, they used to take a lot of time. Fintech technologies have simplified the whole thing, and now a company can receive financial assistance even through a mobile phone.

However, obtaining loans is just one example of what the financial services industry is able to offer B2B users.

B2C solutions

The second option is users (individuals) who resort to fintech services provided by companies (businesses). We're talking about mobile payments (how about PayPal or Apple Pay?) and all sorts of finance-oriented software like Mint.

We discussed Mint in one of the articles, so take your time to read it.

We discussed Mint in one of the articles, so take your time to read it.

In the case of B2C users, fintech is most popular among millennials: they are young enough to embrace innovation and mature enough to be solvent.

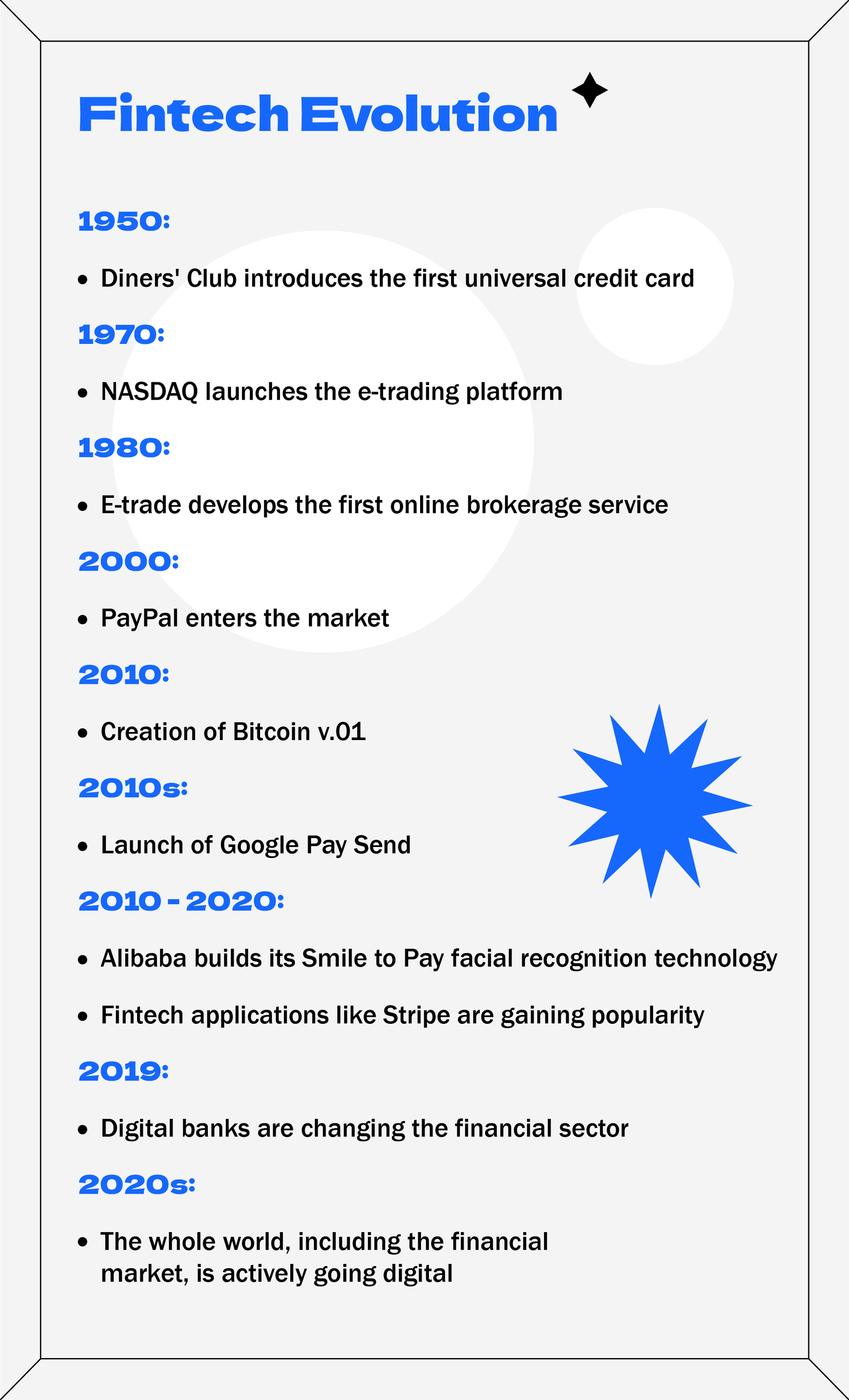

A Brief History of the Fintech Industry

It all started more than 70 years ago, in the middle of the 20th century, when the Diners Club credit payment card appeared on the market. It was Frank McNamare who came up with the idea; it happened after a rather unpleasant situation when he didn’t have enough money to pay for his dinner at a New York restaurant. And he didn't want anyone else to have the same experience… so he had found a proper solution.

In the 60s of the last century, various self-service points became popular... which prompted the creation of ATMs.

As to the very term “fintech”, it was coined only in the 80s. Peter Knight used it in his article when describing a bot working with his email.

And then the 21st century began, and the global crisis struck, which resulted in people not trusting traditional banks. It was the best moment to revolutionize the entire financial sector.

As you can see, FinTech use cases are greatly influenced by the historical period. In the old days, a simple credit card was considered the pinnacle of innovation... today, other services and products are conquering the market. Let's explore them in detail.

Popular Fintech Services & Products

Here are some specific examples of fintech (the most in-demand ones). They’ll help you fully clarify the issue.

#1. Payments and money transfers

The clearest example of how technology is improving the financial sector is, of course, the use of a mobile phone to receive financial services. Who among us hasn't made purchases through a digital payment system? We all appreciate this great opportunity, which has significantly simplified our life and made shopping (and other things) much more pleasant and comfortable.

Also, let's not forget about mobile banking: as we said, in recent years, financial institutions have been increasingly offering their services remotely, which has led to a decrease in the need for physical banking branches... (and it means banks are saving their money).

And finally, we’re talking about numerous alternative payment methods (contactless payments, payments using terminals and QR codes, etc.).

#2. Providing financial services through social networks

It’s about the personalization of financial services. The point is, we all, as users of social networks, report a lot of public information about ourselves, including our tastes, facts of life, and more. Special algorithms process such data and get the opportunity to guess which offer you cannot refuse (in the context of the financial market, of course).

However, this applies not only to financial products and services but also to technologies for implementing them in practice (AI and big data)... which is detailed further. And AI in fintech has become such a tool.

#3. Cryptocurrencies

Cryptocurrency is a concept closely related to the fintech area (since we're dealing with both digital technologies and money). There are many examples of cryptocurrencies: the world-famous bitcoin that started it all, Ethereum, Litecoin, Ripple, and many others (the number of cryptocurrencies continues to grow, and if you want to create your own crypto coin, read our tips).

Any cryptocurrency is based on the blockchain system and allows you to make transfers without involving third parties (intermediaries like banks). It ensures greater transaction speed and guarantees privacy and anonymity.

#4. Lending and loans

Also, let's not discount remote loans, ones that don't require the participation of credit institutions. These are special fintech platforms serving as a meeting place (sort of) for creditors and debtors.

But remember: some states require a license to work with lending. So sometimes the owners of the mentioned platforms have partnership agreements with credit institutions.

#5. Insurance

Fintech has also made itself known in the insurance industry. Many insurance companies, especially startups, have begun to work online, offering to issue their services on a website or in a mobile application. You can insure online any property, from a car and a house to art objects like paintings. Personal insurance is also possible: for life and health.

More and more insurance companies, not to mention fintech startups, have begun to work online and offer their services in a remote digital format. This interaction type saves customers from having to personally visit the institution to draw up an insurance policy.

And insurance companies benefit from simplifying their business processes and thereby reducing their overhead costs.

#6. Investments

Investments in stocks and bonds are also among the digital financial services. After all, it is much easier to do these things remotely, using a mobile phone or another favorite device, be it a netbook or laptop. Moreover, special robotic counselors have recently entered the market, and they're capable of giving users helpful investment advice. Sounds great, doesn’t it?

#7. Security

Fintech can be used to better protect clients' finances. It’s about preventing fraud, such as unauthorized debiting of funds, and reliable verification of the user's identity (and so on).

And by the way, in order to implement reliable person identification (which is an inevitable step in preventing online payment fraud), one needs to use biometrics, AI, machine learning, and other similar technologies. We think it's time to discuss them in more detail!

Technologies Behind Financial Products and Services

#1. Big Data

All businesses deal with a huge, never-ending stream of data. There is so much of this data that the term Big Data has appeared. The concept also includes various tools needed to process and analyze a vast information array.

Why analyze Big Data? The answer is actually obvious: business owners define the behavioral patterns of their customers, so that they can sell their products and services better and more efficiently.

In the financial sector, big data helps in predicting customer investment and market changes, as well as in analyzing user habits. The result, among other things, is the possibility of the aforementioned improvement in fraud detection.

- A good example of using the financial technology in question is the American Express case. The company issued loans at less attractive terms to those who liked buying goods in discount centers (which indicated these clients were short of money). To make a long story short, the company managed to collect information about how certain customers behave and used it to create a profitable business strategy. Surely, the strategy isn't so great from the perspective of customers, but it's not the point.

#2. Artificial intelligence (AI)

Big data itself is just a flow of information. We need a tool to process it. And AI has become such a tool.

AI is a very special system, which mimics human behavior to perform certain tasks. Let’s say, it’s capable of analyzing incoming data (big data) and making various kinds of investment forecasts based on it. Also, it can help you draw conclusions about people's financial habits. In other words, AI allows financial institutions to better understand their customers.

Another option for AI-based fintech solutions is chatbots. Being controlled by artificial intelligence (surely, they can't have a human one!), chatbots provide round-the-clock support to clients of financial institutions.

- The machine learning we mentioned earlier is also part of AI. The essence of the mechanism lies in the system's ability to self-learn and self-develop by solving similar problems and performing similar tasks.

#3. Robotic Process Automation

Another technology related to AI is the automation of specific repetitive tasks. It is commonly called Robotic Process Automation (or RPA for short). These repetitive tasks usually require no special skills, which is why companies implement RPA and thereby improve their business processes.

Speaking of fintech services, RPA helps to process financial information such as accounts payable and receivable. The robotic system copes with such work faster than a person (and its result is more reliable).

#4. Biometrics

Almost everyone has experience in dealing with biometric security systems. Usually, they're protecting payment and banking apps, so the technology is fintech-related either.

These security systems are about the recognition of a user's biometric data: his/her fingerprint, retina or face (the so-called Face ID).

#5. Tokenization

Recently, the development of financial services apps has increasingly been associated with the tokenization of physical assets, which implies their digital display in special registries. And the first thing that comes to mind when talking about tokenization is of course cryptocurrencies (which is far from the only example, though).

#6. Cloud storage

We discussed the huge amount of data that large companies have to deal with. And in addition to processing the information, we also need to store it, preferably securely.

Cloud storage seems to be a great solution to the problem, as it makes data available anywhere in the world.

#7. Blockchain

We've written a lot about the concept of blockchain and its business benefits in our other articles. So let's be brief: blockchain is a secure and decentralized system for distributed data storage. One can resort to it to perform many tasks related to the financial services industry: we’re speaking of the creation of smart contracts and cryptocurrencies, the protection of the authenticity of documents, trading, and so on.

Regulatory Evolution and The Open Finance Ecosystem

Modern fintech ecosystems rely on RegTech to navigate complex legal landscapes and ensure global AML (Anti-Money Laundering) and KYC (Know Your Customer) compliance. These automated systems monitor transactions in real-time, significantly reducing risks associated with financial crime while streamlining user onboarding. Integrating regulatory technology allows firms to scale across various jurisdictions without the massive overhead of manual document verification.

The shift toward Open Banking has transformed the industry into an API Economy, facilitated by regulatory frameworks like PSD2 and Open Finance standards. These protocols enable secure, authorized data sharing between institutions, allowing third-party providers to build consolidated financial management tools. This interoperability fosters competition and gives consumers total control over their financial footprint across different platforms.

Embedded Finance now allows non-financial brands to integrate credit, insurance, or payment processing directly into their user journeys at the point of need. Simultaneously, the adoption of Generative AI is driving hyper-personalization, moving beyond standard automation to provide sophisticated financial co-pilots. These tools analyze real-time data to offer predictive wealth management advice tailored to individual risk profiles and spending habits.

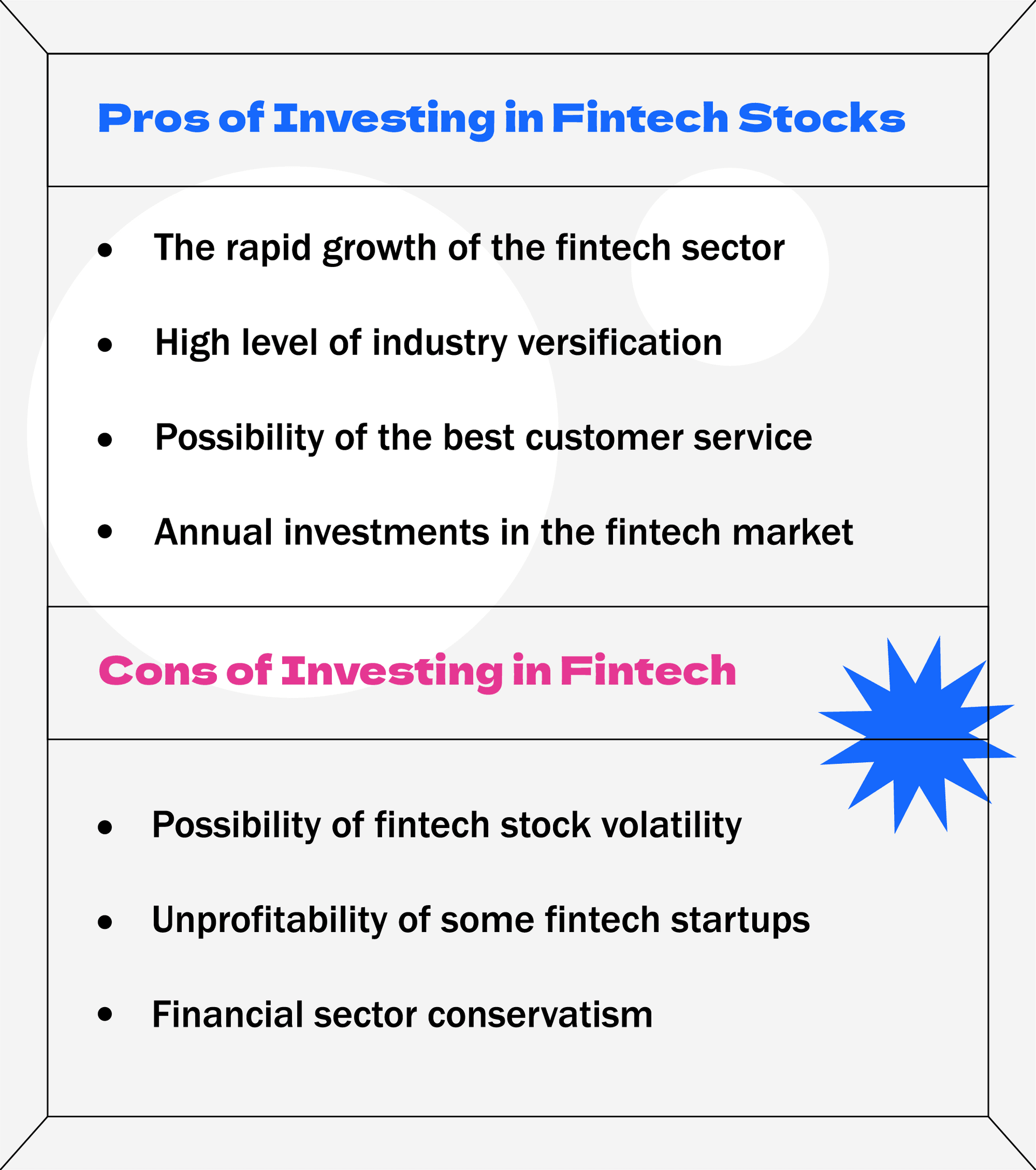

Pros & Cons of the Fintech Industry

We've already answered the questions "What is financial technology?" and "How does fintech work?". Now it's time to discuss the issue of expediency and desirability, so to say... is the game worth the candle?

Investments in Fintech Stocks: Is It Worth It?

Investing in intriguing new markets and areas can be a profitable business… or, on the contrary, lead to significant financial losses. So before giving you specific advice, let's analyze the pros and cons of investing in fintech.

The situation is generally satisfactory and appears most promising: the fintech market is flourishing and becoming stronger year by year. It's time to join it too, and investing is a good way to do that.

Another option is to run your own startup… or strengthen an existing company with innovative technologies.

Development of Financial Services Apps: What Are the Prospects?

You already know why financial companies should innovate their processes (we've made our point in the “What is a fintech company?” section). But if you’re still in doubt, take a look at some more encouraging statistics.

As studies show, banking systems that have replaced more than 50% of middle-level personnel with artificial intelligence have cut costs many times over and optimized some processes. Of course, we are talking about simple, routine tasks (repetitive ones).

Are you new to the market? Then perhaps the examples below will inspire you to turn the situation around.

Successful Fintech Startups

- Cake. Service with a very “delicious” name offers to install a mobile app, link a card to it, and use it to pay for purchases in cafes and restaurants. The application seems to be simple in its functionality, but it’s very user-friendly, which makes it in high demand anyway.

- FingoPay. Here we’re dealing with an advanced version of a payment application based on biometric fingerprint scanning. The idea belongs to the startup Sthaler. It was this company that proposed the FingoPay technology, the essence of which is to create a “map of the veins’ location”. It can be linked to a credit card or bank account.

- Klarna. Speaking of successful fintech startups, let's not forget about the Swedish project Klarna. Its stated mission is to make payments as easy as possible... and some even think it has the potential to become a strong competitor to PayPal.

- eToro is a kind of social trading network, which works with currencies, commodities, and the like. Its goal is to track and analyze successful trading projects (so that you can follow the lead of the best market players).

- LendingClub is another inspiring project. The platform acts as an intermediary between borrowers and lenders in the United States.

- Robinhood (a mobile application) allows you to buy and sell stocks using mobile devices. Moreover, no fees are required, which increases the popularity of the service.

The Future of the Financial Services Industry

Fintech is diverse. It includes both products for customers and closed solutions for businesses. Therefore, work in this area is diverse: you can deal with solving business problems aimed at improving processes and user experience, or you can deal with purely technological development. Fintech is attractive because it can quickly and with minimal effort on the part of the user to solve his problems and needs.

Companies have already begun to save money by reducing the need to hire employees; also, they’ve increased profits by streamlining their processes. And that's just the beginning! According to the Pitchbook analytical forecast, by 2025 the volume of the fintech industry will have reached a capitalization of more than $220 billion (globally speaking).

Alas, the pandemic has made its own adjustments, but the forecasts are still good. The industry continues to evolve because nothing can stop the progress.