The integration of IoT payment gateways requires precise orchestration of tokenization, PIS (Payment Initiation Service), and cryptographic authentication. Financial institutions deploying autonomous transaction systems must prioritize data security protocols and low-latency API communication. This technical brief evaluates the architectural requirements for scaling IoT-enabled financial services and mitigating systemic vulnerabilities in machine-to-machine payment environments.

What Are Internet of Things Payments?

The Internet of Things (IoT) unites smart objects into a single system, and they use special built-in sensors to collect data and exchange it with each other.

Why do we need IoT? In essence, the answer is very simple: IoT devices can improve our lives and optimize business processes. This includes everything from automatic regulation of heating and lighting in our houses to efficient factory control.

IoT has penetrated into different spheres of life, and the world of finance is just one of them.

Difference between contactless and IoP payment models

The global contactless payment market is predicted to reach $2.23 trillion by 2025, which is impressive in itself. So it's probably the best time to address the issue in question with the utmost seriousness.

And by the way, do you know that the concepts of contactless and internet of things payments cannot be called identical (although they’re pretty alike)?

Contactless payments

As it’s logical to assume, such a payment doesn’t require direct contact between the card and the terminal. Moreover, any smart device with the NFC function and activated payment software can serve as a bank card: smartwatches, fitness trackers, rings, key fobs, and other similar gadgets called wearables (we’re discussing the matter in greater detail in the Promising Payment Types section).

Many fashion brands are already creating special high-tech accessories, which may function as digital wallets. So in the near future, we'll be able to bring, say, an elegant pendant (or something else) to the terminal to pay for the purchase.

It sounds pretty cool, right? But it's not really IoT payment solutions just yet.

The essence of smart payment in IoT

Wearables have transformed the financial market and thus ushered in even greater technological advances. In particular, the IoT devices in the payments industry have produced stunning results.

In this case, IoT devices are household appliances (say, a refrigerator), parts of a smart car, and so on. An important condition: these objects must be connected to the Internet.

Ideally, payments in the IoT, also known as invisible, don't need human participation (or such participation is reduced to the required minimum).

Let's build a hierarchy of invisible transactions, which in their perfect form become payments without human involvement:

-

At the initial level, a smart device can only inform you about the status of your bank account, it's not allowed to perform any real financial transactions. A simple example: you ask a smart speaker to tell you what your account balance is, and it fulfills your order. You yourself don't have to do anything.

-

The second stage is more like IoT payment solutions, but human participation isn't excluded yet (but it is significantly reduced). Usually, the user has to confirm the transaction through biometric authentication or something like that. For example, he receives a notification asking if he wants to confirm a payment, and he must respond to it.

-

The third level implies automated smart payments made when certain conditions are met (let’s say, when the cleaning products and detergents in the washer start to run out, the system makes a purchase of new ones).

-

And finally, we see real, full-fledged IoT mobile payments when transactional processes don't involve a person at all. Smart devices initiate payments by themselves, taking into account user behavior, needs, and special instructions (such as financial limits, etc.). A striking example is a shop, whose stocks are being replenished without direct human participation, the system itself analyzes the demand of buyers, their activity, the level of stocks and makes the necessary purchases (within the established budget).

Brief evolution of IoT payment

What led to the new payment solutions? What was the initial impetus and initiated the mentioned evolution?

-

Consumer needs. We, the consumers, have become quite capricious and demanding. We are used to doing things with maximum comfort, including when shopping. And it's not only about our exactingness, we're just too busy and don't mind delegating some simple tasks to digital algorithms (and conducting verified transactions is one of those tasks).

-

Business needs. The need of consumers results in the needs of the companies, which serve them. In the end, a dissatisfied consumer is unlikely to become a paying buyer. Therefore, if a consumer wants to have access to an IoT payment platform, the company must do its best to provide the desired.

-

Ubiquitous internet. Whereas earlier the Internet was the privilege of the elite, so to say, the chosen ones, now online access is everywhere. It's time to make the most of the new opportunities.

-

Affordability. Implementation of smart systems is still expensive, but it becomes more affordable every year.

-

The natural development of digital technologies, which occurs regardless of whether we want it or not.

Ideas for bringing IoT to the finance industry

-

Car as a means of payment. Just picture the scene: your car itself pays for the gas station, toll road, parking, etc. You, at the wheel, no longer have to leave the car to make a payment or deal with cash, nothing is going to distract you from driving. Transactions are being processed without your participation (but with your knowledge and permission, of course).

-

AI-based smart home. A home like this can totally transform the lives of family members. Among others, the AI system is able to make some of the required purchases on its own. Say, how about buying food based on the dietary preference of house dwellers and within their budget?

-

By the by, the IoT payment platform will only order products from eligible online stores (those that meet the specified criteria).

-

-

Smart self-service stores. Purchases are being paid for with little or no human intervention. The buyer wanders around the store, choosing the products he needs, and payment is being processed automatically and imperceptibly (for more details, see the section where we give real-life examples).

-

The coffee machine could also be self-service with payment in the background, which greatly saves the time and effort of the consumer.

Of course, it’s just a shortlist of new payment solutions, in fact, it largely depends on the needs of a particular person or company and the technological capability to implement the plan.

And speaking of technological capability…

Technologies to implement IoT in Payments

We won't be able to list all the technologies required, so we'll restrict ourselves to the most popular ones.

Big Data

The Internet of Things implies the constant collection and processing of information, and since there is a lot of it, the concept of Big Date arises.

Let’s discuss it at length.

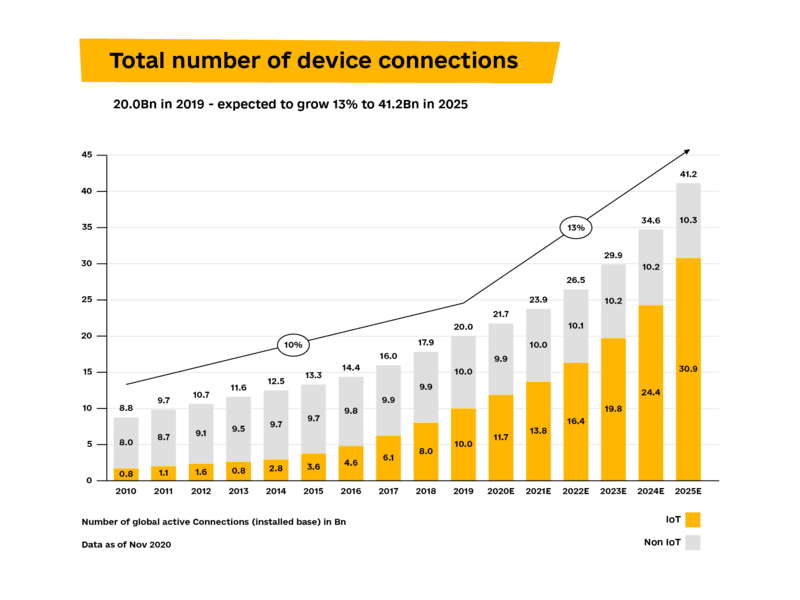

So, we’re dealing with smart devices, which collect many pieces of information in real time. And they are predicted to generate 73.1 zettabytes of data by 2025 (not bad, yeah?).

IoT sensors are collecting data on the state of objects (such as on/off mode), their location, movement of people, and more. And all the gathered information goes to the central system, which must process it and use it appropriately (say, to automate some routine tasks).

Although financial transactions are only a small part of the Internet of Things world, they are still associated with the ongoing processing of big data.

AI & Machine learning technologies

Of course, there isn’t the slightest chance of success without the use of AI technology. After all, the IoT payment platform is designed to make independent decisions, initiate transactions, which means it must have intelligence (albeit artificial).

Also, AI implies the implementation of machine-learning algorithms. Here, again, Big Data is involved: sensors collect information, the central system analyzes it, and gradually self-trains (becomes smarter).

Blockchain

According to Gartner estimates, blockchain technology is likely to reach the so-called "productivity plateau" in 2022. That’s precisely the reason for its popularization: the blockchain is starting to be more and more actively implemented in various industry solutions. And IoT mobile payments should also take their place in the whole scheme.

What is blockchain in simple terms? Take a closer look at the name itself: it is a chain of blocks. These blocks are distributed among the trusted participants of a certain system.

This leads us to the following:

-

decentralization (information is distributed among all participants);

-

immutability of chain links;

-

uncontrollability by any regulatory body, which implies the absence of third parties;

-

reliability of transactions (any operation is carried out only after being confirmed by each participant in the system).

We think it is quite clear why one should use blockchain to implement IoT in Payments.

Tokenization

Tokenization, too, is related to the concept of blockchain and based on it. In fact, we’re dealing with the digitization of physical assets, turning them into some kind of tokens.

Why do we need tokenization when making payments? As you well understand, contactless transactions mean the use of card data. And if the device, which helps to make a payment, is vulnerable (and most of them usually are), there is a risk of this information being stolen (which in no case should be allowed).

Tokenization replaces the user's real card number with a unique code (token), and it can only be used to perform a single transaction. Any subsequent operation requires a new (also unique) token. So if a fraudster intercepts information about a token during the transaction process, nothing bad will happen: being a one-time code, the token has already outlived its usefulness. Thus, we secure IoT payments and make them much more reliable.

By the way, you’re allowed to tokenize not only money but also any physical assets. However, it's a bit off-topic.

Large players from different markets are actively involved in improving tokenization. A prime example is Netflix, which has recently become a token provider. So even if the data of its user is stolen, disaster won't strike: the information is linked to a specific account, and the money tied to it can only be used to buy access to Netflix content, nothing else is possible.

Key Benefits of IoT Payment Solutions

Let's look at these benefits from a consumer and business perspective (separately).

Consumer perspective

-

shorter transaction time (in the end, payments have become almost invisible to the user!);

-

increased comfort: since user involvement is minimized, comfort reaches the highest level;

-

improving financial habits. The IoT approach teaches users to spend money wisely, without exceeding their budget limits. The explanation is simple: the IoP system will do as it's been instructed, digital algorithms aren't subject to any temptations (unlike us, humans).

-

lack of physical contact, which is a must-have in a pandemic.

Business perspective

-

personalization of offers. Big data and AI technology make it possible to effectively analyze user behavior and provide customers with best-price offers;

-

higher buying activity. According to the analysis of statistical data, the less often people use paper money, the more they spend (parting with money in non-cash seems to be easier);

-

accelerating the processing of financial transactions (due to the aforementioned invisibility of payments);

-

greater efficiency of the company, as a result of all of the above.

The Most Promising Types of IoT Payments

We want to warn you: the evolution of IoT payments is in full swing (to be exact, their journey has just started), so the schemes described below are very crude and far from complete. There is still a lot of work to be done to make the dream (IoP) a reality.

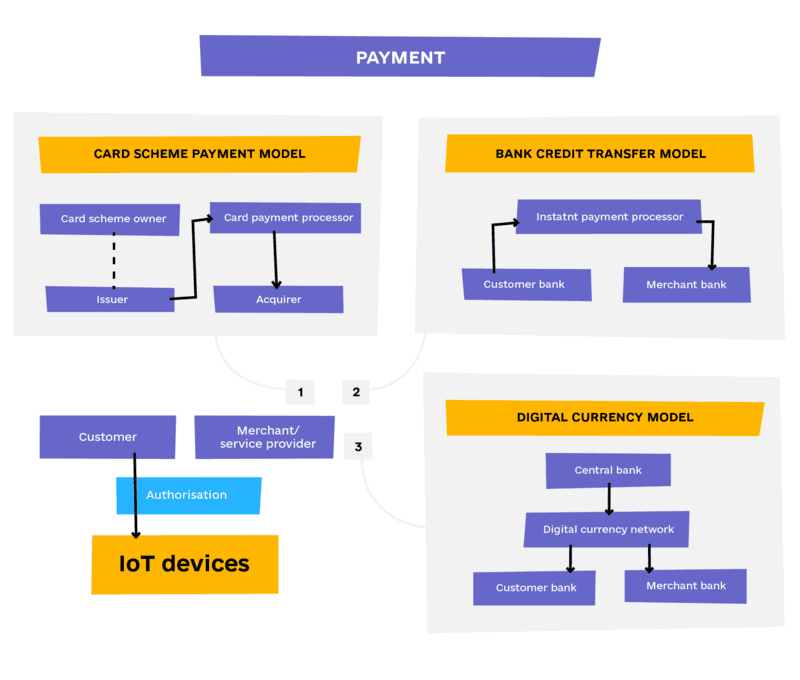

NFC-based model

NFC (Near Field Communication) is a contactless payment technology. Let's understand its essence by looking at traditional plastic cards.

When implementing the NFC model, information exchange occurs without direct contact, to be precise, at a short distance of certain devices from each other (such as a bank card and terminal). So there is no real physical interaction (contact). The data is being read using magnetic induction.

What do IoT mobile payments have to do with it, you ask? It's very simple: NFC technology, along with tokenization (which is detailed above), allows turning almost any device into a kind of bank card. And we're familiar with many examples of the sort: in the end, purchases using smartphones, rings, and other things have become commonplace. So why not turn your car into a 'bank card' too so that you can pay for certain purchases on the road while driving?

Okay, let's specify: we’re not making the car itself a payment platform, we’re just embedding a token-based card into it, provided your vehicle has an online connection (which is key when it comes to the Internet of Things, anyway).

PIS model

You've probably heard about instant payments (not to be confused with IoT payments!). It’s an ideal option if you need to urgently transfer money to your friend, acquaintance, relative abroad: given that he or she lives in Europe and his/her bank participates in the SEPA program.

SEPA stands for Single Euro Payments Area. The initiative simplifies, streamlines, and somewhat standardizes the banking process within Europe. SEPA covers the entire European Union as well as a number of other countries including Iceland, Switzerland, Norway, Liechtenstein, the United Kingdom, Monaco, etc.

All this became possible thanks to the EU directive PSD2, which creates conditions for open banking. As a result, trusted third parties have access to financial information about the bank's client with his or her permission (and only through the enhanced authentication system!).

PSD2 led to the concept of PIS (Payment Initiation Service) providers that can process payments on behalf of the payer, helping him or her buy an item online, transfer money, and the like.

Moreover, such PIS-based schemes could be used to implement IoT in payments (and they are already being used, actually).

Cryptocurrency model

And of course, let's not forget about the cryptocurrency and the distributed ledger, which implies the ability to conduct financial transactions without the participation of third parties (we’ve mentioned these things when discussing blockchain technology). As many believe, digital currency and distributed ledger would make a great basis for building IoT payment platforms.

So far, it is difficult to say what the cryptocurrency approach will result in; it may be necessary to create some standards and involve banking regulators. In any case, the model appears to be very promising.

Challenges of IoP Implementation

Consumer conservatism

Although the benefits of IoT payment solutions are undeniable, and there is a demand for them, (in the end, their emergence is a kind of response to this demand), not all people, especially the older generation, are ready to accept innovations. And they have the point!

In particular, their anxiety is based on the following:

-

fear of unfamiliar technologies, which is common to older people;

-

distrust of digital algorithms (“Why should my refrigerator decide what and when to buy?!”);

-

the habit of paying in cash;

-

a natural concern associated with the security of IoT payments.

However, the anxiety and distrust of users will disappear by themselves over time, when new technologies prove their effectiveness and suitability.

Security issues

The key challenges with smart payment in IoT are security and data protection issues. Unfortunately, Internet of Things devices are potentially vulnerable to various cyber-attacks and provide more opportunities to steal data... which cyber fraudsters are willing to take advantage of.

On the other hand, the implementation of the IoT system allows better studying the user, his behavior, habits, payment history, and, as a result, drawing up a realistic view of him. And if this user does something unusual, which is totally out of his identified character (say, he tries to make an atypical payment), there will be a chance to prevent fraud before real harm is done.

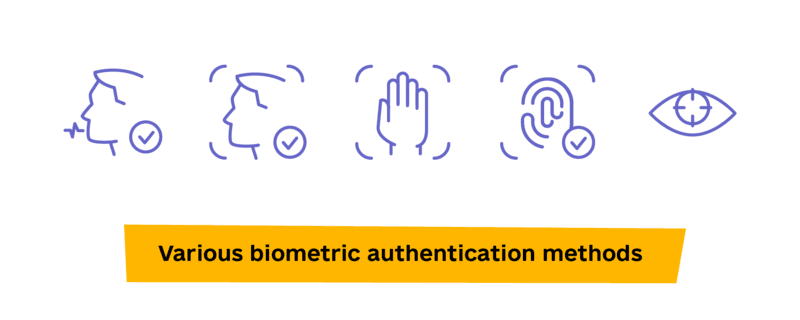

Authentication

There are many ways to protect user data, but in any case, the most important factor is authentication, which consists of two aspects:

-

Authentication of the device itself. Alas, many devices aren't originally designed to support and protect financial transactions. That's why the introduction of an IoP function can lead to major security problems (which plays into fraudsters' hands).

-

Device manufacturers are seriously poring at the mentioned problem by trying to create the most reliable and trustworthy authentication system. Such a system is aimed to ensure the safe interaction of devices in the network;

-

-

User authentication. That’s where biometrics usually comes in. The user may confirm his payment by voice (if his hands are full), put his palm to a special panel in the store, and so on.

When discussing IoT in the finance industry and security challenges, it should be added that some payment scenarios require new methods of authentication and data protection, which are still under development. In the ideal case, as we've already said, internet of things payments should be initiated by devices themselves without involving a human... which means the process of authentication becomes more complicated. For example, how to confirm the payment and make sure it is made with the full consent of the client? Surely, it's something worth considering.

Fortunately, it's not our problem to solve.

Compatibility of services, systems, and devices

Since payments in the IoT are a new area, unified, globally approved standards haven't yet been developed, their establishment is something to look forward to. Otherwise, we may face a situation where some software doesn't work properly with a certain device. In other words, there is no confidence in the compatibility of digital products provided by different companies.

To solve the problem, it is enough to discuss and document the rules, which IT developers and device manufacturers will have to follow.

Imperfectly optimized algorithms

The connection of the IoT to the finance industry has just begun, so we can expect all sorts of incidents at the initial stages: say, the refrigerator spends about $ 1000 when ordering food while it was meant to be $100. However, in the future, these situations will be eliminated.

The introduction of any new technology involves overcoming certain pitfalls. Dealing with obstacles is a natural way of development and growth of both people and digital systems. And the evolution of IoT payment is no exception. However, the possible risks and dangers aren’t a good reason to avoid innovations, which will subsequently bring a lot of benefits to each party to the process.

Innovative IoT Payment Solution Examples

-

Voice banking from NatWest, implemented in 2019 with the help of Google Assistant. The function works at a rather primitive level and allows you to get information on your bank account, nothing else.

-

Amazon Go, which provides increased convenience while shopping. Let’s take a look at how it works:

-

At the entrance to the store, the customer is authorized via the Amazon Go mobile app (as you might have already guessed, the application supports payments in the IoT environment);

-

The application keeps running in the background and tracks the buyer's purchases (the tracking process is based on RFID tags and video cameras);

-

A product taken from the shelf is automatically added to the shopping list (and it disappears from it if you put it back);

-

Payment takes place upon leaving the store.

-

-

Smart refrigerators from Samsung (based on software provided by MasterCard). These refrigerators not only control the temperature of the products but are also trained to order food items;

-

OpenTable as an example of the use of IoT mobile payments in the restaurant business. The goal of OpenTable is to simplify transactional processes.

Summary

We gave you a lot of research data (you’ll find more of them here) and offered you many useful tips. These tips might be handy in case you’re willing to follow the latest trends in the payments industry.