Blockchain has become a paradigm shift that changes the operations of different industries. Nevertheless, like any other disruptive technology, a lot of myths and misconceptions have appeared. We should differentiate between fact and fiction to use blockchain technology effectively and responsibly. We can better understand what blockchain is (and isn’t), how it functions, and the varied applications it holds besides cryptocurrencies by clarifying these misconceptions.

-

Blockchain is not just about Bitcoin; it is the technology that can transform different fields.

-

Blockchains are strong but not flawless, and being aware of the possible weak sections is a very important thing in keeping the network safe.

-

Educational investment and partnerships with software development experts are the main factors for businesses that will use blockchain technology.

Myth 1: Blockchain and Bitcoin Are the Same

Among the most common myths about blockchain technology is the confusion between the blockchain and Bitcoin. Blockchain and Bitcoin were created simultaneously, so they are widely believed to be the same thing. However, we must understand that blockchain is a much broader term. It is the technology that created Bitcoin. While Bitcoin is indeed the first and most famous application of this technology, equating the two is like saying that Google is the Internet.

Blockchain is a decentralized digital ledger technology (DLT) that records transactions across multiple computers so that the records cannot be altered retroactively, without the alteration of all subsequent blocks and the consensus of the network.

This makes blockchain a naturally secure and transparent method of data and transaction recording.

Bitcoin is a type of digital currency based on blockchain technology and used for secure, anonymous, and decentralized financial transactions. The blockchain of Bitcoin acts as a public ledger for all the transactions in the Bitcoin network, thus, it is possible to transfer digital currency securely without the use of intermediaries like banks or governments.

Blockchain technology can be much broader than purely financial transactions. It can be used in different industries with various aims. Nowadays, many businesses are studying how enterprise blockchain development can improve their operations.

Here are a few examples:

Healthcare: Blockchain can guarantee the safety of medical records storage and sharing. Thus, they are only available to authorized personnel and patients and lead to quicker diagnosis and treatment.

Financial Services: Blockchain is a viable solution for international payments, real-time settlements, and improving transaction transparency and security.

Digital Identity: Blockchain can correct identity theft and fraud by adding digital identities that cannot be changed. For example, Estonia's e-Residency program is the first of its kind, a government-issued digital identity that allows entrepreneurs from anywhere in the world to operate and conduct business online in the EU.

Real Estate: Blockchain can simplify property transactions such as sales, leasing, and financing by reducing paperwork and improving transparency.

Learn more about the evolution of Blockchain from Bitcoin to business applications.

Learn more about the evolution of Blockchain from Bitcoin to business applications.

Myth 2: Blockchain Transactions Are Always Anonymous

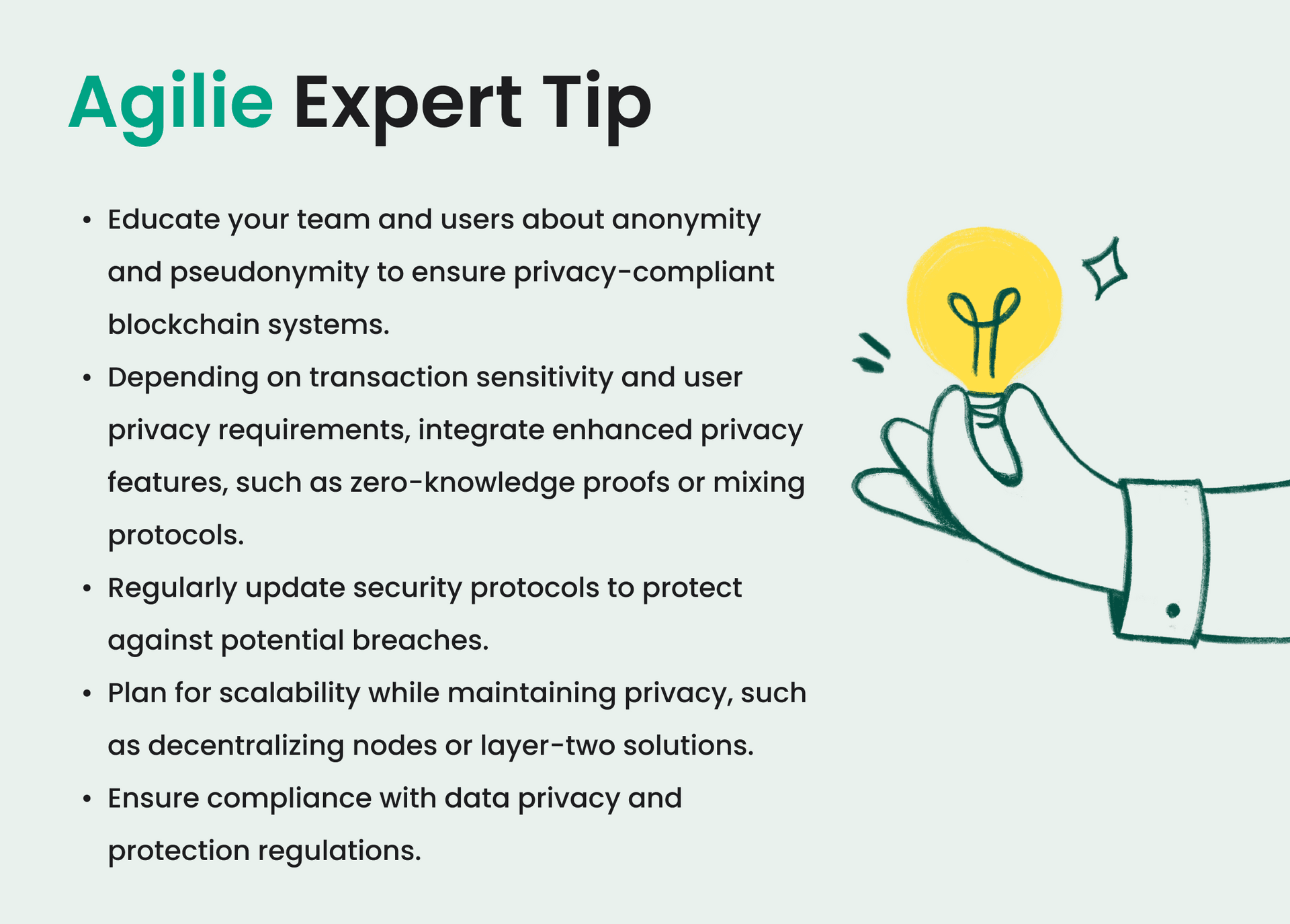

A frequent mistake people make about blockchain technology is that it is automatically anonymous to its users. However, the truth is more nuanced. Blockchain transactions are not strictly anonymous but pseudonymous.

Pseudonymity means that a user's identity is not directly tied to their blockchain transactions but rather to a digital pseudonym, typically a public key or a blockchain address. These addresses are like a sequence of letters and numbers, giving privacy but not total anonymity.

In contrast, anonymity would mean that the transactions are entirely disconnected from any identity, even a pseudonym, making them untraceable to the user. Blockchain does not usually provide this level of anonymity because the transaction history of each blockchain address is visible to anyone who accesses the blockchain.

Most blockchains are open ledgers, meaning that all transactions are visible to anyone who wishes to view them. This level of transparency ensures that while users' identities are not directly exposed, their transaction histories and patterns can be analyzed.

While basic blockchain transactions offer pseudonymity, several enhancements and tools can increase privacy:

1. Mixing Services: Services like CoinJoin allow multiple users to combine their transactions into a single transaction with multiple inputs and outputs. This mixing blurs the traceability of any single coin, making it more difficult to link wallets with identities.

2. Privacy-Focused Cryptocurrencies: Some cryptocurrencies, like Monero and Zcash, are designed specifically to enhance privacy. Monero uses ring signatures and stealth addresses to hide the transactions’ origins, amounts, and destinations. Zcash allows users to shield transactions completely through its zk-SNARKs technology, which enables transactions to be verified without revealing the sender, receiver, or amount.

3. Use of Multiple Addresses: Users can increase their privacy by using multiple wallets or addresses, dispersing their transactions across several points, which makes it more challenging to link them to a single identity.

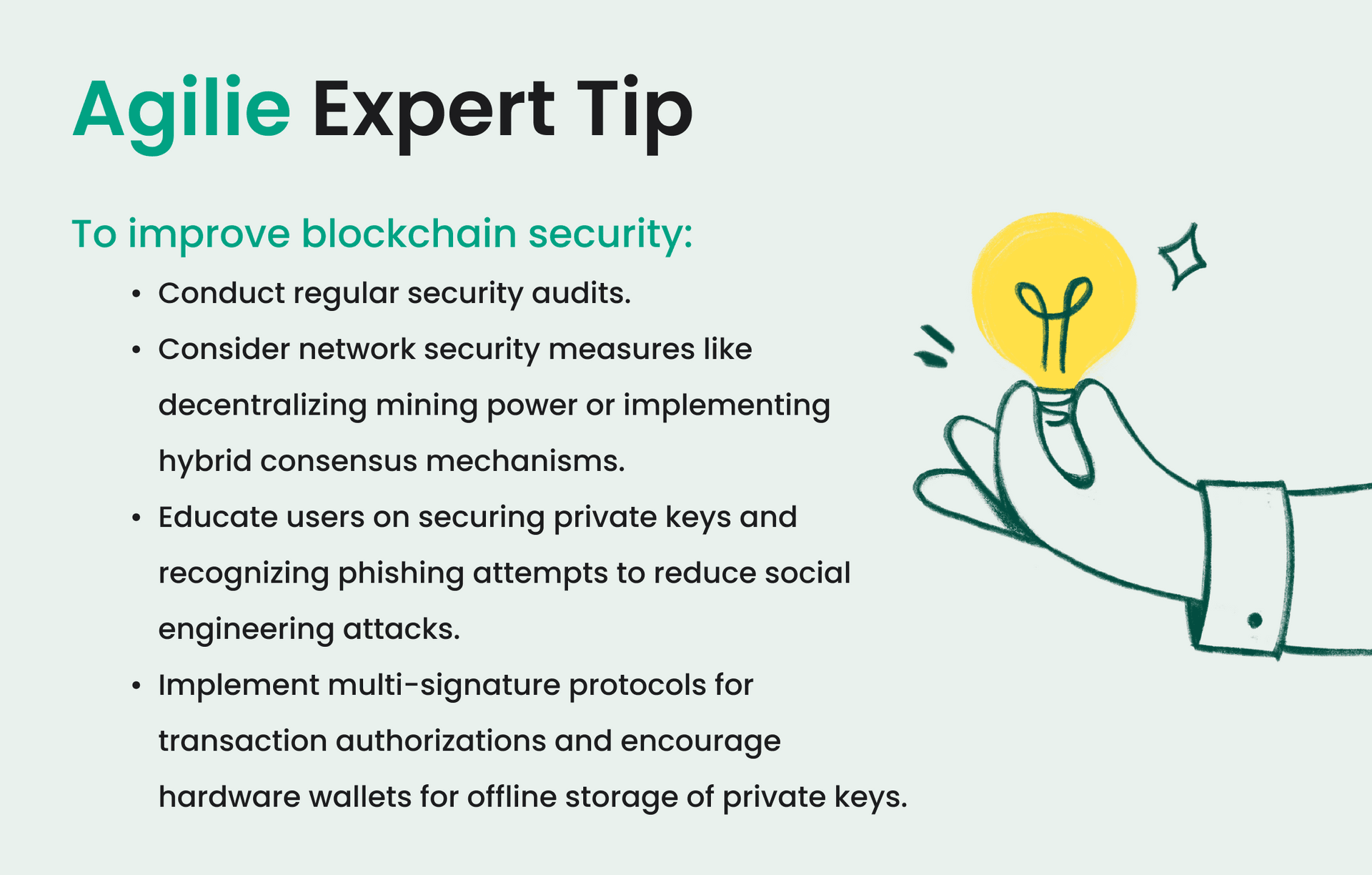

Myth 3: Blockchains Are Unhackable

The idea that blockchains are completely unhackable is a frequently held misconception that can cause a dangerous level of complacency in security measures. While blockchain technology does offer robust security features, it is not immune to vulnerabilities. Knowing the security features employed and the situations in which breaches happen is very important for anyone who wants to use blockchain for their business.

Blockchain technology secures data through several mechanisms:

Cryptography: Every transaction on a blockchain is secured using cryptographic algorithms, which ensure that data can neither be altered nor read without the appropriate cryptographic key.

Decentralization: By distributing copies of the ledger across a network, blockchain reduces the risk of a single point of failure that could compromise the entire system.

Consensus Protocols: Blockchains use various consensus mechanisms, like Proof of Work (PoW) or Proof of Stake (PoS), to agree on the validity of transactions. These protocols prevent a malicious actor from changing even a single aspect of the blockchain.

Learn more about our blockchain software development services.

Learn more about our blockchain software development services.

Despite these security measures, there are scenarios where blockchains can and have been compromised.

Scenarios Under Which Breaches Have Occurred

51% Attacks: This type of attack happens when a single entity gains control of more than 50% of the network’s mining hash rate or stake, allowing them to manipulate transactions and potentially double-spend coins.

Code Vulnerabilities: Smart contracts, which are self-executing contracts with the terms directly written into code, can contain vulnerabilities. One of the most famous incidents is the DAO attack on the Ethereum network. Hackers exploited a vulnerability in the DAO (Decentralized Autonomous Organization) smart contract code to siphon off one-third of the DAO’s funds.

Phishing and Social Engineering: End-user security is often the weakest link in a blockchain system. Phishing attacks can allow attackers access to blockchain assets, bypassing network security measures, to steal private keys or wallet credentials.

Conclusion

The blockchain technology is often seen as highly popular and muddled at the same time. Falsified myths are only part of the misconceptions that can mislead such a fantastic technology. Similarly, proper professional knowledge and strategy can help blockchain perform to its potential in various fields. Building your own cryptocurrency can be a strategic move for businesses seeking to innovate and tap into new digital markets.

At Agilie, we understand that dealing with a complex environment is also a significant challenge. This is why we create powerful blockchain systems and wish to educate our clients regarding the breadth of blockchain-utilizing services. Therefore, such solutions can be tailored to your industry's concrete necessities and problems.

Contact us to find out how our blockchain development services can help you achieve your goal.

Contact us to find out how our blockchain development services can help you achieve your goal.