The fintech sector has shown a rapid increase in the USA since 2012, showing its high market demand. According to Statista, there are 10,412 financial technology companies in 2024 in the USA as compared to 2,881 in 2012. The data are encouraging as services like money transfer, neobanks, and cryptocurrency support truly revolutionize the way people deal with their financial assets.

Nevertheless, regardless of the presented promising statistics, launching a fintech business or specific product on the US market requires considering the major regulations in order to secure the investors and clients and prevent money laundering. Therefore, in the article, we analyze the key fintech requirements and regulation bodies that govern fintech-relevant businesses in the USA.

-

In the US, all national banks and fintech organizations are obliged to ensure the security of clients and investors and prevent money laundering. It is important to clarify that the financial technology companies fall under different regulations, depending on the services they provide (cryptocurrency business or launching payment applications).

-

The USA’s regulatory landscape is divided into the federal and state levels that enact and control regulations on security, money operations, and licensing.

-

Partnering with US banks can ensure that the fintech company receives benefits like reduced licensing obligations and access to Visa/Mastercard payment networks.

Why Are Regulations Important For Fintechs?

Regulatory compliance in fintech plays a central role in determining its overall position in the US market. The key reasons why regulations matter for financial technology are:

-

Customer protection.

-

Market stability.

-

Risk management.

Customer Protection

Customer protection is the key regulatory compliance for fintech, which touches upon but not limited to the payment apps authorization, money transfer, online payment procedures, etc. KYC or Know Your Customer is a regulatory standard, which requires fintech organizations to check and grant the legitimacy of the user’s identity.

CIP (Client Identity Program) is the central customer protection layer of KYC, which obliges fintechs to check the correctness of the user’s identity by analyzing their credentials.

CDD (Client Due Diligence) is the second key layer of KYC, which requires financial technology companies to conduct an in-depth analysis of the client’s behavior to evaluate the potential risk levels and clarify the purpose of transactions.

Market Stability

Market stability is the next reason why fintech regulatory compliance is a must for fintech companies. The US banks, the same as financial technology companies, are obliged to abide by the AML or Anti Money Laundering regulation to prevent financial manipulations. AML comprises the elements of CIP and CDD. Additionally, Anti-Money Laundering involves managing risks on suspicious activities and transactions monitoring:

-

SAR (Suspicious Activity Reporting)

SAR requires organizations to report suspicious transactions that may represent money laundering. SAR relates not only to anti-money laundering but to preventing other types of suspicious activities like financing terrorism and fraud. Financial institutions have the determined requirements and deadlines per report submission.

-

CTR (Currency Transaction Reporting)

CTR is applied not only to banks but to fintechs that deal with cash transactions. These institutions are obliged to provide reports on daily cash transactions which are more than $10.000.

Risk Management

If the financial technology organization launches its business in the US market, then the fintech data regulations like the Enhanced Due Diligence (EDD) of KYC and AML/CTF are a must to prevent risks of illegal financial manipulations.

-

EDD (Enhanced Due Diligence)

This regulatory measure should be applied to high-risk clients as it promotes analyzing their associations with politically exposed people, as well as assessment of the transaction sums to detect whether they are relevant to the high-risk activities. EDD can comprise additional procedures like checking the source of finances and regular transaction monitoring.

-

CTF (Counter-Terrorism Finance Rule)

The Counter-Terrorism Financing Rule puts into perspective the detection and prevention of any attempts of terrorist-relevant organizations to get access to funds.

Hence, fintech organizations have to ensure a decent level of customer protection to prevent market instability to reinforce managing the financial manipulations. But what is the overall regulatory landscape in the US and why does it matter for fintech? Let’s find out.

Understanding the US Fintech Regulatory Landscape

The US fintech regulatory landscape is quite complex, considering the absence of a centralized financial regulator(s). Its key regulatory agents represent the federal companies and state agencies. The parallelism between the federal and state regulatory bodies creates a controversial impact on the fintech industry, as the jurisdictions can reiterate, by generating a two-level system of regulation.

Financial technology companies have to be extremely careful when implementing their digital solutions to the US market due to the importance of legal compliance with federal and state agencies. One essential clarification: state regulations can differ throughout all 50 states, so in order not to get issues with laws, it is essential to be aware of them prior to launching the business there.

Federal Regulations and Compliance

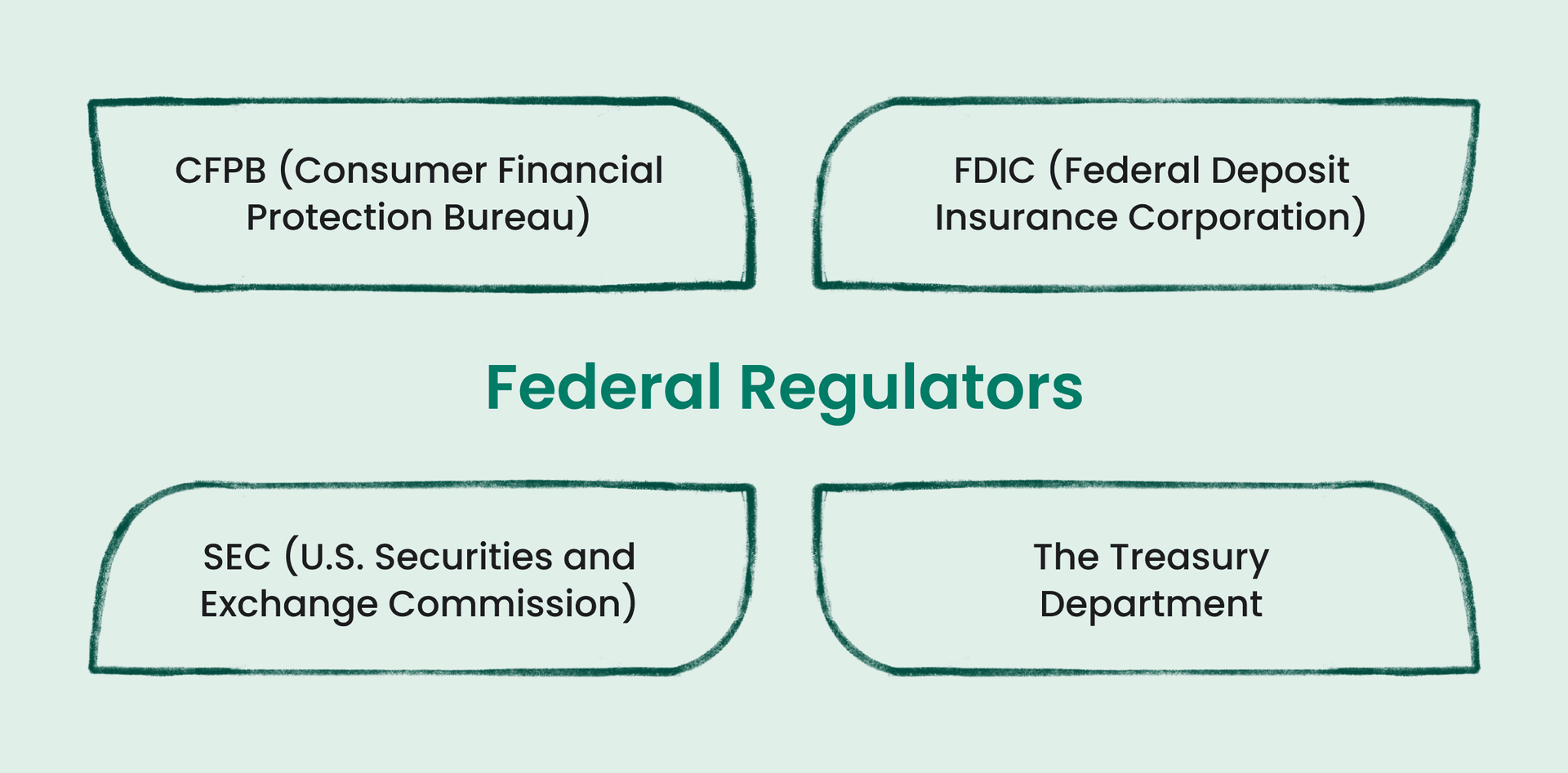

Prior to discussing the key regulations for fintech, let’s dive into the paramount federal companies that promote the national-level regulatory compliance for the fintech companies.

CFPB (Consumer Financial Protection Bureau) is responsible for regulating the national and foreign companies, including fintechs that provide financial services to the US citizens on whether they adhere to the federal consumer protections laws by checking money transfer, lenders, banks, etc.

FDIC (Federal Deposit Insurance Corporation) focuses on lenders and traditional banks that collaborate with the fintech-relevant platforms. The essential clarification is that FDIC does not regulate fintech but their partner banks. This regulatory body regulates the state-chartered banks that are not in the Federal Reserve System.

SEC (U.S. Securities and Exchange Commission) regulates fintech-relevant digital assets like non-fungible tokens and cryptos to guarantee fair financial companies’ practices and ensure the investors’ protection. This federal organization does not regulate all cryptocurrencies, only those that respond to the Howey Test, which the SEC classifies as securities (Solana (SOL), NEAR Protocol (NEAR), Binance Coin, etc.). NFT regulations take into account the aims of their usage and whether they are classified as securities. This regulatory body focuses on fintech abidance by the security laws, so it evaluates additionally crowdfunding.

The Treasury Department is responsible for checking whether the fintech organization adheres to the customer protection laws, as well as focuses on fraud-preventive measures, especially when it comes to anti-laundering.

The aforementioned federal organizations play a central role in governing the following regulations.

The Treasury Department regulates the Bank Secrecy Act (BSA) law on anti-laundering, requiring the financial institutions of the US to help the US federal agencies in detecting the individuals who want to circumvent the US financial system and preventing money laundering. BSA requirements include reporting cases when the daily aggregate surpasses $10,000, as well as when the fintech company detects tax evasion.

Ruled by the Consumer Financial Protection Bureau, the Truth in Lending Act (TILA) analyzes the correctness of credit reporting. This act prevents unfair credit billing and inaccurate credit card practices. To ensure compliance with TILA, lenders who can use fintech loan apps or peer-to-peer lending apps are obliged to provide clients with the loan cost information, specifically relevant fees and charges.

The Equal Credit Opportunity Act is regulated by the Consumer Financial Protection Bureau and makes lenders liable in the case of any form of racial, color, religious, sex, age, disability discrimination etc. against the application. Additionally, the act prohibits creditors from misusing the public assistance program as a means of income generating.

The State-Level Regulations

Although state-level regulations can overlap with the ones of the federal agencies, each of the 50 states has its own regulatory body that focuses on controlling the financial institutions’ and fintechs’ abidance by the state financial laws, consumer protection, investment & trading regulations, etc. It is possible to define the key categories of the identified regulators.

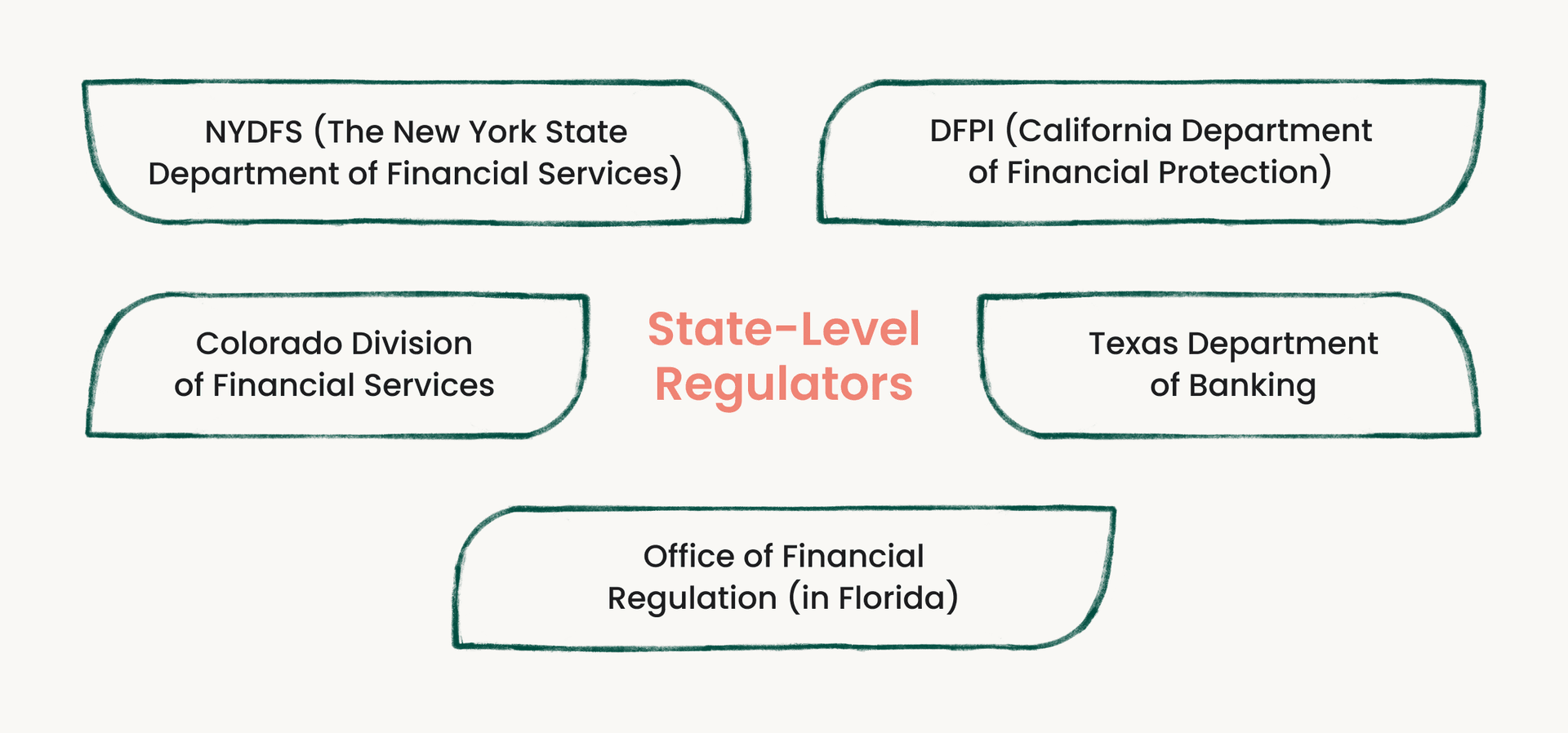

State Banking Regulators or agencies that focus on regulating the fintech companies’ state-chartered banks’, and credit unions’ adherence to the state financial laws and regulations of consumer protection. Additionally, State banking Regulators ensure the licensing of the fintech companies that perform money transfers and digital financial services. The instance of the identified regulatory body is The New York State Department of Financial Services (“NYDFS”).

NYFDS imposes new obligations on banks and fintechs regarding cybersecurity support and maintenance. The obligation (Dec. 1, 2023) sets new reporting rules for the presented parties to report the cases of ransomware or extortion payment associated with cybersecurity events within 24 hours of the case occurrence. Additionally, banks and fintechs have to provide a written description to clarify whether and why the payment was necessary, as well as efforts made to find alternatives to manage to comply with the new rule within 30 days of payment.

State Securities Commissions aim to analyze the activities of the market participants, including fintech, that are relevant to investment and trading. The focus of this regulatory body is analyzing security in the aforementioned participants’ activities.

The California Department of Financial Protection and Innovation (“DFPI”) represents an example of a state-level regulator that puts into perspective the protection of investors and checking the fairness of practices by analyzing the operations of California brokers and investment advisers.

California’s Digital Financial Assets Law (Jul. 1, 2025) will require California residents or individuals who want to launch their digital finance asset business in the state of California to get a license from the California Department of Financial Protection and Innovation. The major regulatory requirements represent compliance with disclosure and annual reporting. California’s Digital Financial Assets Law regulates those crypto assets that do not fall under the SEC regulations, like Bitcoin and Ethereum, which are viewed as digital commodities, not securities.

State Licensing Authorities, like the Texas Department of Banking issue licenses and regulate fintech on their abidance by the Texas licensing requirements. The Act 1666 obliges the providers of digital assets to adhere to the specified provisions in order to maintain the money transmission license that comprises the commingling of funds, requirements of accounting, and annual reporting, as well as ensuring clients’ access to their funds.

The Office of Financial Regulation is a key state-level regulator in Florida, which aims to prevent unlicensed activities and criminal financial manipulations. FL Stat § 559.952 launches a Financial Technology Sandbox where the fintech organizations can test their cryptocurrency-relevant products under the license period. This regulation does not require a money transmitter license within the mentioned period.

By regulating the state-chartered Credit Unions and Savings and Loan Associations, the Colorado Division of Financial Services emphasizes consumer protection regarding the financial monitoring process.

According to exemption IV of § 11-51-308.7. Colorado Digital Token Act (Part 3 - Registration of Securities and Exemptions), the digital tokens can be used only for the consumptive purpose, or when the client aims to get a product or services while investment aims are unacceptable. This matters to avoid speculations.

Fintech Collaboration with Banks

Prior to analyzing the benefits and challenges of the fintech-bank partnership, it is important to discuss the basics of licensing for fintechs in the US landscape.

-

Regulatory Sandbox. This fintech requirement implies the company’s testing of its services under controlled regulatory guidance in both federal and state landscapes within a limited predefined time. Finally, it is worth mentioning that not all states/federal regulators and fintech companies can take part in the regulatory sandbox.

It is worth clarifying that not all states and federal regulatory bodies implement regulatory sandbox.

-

Adherence to the Regulatory Frameworks. Fintech company has to comply with Anti-money laundering (AML), counter-terrorism financing (CTF), and KYC (Know Your Customer) regulations, same as guaranteeing security measures to ensure that their financial operations are error-free, ensure encrypted transactions, record and report suspicious financial activities, and provide tech-savvy idea verification service. It is important to note that if the fintech company works in the US but provides services to the European Union citizens, it should comply with GDPR (General Data Protection Regulation), depending on the service type.

-

Adaptation to the Regulatory Changes. If the fintech organization launches its business in the US it has to keep up with the alterations in the regulatory environment to keep client’s protection and ensure its awareness of the daily aggregate norms if they change to prevent money laundering.

Based on the three analyzed factors, launching a fintech product or service is a challenging task in the US legal environment, which makes collaboration with banks an optimal variant of reducing licensing obligations.

The reason is quite transparent - the national bank that is licensed is regulated by:

-

The chartering authority (federal or state level).

-

Certain statutes of the Federal Deposit Insurance Act if it gets the deposit insurance.

-

Federal Reserve, as a primary federal supervisor if the bank is a member of the Federal Reserve System.

Additionally, as a Bureau of the Treasury Department, OOC is responsible for chartering national banks. It supervises all national banks on regulatory compliance, as well as checks all the bank’s mergers and branches.

From this point, if the fintech company collaborates with the bank, the licensing obligations are reduced as the organization plays the role of the solution provider, while a bank is a sort of a ‘sponsor.’ Some fintech businesses can have a little track record or run an unusual business model, which might not guarantee their regulatory compliance on state/federal levels, leading to the rejection of their license. The bank covers the required licensing elements like track record, record keeping, AML, TILA, CTF, and KYC, which makes the fintech company a digital service provider.

The bank-fintech collaboration promotes a range of mutual benefits.

From the Fintech’s Side:

-

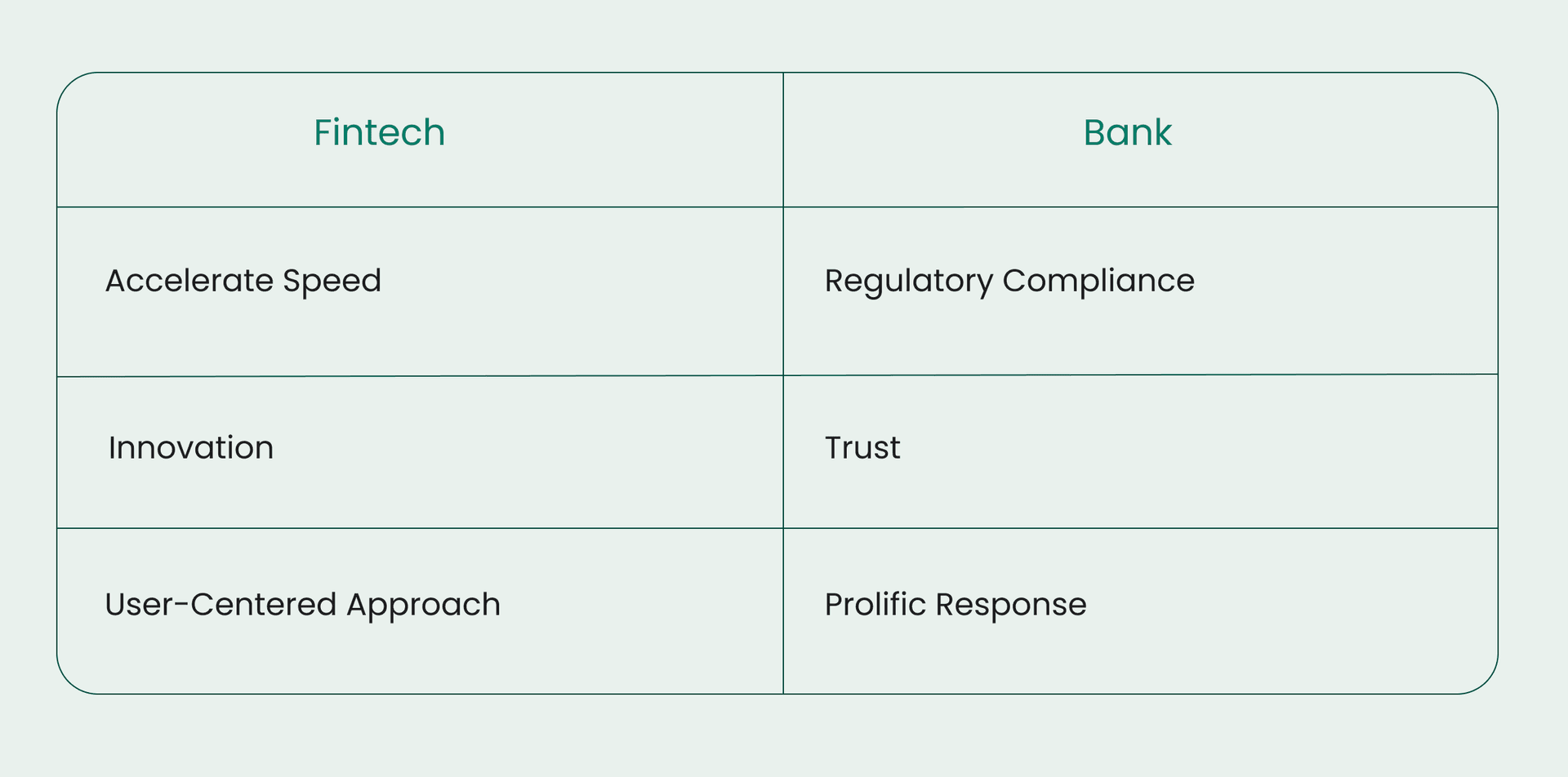

Accelerate Speed

Fintechs are masterminds in the digital real-time payment solutions, which can minimize the transaction time. This linked article presents key insights on the fintech app development process.

-

Innovation

Financial technology companies tend to craft new digital solutions by integrating blockchain and AI as means of security reinforcement, optimized user experience, and analytical predictions.

-

User-Centric Approach

Fintechs put into perspective customer impressions and behavioral patterns to provide them with the most optimal personalized recommendations, guidelines, and offers. Involving features like rewards and gamification can boost client attraction and brand recognition due to the personalization of services and recommendations.

Summing up, the bank can accelerate its performance, boost user-centricity through personalization, and diversify its services with AI prediction functions.

From the Bank’s Side:

-

Regulatory Compliance

The banks are responsible for setting relationships with the regulatory bodies (of state and federal levels) and guaranteeing compliance with anti-fraud, financial regulations, AML, and KYC.

-

Trust

The banks win reputation and trust among the public and regulatory bodies.

-

Prolific Response

When it comes to crimes, the banks have well-established protocols to provide a fast response to financial crimes.

Summing up, fintech can benefit from the bank due to its trust and relationship with regulatory bodies, which economizes the time needed to generate a reputation, by enabling it to focus on developing and implementing solutions.

Challenges of Partnership between the Banks and Fintech

Regardless of the promising benefits banks and fintech provide each other with, it is important to discuss the fintech regulatory issues and challenges of such a partnership.

-

Reputational Risk

If the fintech company launches a defective product, which might cause security-relevant problems like incorrect crediting and money fraud, the bank will suffer reputational damage, affecting its licensing

-

Differences in Cultural Approaches

Difference in cultural approaches may cause client confusion and dissatisfaction because of the potential absence of service synergy. While the fintech companies can focus on a more modern UX/UI design and approach to treating the customers, the banks can keep their conservative, well-defined method, leading to misunderstandings.

-

Regulatory Compliance

As the bank is responsible for handling all licensing requirements, the fintech company might not be aware of the details of the bank’s regulations, which, in case of violation, will provoke regulatory risks to the bank.

Hence, although the partnership between fintech and banks might be fruitful for both parties, the aforementioned challenges might disrupt its effectiveness and provoke unfavorable results.

This article can expand your knowledge ofon the challenges associated with digital banks.

This article can expand your knowledge ofon the challenges associated with digital banks.

Payment Network Access

In the US, the inquiring bank has to be a member of Visa and Mastercard networks to be able to work on the card transactions. The key challenge for fintech companies is that only the member bank of the network can issue Visa or Mastercard cards.

In order to have the possibility to ensure financial transactions with Visa and Mastercard, the principal fintech compliance regulation requires financial technology companies to collaborate with the bank that is a member of this payment network. The key point to take into account is that, initially, it is the member bank that has to acquire and settle the funds that the fintech company can circulate within the services it offers to the banks and merchants.

Finally, regardless of intense dependence on the bank for the payment network, the fintech company can play the role of the marketplace by transferring money from the acquired bank to the seller.

Safeguarding Funds at USA Banks

Now it’s time to discuss the importance of keeping financial input secure in the USA banks and analyze fintech’s function. It is important to mention that the Federal Deposit Insurance Corp. (FDIC) will safeguard the depositor from bank failures. The essential points to keep in mind are:

-

FDIC safeguards the funds only if the bank is FDIC-insured. Therefore, fintech companies can offer their services like checking/savings accounts when collaborating with the FDIC-insured banks to get the client’s funds protected.

-

The limit of FDIC protection is $250,000 per depositor.

According to the Federal Deposit Insurance Corporation, non-bank organizations never get FDIC insurance. From this point, partnering with fintech companies requires scrutiny to understand whether they will partner with non-FDIC-insured banks or with FDIC-insured ones. The key exception is that if the fintech company collaborates with the FDIC-insured bank, then the $250,000 FDIC safeguard limit will be applied in the case of the bank’s shutdown. For instance, the fintech company Chime provides clients with the opportunity to use checking and savings accounts, as well as debit cards, which are federally protected as the company collaborates with the FDIC-insured Bancorp Bank or Stride Bank.

Strategies to Mitigate Risks of Bank Failures

Although bank failures are not a common process, default,, and tough economic situations can put the overall user’s savings at stake. So, to get the clients informed, here are a few strategies on how to reduce the risks of potential bank failures:

-

Consider Only Insured Accounts

It is important to know that FDIC financially insures only checking and savings accounts. Some retirement accounts, like IRAs, fall under the insured category. Additionally, FDIC secures money market accounts and certificates of deposit (CD).

Please note that if the client invests money in stocks, mutual funds, life insurance policies, etc., FDIC will not cover that.

-

Apply Different Account Categories

As was mentioned above, the FDIC insures a depositor with $250,000, which applies to each account category. Those categories include single trust, joint trust, living trust, etc. The client can have a single-owner account, which will have $250,000 insurance. But, if they are married, they can create a $250,000 joint-owner account with their spouse, leading to the $1 million FDIC insurance coverage in total.

-

Pay Attention to the Account Balance

It is extremely important for the users to keep an eye on their account balance, especially if their finances go beyond $250,000 in order to check whether the sum does not exceed the coverage limits. For this purpose, the Electronic Deposit Insurance Estimator (EDIE) will help evaluate the balances.

Cryptocurrency Regulation

Cryptocurrency-relevant activities like trade, exchange, and creation face stringent federal control considering the enhancement of the fraudulent activities considering the cryptocurrency assets, failures of the from-scratch cryptocurrency development, and violation of the investors’ protection.

SEC (U.S. Securities and Exchange Commission) accuses Colorado-based Gold Hawgs’s Paul Garcia of violating 17(a)(1) and (a)(3) of the Securities Act of 1933 and Section 10(b) of the Securities Exchange Act of 1934 and Rules 10b-5(a) as they performed a fraud considering cryptocurrency manipulations and failure to protect the investors.

The key cause of damage was that the defendant got $400,000 of investment to create a new cryptocurrency from scratch, but when the coin offering failed, the COO, Garcia stole $123,000 raised from investors and transferred them into another company.

The case of Garcia was one of the legal instances that led to tightening the regulation of cryptocurrency in the US, which was related not only to crypto ventures from the investors’ standpoint but also to bringing transparency when selling this digital asset to the public.

The key federal regulators worth mentioning are the SEC and the IRS, which aim to control the buying and selling of cryptocurrency digital assets to prevent manipulations and fraudulent activities.

The SEC

By categorizing crypto as securities under the Howey test, the SEC regulates the issuing company’s registration of all sales of the identified digital assets. This tightens the run of crypto in the US and the fintech compliance, as the presented federal regulatory body aims to make cryptocurrency abide by the same rules as the publicly traded companies in order to ensure buyers with transparency on the potential risks. You might be interested in the characteristics of crypto exchange app development to save your digital assets.

It is important to clarify that although cryptocurrency falls under the regulations, the federal regulator, SEC controls only those crypto that are considered securities according to Howey Test. The regulations can vary for the decentralized crypto assets.

The IRS (Internal Revenue Service)

The IRS categorizes crypto as a property, imposing a tax on a person when they purchase or sell this digital asset. When the client decides to sell cryptocurrency for more than they bought it originally, then they will have to pay capital gain tax. Investors should remember the possibility of a tax event, which can be provoked by selling and buying crypto. The tax event requires them to report on their annual tax returns to avoid crypto speculations.

Internal Revenue Service issues the final regulation, which tightens the crypto-relevant activities as it obliges brokers like the digital asset hosted wallet providers, operators of the custodial digital asset trading platforms, etc., to provide reports on the clients who sell their digital assets. The underpinning motives for this regulation are:

-

IRS aims to detect cases when individuals use crypto to hide the taxable income in order to prevent non-compliance with the tax reporting, which tightens fintech regulations.

-

The brokers take possession of the crypto; the clients aim to sell as these intermediaries make most of the selling operations. For this purpose, the final regulation is applied to check taxpayers.

Explore how to protect your cryptocurrency assets and craft a crypto wallet.

Explore how to protect your cryptocurrency assets and craft a crypto wallet.

Challenges of Establishing Banking Relationships for Cryptocurrency Businesses

Regarding the aforementioned cases of stringent regulations on cryptocurrency and the case of fraudulent crypto vendor manipulation, the banks experience challenges in integrating into their list of services.

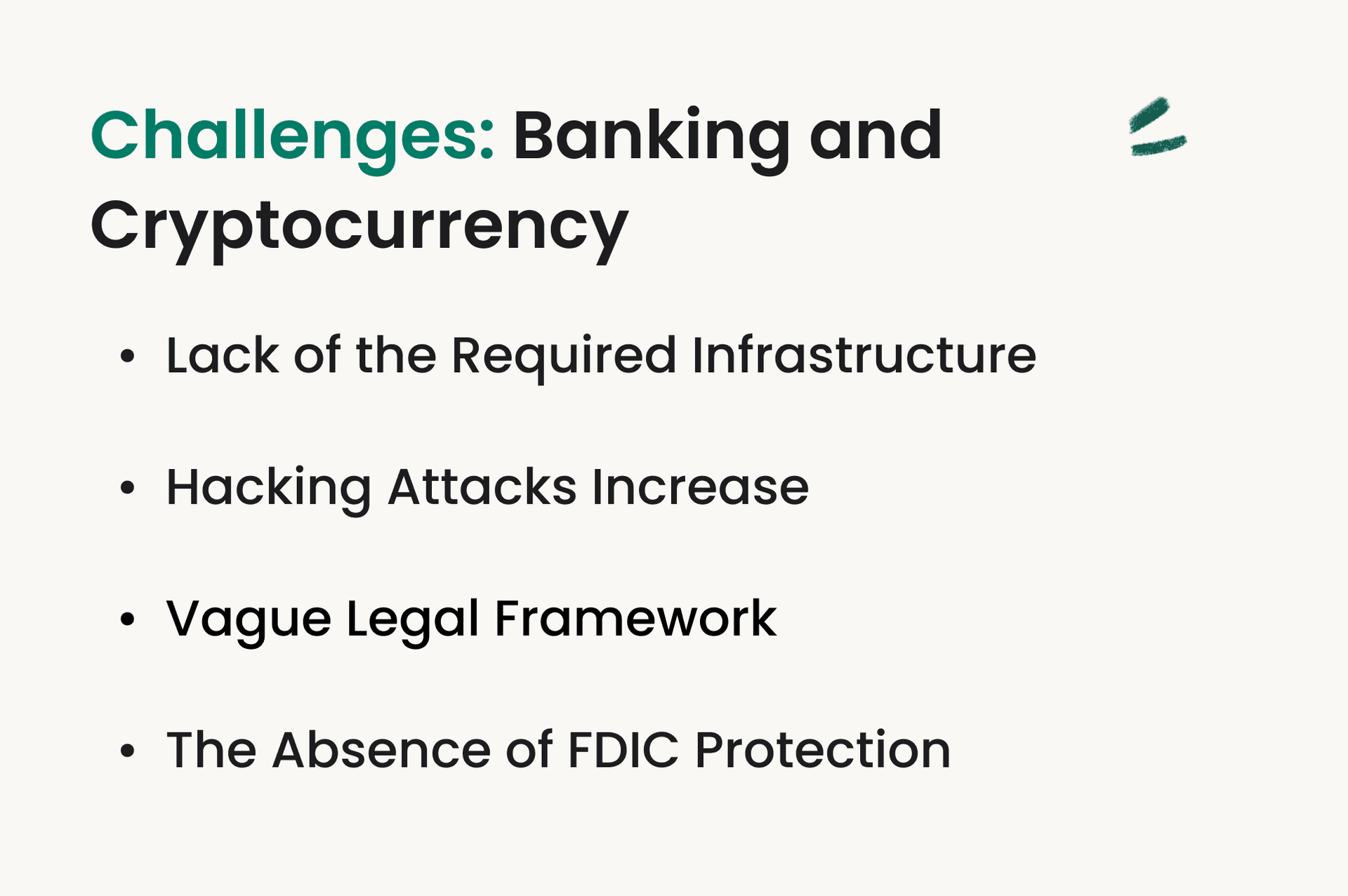

1. Lack of the Required Infrastructure

This challenge indicates that banks can face complexities with investment into the required technological equipment and keep their regular updates, which might incur monetary losses and hinder their legal reputation due to the lack of trained specialists that can monitor crypto circulation.

2. Hacking Attacks Increase

This challenge makes US banks skeptical about implementing cryptocurrency, as the lack of the technological infrastructure and skilled personnel presented above might undermine their ability to detect and prevent hacking attacks.

3. Vague Legal Framework

Regardless of the presented SEC and IRS attitudes to regulating cryptocurrencies, the chance of money laundering remains high, regarding more legal transparency in preventing and covering fraudulent crypto activities. The banks’ implementation of Know Your Customer and Anti-Money Laundering protocols can, indeed, prevent traditional money laundering. However, there might be legal challenges regarding the control over the decentralized networks.

4. The Absence of FDIC Protection

Even if the bank is FDIC-insured, it will not be able to secure the cryptocurrency assets because crypto is a non-deposit product.

Hence, the aforementioned challenges and stringent legal regulations cause complexities for the fintech companies to run cryptocurrency services in the US market and offer them to the partnering banks.

How Agilie Can Assist You in the Development of Your Fintech Product

It is important to understand the legal environment of the US to launch a fintech-relevant business or integrate financial technologies to optimize the existing project or product. Knowledge of how to choose the right development partner is of no less importance in order to ensure the business with the best digital solutions. The key aspects worth considering here are the duration of the firm’s existence on the market, domains of expertise, and the versatility of its services. You may find the characteristics of a fintech development company that prove its reliability in the linked article.

Agilie is an outsourcing organization that crafts result-driven technological solutions for organizations to elaborate on projects from scratch or optimize existing products with the niche IT specialists’ profound expertise. For 14 years, the organization kept evolving by presenting its unique digital services applied in the real estate, fintech, marketing, and e-commerce domains, proving the reliability of Agilie as a development actor.

Agilie offers the following fintech software development services:

-

Payments (applications for payment, money transfer, and software for payment automation).

-

Blockchain (decentralized financial apps, smart contracts, cryptocurrency wallets, applications for crypto exchange and trading, etc.).

-

Mobile banking development services (financial planning, notification center, system user management, card issuer integration services, software security, etc.).

Conclusion

The legal environment in the US is quite complex considering the evolving regulations on the fintech companies’ functionality and service provision. Abidance by federal and state regulations is a must to protect users and investors from money laundering. Nevertheless, fintech regulatory requirements like partnering with banks can optimize fintechs’ operations, especially when it comes to Visa and Mastercard. 4 Things to Know About Fintech Requirements in the USA | Agilie

The crypto market requires scrutiny attention, considering the tightening regulations on selling and buying, while banks don’t hesitate to deal with crypto based on the vague regulatory environment. Finally, regardless of the regulatory environment, the US organizations keep looking for reliable fintech partners to collaborate on multiple security, payment, and money transfer solutions.

Wanna make your fintech project tech sophisticated and attractive? Just contact us to cooperate!

Wanna make your fintech project tech sophisticated and attractive? Just contact us to cooperate!