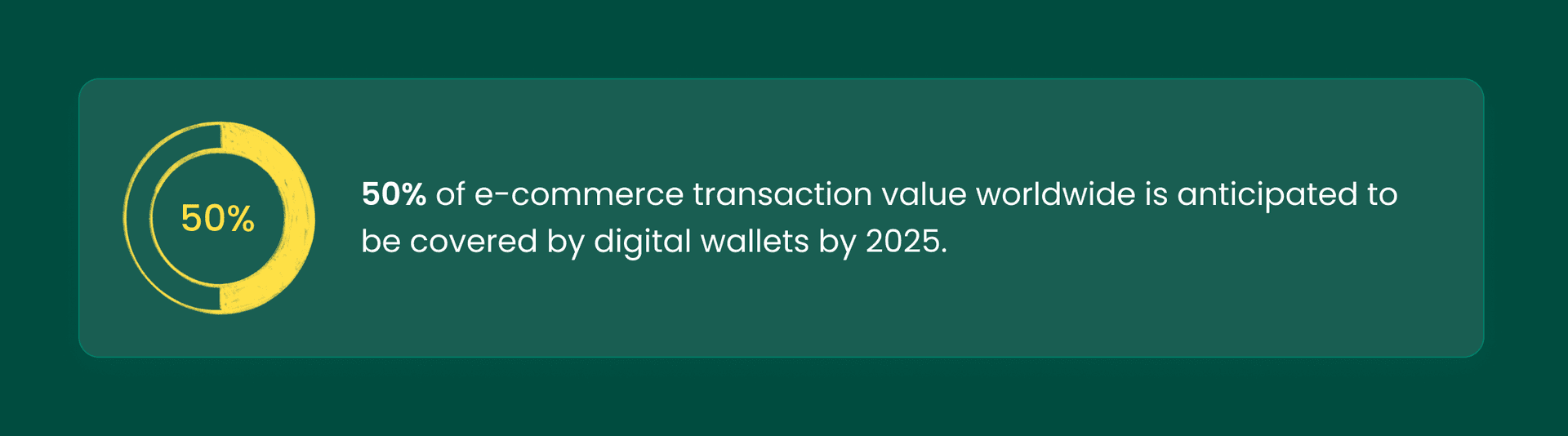

Digital wallets are now an essential part of the modern payment landscape. Fintech organizations, banks and startups all vigorously pursue this advancement in technology due to its convenience, speed, and global applicability. Digital wallets complement traditional payment processing by supporting online purchases, peer-to-peer payments and omnichannel retail experiences.

According to J.P. Morgan, 56% of consumers indicate strong intention to use digital wallets for online payments while opting for in-store pickup. Based on these advantages, digital wallets are growing rapidly in popularity, so in the article we discuss their types and how digital wallets work.

-

Fiat-based digital wallets are primarily defined by their network’s scope, ranging from closed-loop systems accepted via a limited partner network to open wallets that provide almost universal acceptance.

-

Crypto-based digital wallets are distinguished by who controls users’ private keys, thereby defining ownership of assets.

-

Digital wallets represent a strategic tool that can be built using cost-effective white-label solutions and monetized through various methods, including transaction fees, subscriptions, etc.

What Are the Main Types of Digital Wallets?

Let’s explore the principal types of digital wallets, underlining their use cases, advantages, disadvantages, and examples.

Open vs. Closed vs. Semi-Closed Wallets

There are different types of digital wallets based on their fiat or crypto payment processing. Let’s start with the open, closed, and semi-closed wallets.

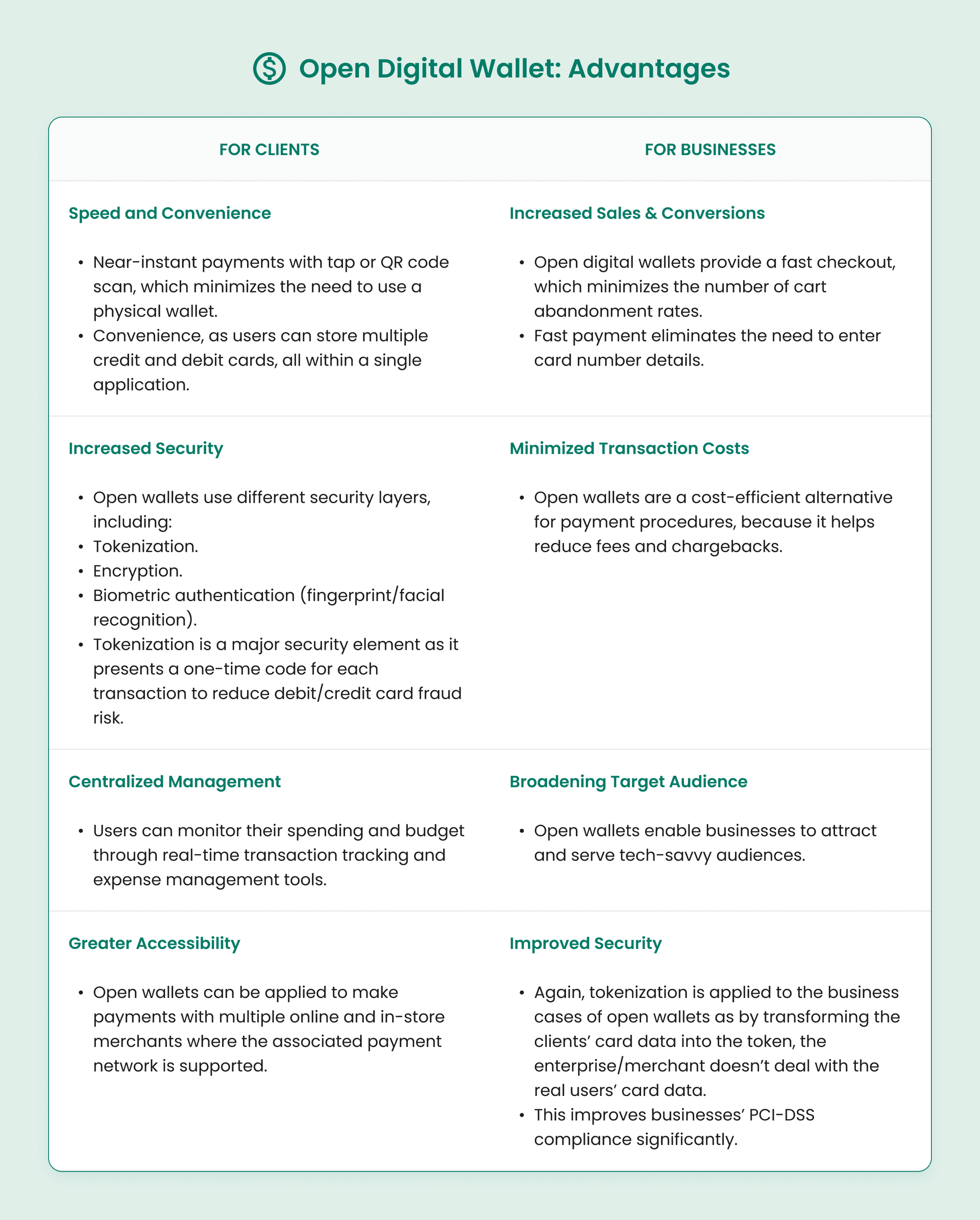

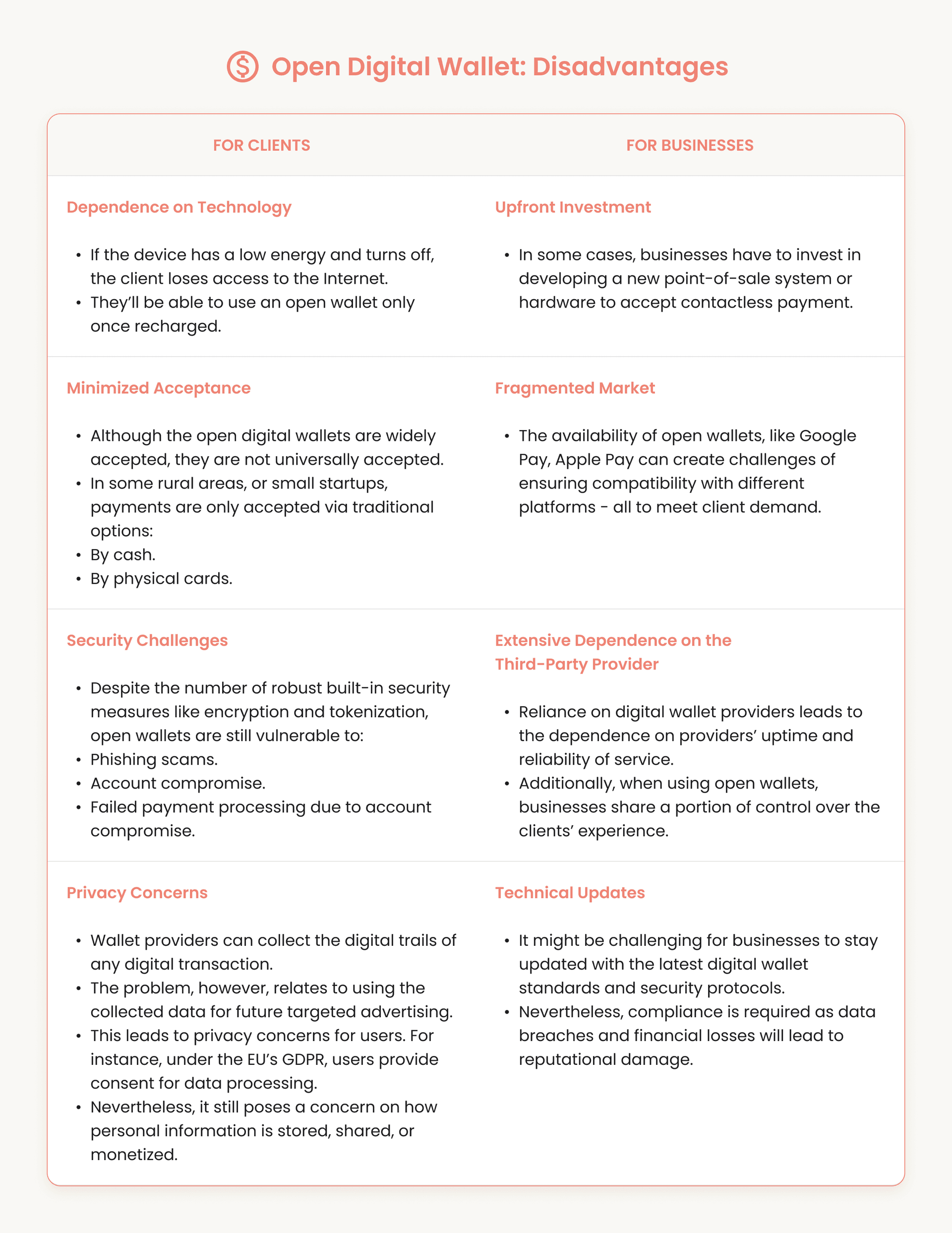

Open Digital Wallets

Open digital wallets, or electronic wallets, rely on fiat currency because they tend to be widely accepted by various entities and are not affiliated with a specific organization or vendor chain. They are designed to be broadly compatible with banks and merchants in many geographical areas. Examples include:

-

Apple Pay: is Apple's original open digital wallet applicable only to the devices of this trademark (iPhone, Apple Watch, Mac). By utilizing NFC payment technology, Apple enables instantaneous payments supporting millions of merchants worldwide. The Apple Pay open digital wallet does not align with a specific brand, enabling users to conduct contactless payments for any product/service that supports digital wallet as a payment method.

-

Google Pay: is Google's open digital wallet compatible with Android devices. Just like Apple Pay, this wallet supports NFC and transaction tokenization to promote fast and secure payments. Google Pay enables in-store payments and in-app purchases. Finally, this open digital wallet is P2P, enabling users to send and receive funds.

Open Digital Wallet: How Does It Work?

-

Account Creation

First, the client has to add their payment card by entering card details. Then, the wallet sends this information to the issuing bank. The bank verifies the card and can require additional authentication, including an SMS code.

-

The Role of Tokenization

Once confirmed, the wallet stores a digital token that replaces the actual card number. The wallet’s system does not operate on actual card data. The token is specific to the user's device and has no monetary value if the device is stolen. The tokenization system, managed primarily by payment networks in coordination with the issuing bank, ensures that the wallet processes transactions without exposing sensitive card information.

-

Making a Transaction

When the client wants to make a transaction, they first have to authenticate their identity using a fingerprint, facial recognition, or a PIN.

Then, for data transmission, the device uses NFC to wirelessly send the encrypted payment token to the merchant’s contactless terminal. For online and in-app purchases, the wallet provides the token instead of the actual card number.

The network maps the token back to the card credentials preserved in the token vault and forwards the authorization request to the issuing bank. The bank validates the transaction, including funds, authentication, and account status, and sends an approval or decline through the same path.

The entire process is near-instant, so the client receives an instant confirmation or a transaction decline.

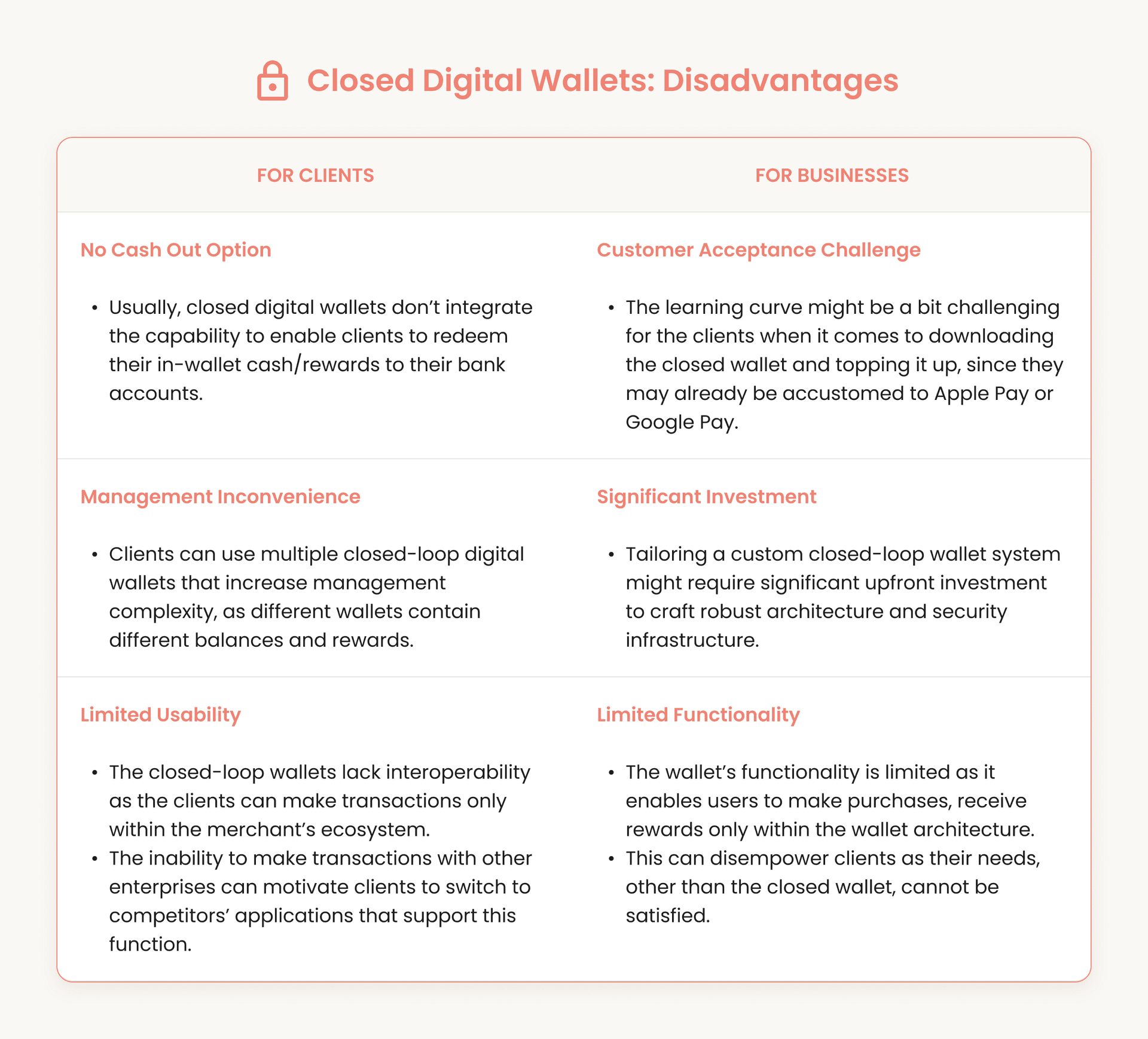

Closed Digital Wallets

A closed e-wallet refers to a specific business, enterprise, merchant, or brand that can be used only for transactions within this ecosystem. For instance, if it’s a fitness club, the user can top up fiat money to pay for sports-specific services/products, but cannot transfer finances for other services that are not related to this specific fitness club or chain of clubs. Examples include:

-

Starbucks App: users can top up their Starbucks wallet and use funds exclusively for food and beverages within the ecosystem. The application integrates the Starbucks Rewards program to automatically apply and track loyalty points in the user’s wallet.

-

Walmart Pay: this wallet is designed exclusively for the Walmart ecosystem. Users can pay for in-store and website purchases, as well as at physical store checkouts. If it’s an in-store purchase, the Walmart application will generate a QR code for the user to scan at the register. This will facilitate the transaction, using payment methods linked to the Walmart account.

Closed Digital Wallet: How Does It Work?

-

Account Setup

The user downloads the merchant’s application and creates an account. This action provides them with access to the company's ecosystem.

-

Account Top Up

The user tops up their account via traditional payment methods, including debit/credit card or bank transfer. The loaded funds cannot be withdrawn; they represent the digital balance with the merchant's ecosystem.

-

Payment & Verification

When initiating payment, the clients use the wallet’s built-in feature, such as displaying a QR code or a scannable barcode. Then, the merchant's point-of-sale system will scan the code and send it to the organization’s internal servers for real-time verification. Once validated, the funds are deducted from the client’s prepaid balance.

Interesting Details

-

The Absence of Intermediaries

Closed wallets operate via the closed loop as the transactions don’t pass through the external payment networks, including Visa, Mastercard, or a banking institution. The merchant’s ecosystem completes the entire transaction cycle internally.

-

Rewards and Refunds

The system will maintain the funds in case of a refund or reward to incentivize clients to make further purchases within the merchant’s ecosystem.

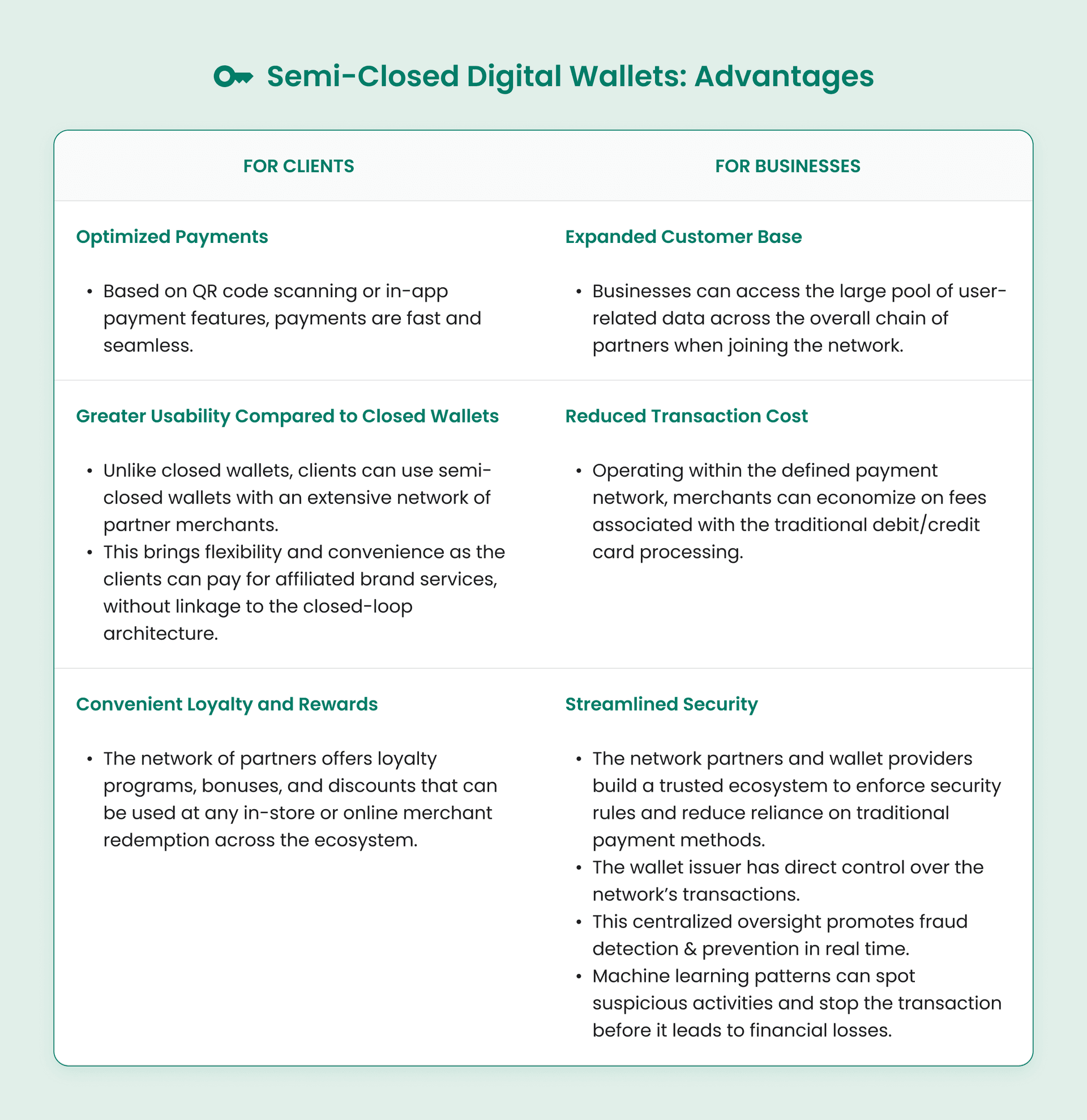

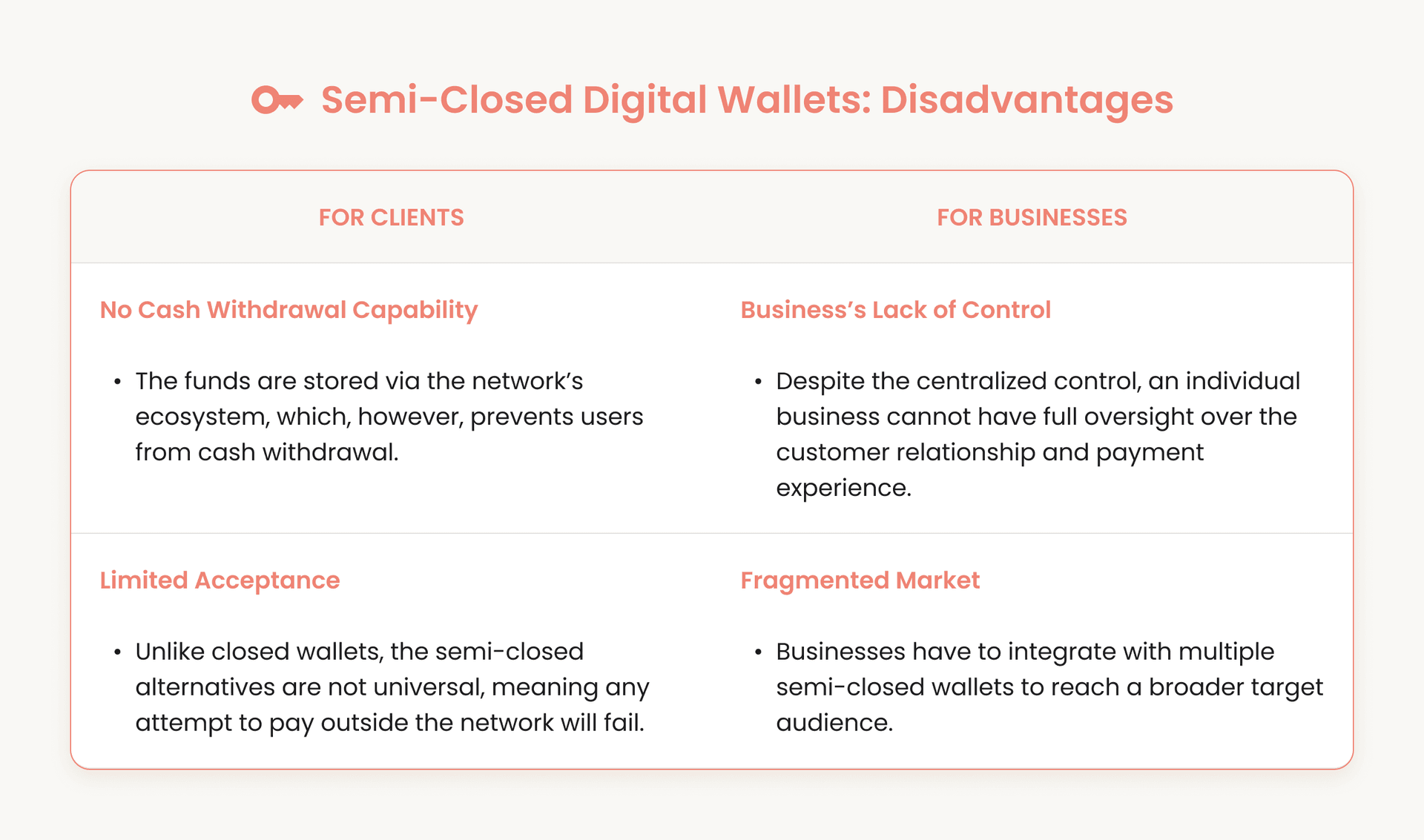

Semi-Closed Digital Wallets

This virtual wallet type operates with fiat funds and can be used across a chain of vendors who partner with digital wallet providers, making it the best option for local shopping. Here are a few examples of semi-closed digital wallets:

-

Paytm (India): the wallet can be used to pay for a spectrum of services, including utility bills, travel bookings, and online shopping at various physical retail stores partnered with Paytm. This semi-closed wallet is regulated by the Reserve Bank of India and enables spending via an extensive partner network, but it does not allow direct cash withdrawals.

-

WeChat Pay (China): WeChat Pay is a part of China’s ‘super app’ ecosystem that supports a wide range of actions, such as bill payments within a single application. WeChat Pay functions more like a fully regulated open mobile payment system under the control of the People’s Bank of China, yet it’s formally a semi-closed wallet.

Semi-Closed Digital Wallet: How Does It Work?

-

Account Setup & Funding

A non-bank financial entity or a banking institution can issue a semi-closed wallet. Users can top up the wallet by using multiple sources including debit/credit cards, and bank accounts. The stored balance is held by the wallet issuer, but the client can use it for spending within the network of merchants and service providers authorized by the issuer.

-

Authorized Merchant Network

When it comes to semi-closed wallets, the wallet provider partners with a network of merchants, which can include online shops, physical stores, and service providers. The wallet will be valid only within this chain of authorized partners.

-

Payment Processing

When paying for a product or service, the wallet provider’s network will proceed with the transaction. Semi-closed wallets support a variety of payment methods, including QR code scans, e-commerce sites, and mobile-to-mobile transfers. The payment is near-instant and seamless as the wallet provider manages both user balances and merchant settlement with its system.

-

No Bank Transfer

While it is possible to fund semi-closed wallets from debit or credit cards and link them to bank accounts, it’s impossible to withdraw cash from ATMs or send that money to other bank accounts. The clients are required to use the balance of the semi-closed wallet to purchase goods or services from merchants in the wallet provider's network of authorized merchants.

-

Regulatory Oversight

It should be noted that semi-closed wallets exist within different levels of regulatory oversight. Wallet providers will have restrictions on ensuring their consumers operate with KYC (Know Your Customer), AML (Anti-Money Laundering), and data protection standards to ensure safe and legal operations.

Custodial vs. Non-Custodial Wallets

Custodial and non-custodial wallets serve cryptocurrency flows. Let’s discuss in detail the uniqueness and differences between custodial vs non-custodial wallet types.

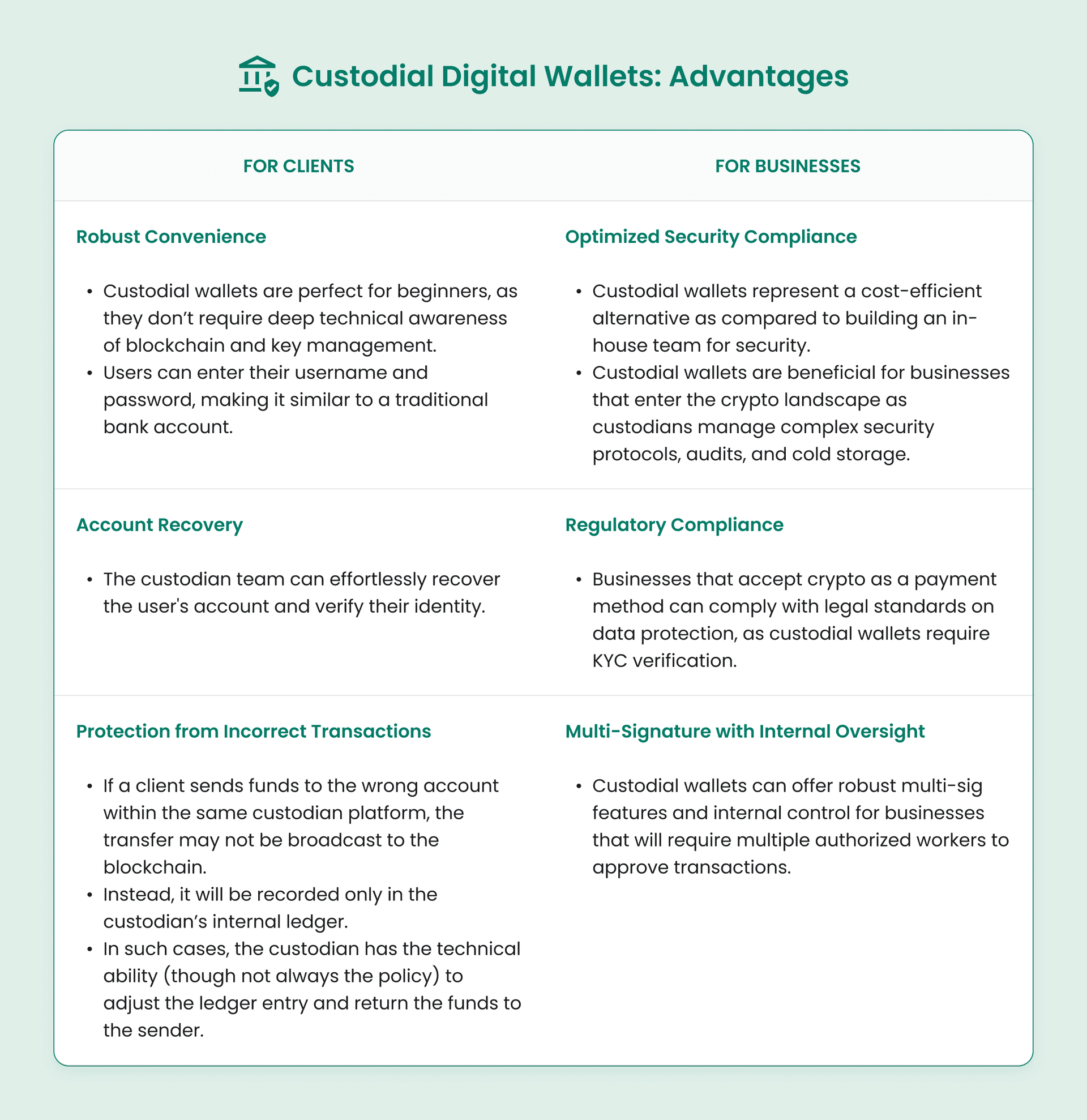

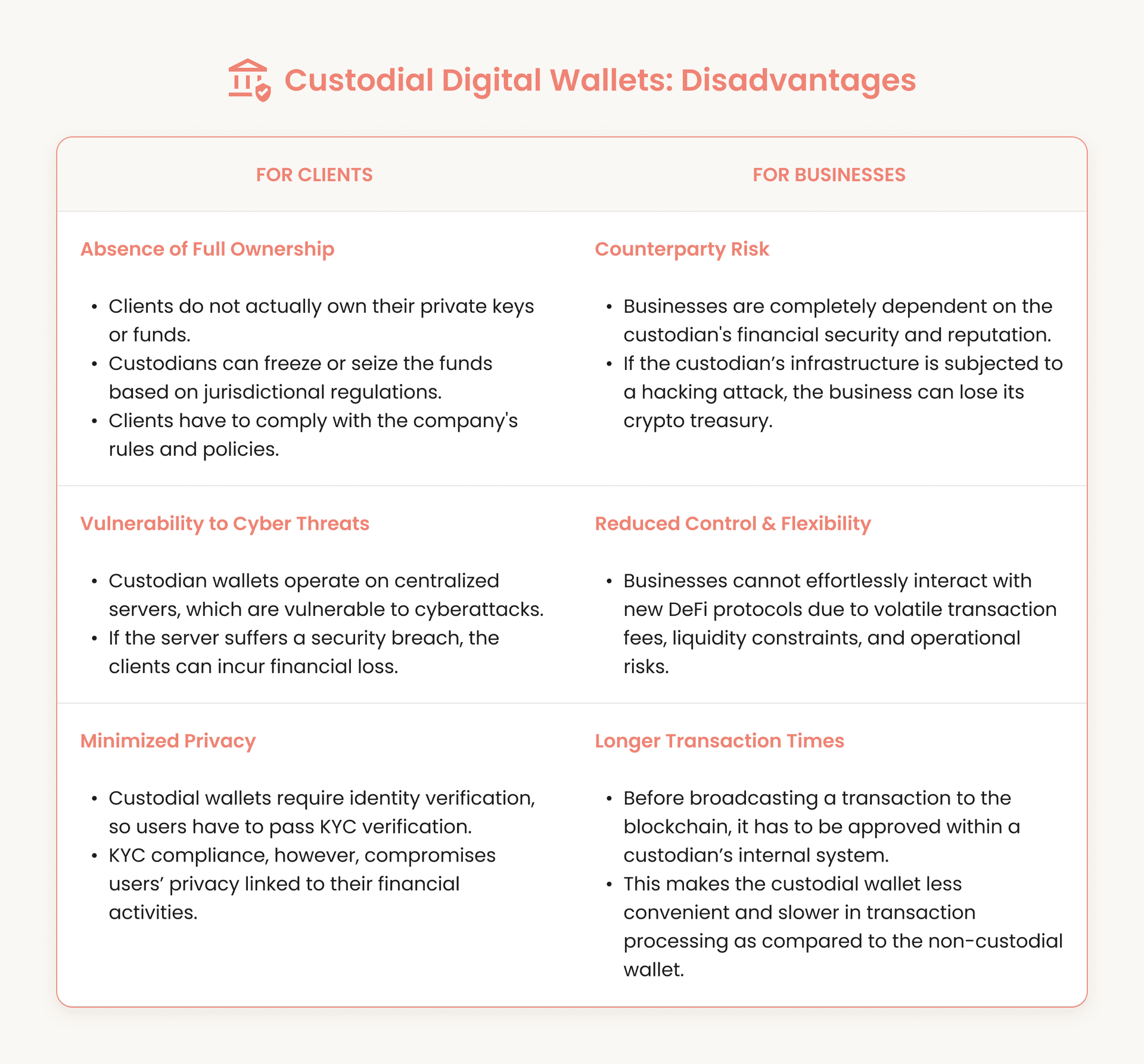

Custodial Digital Wallet

Custodial wallets are digital wallets in which the third-party custodian preserves the client’s private keys and funds. Private keys are essential for data encryption to ensure further transaction processing. The custodian secures and manages the transaction after the client initiates it. There are the following examples of custodial wallets:

-

Coinbase: Coinbase operates a custodial wallet system by default for all user accounts. When a client or business purchases crypto on Coinbase, the platform securely holds those assets in custody. Coinbase manages and stores clients’ private keys.

-

Kraken: primarily an exchange, it also operates a custodial wallet system, where it stores private keys and preserves businesses’ or clients’ assets.

Custodial Wallet: How Does It Work?

-

Account Creation

The user has to sign up on the provider’s platform (website or application) by entering information such as their name and email address. Additionally, they have to create a secure password. Users don’t have to create their own private keys or seed phrases during the account creation process as these are managed by the custodian.

-

KYC Verification

The client has to provide their government-issued document (e.g., passport, driver’s license), and in some cases, complete a liveness check to validate their identity.

Additionally, users may be required to submit documents proving their residence. Users may be required to submit proof of residence, such as utility bills or bank statements.

Different platforms operate via different KYC thresholds, meaning that clients are limited to predefined transaction thresholds until full verification is completed. Limits will be removed once verified.

-

Account Operations & Transactions

Centralized Control: Users’ account balances are entries in the custodian’s internal database. When the client deposits or purchases crypto, it’s not sent to the personal wallet but stored via the centralized ‘hot’ or ‘cold’ wallets.

Simplified Transactions: Users launch a transfer by providing the request/recipient address, the amount to be sent, and confirming through a simple interface. The custodian then uses their private keys to digitally sign and broadcast the transaction to the blockchain on behalf of the user.

Internal Transfers: If transactions occur within the same platform, they may not necessarily go on-chain. Custodians simply adjust the internal ledger to reflect the change in balances, so the transactions can be completed almost instantaneously, and the cost to facilitate them is much lower.

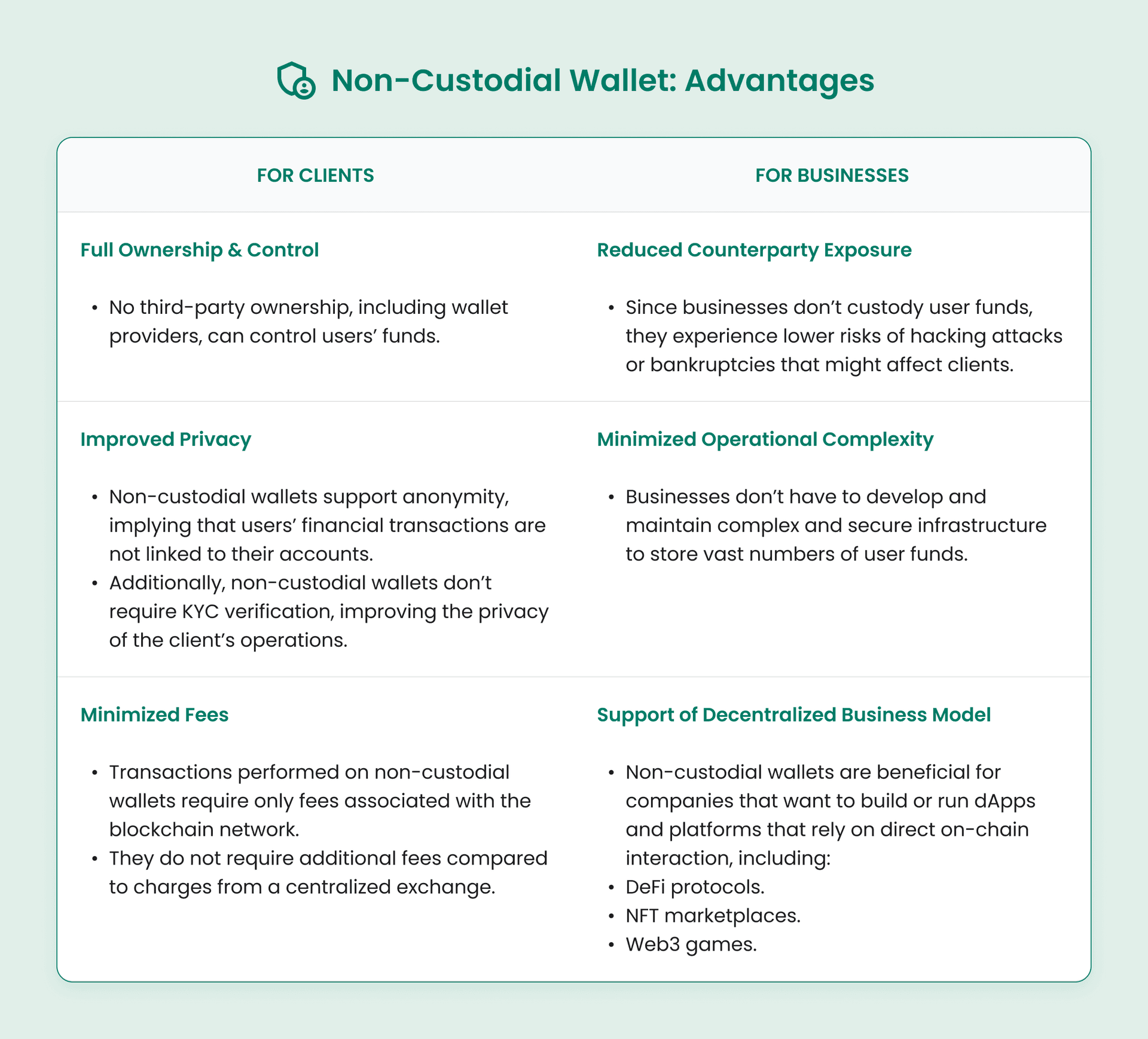

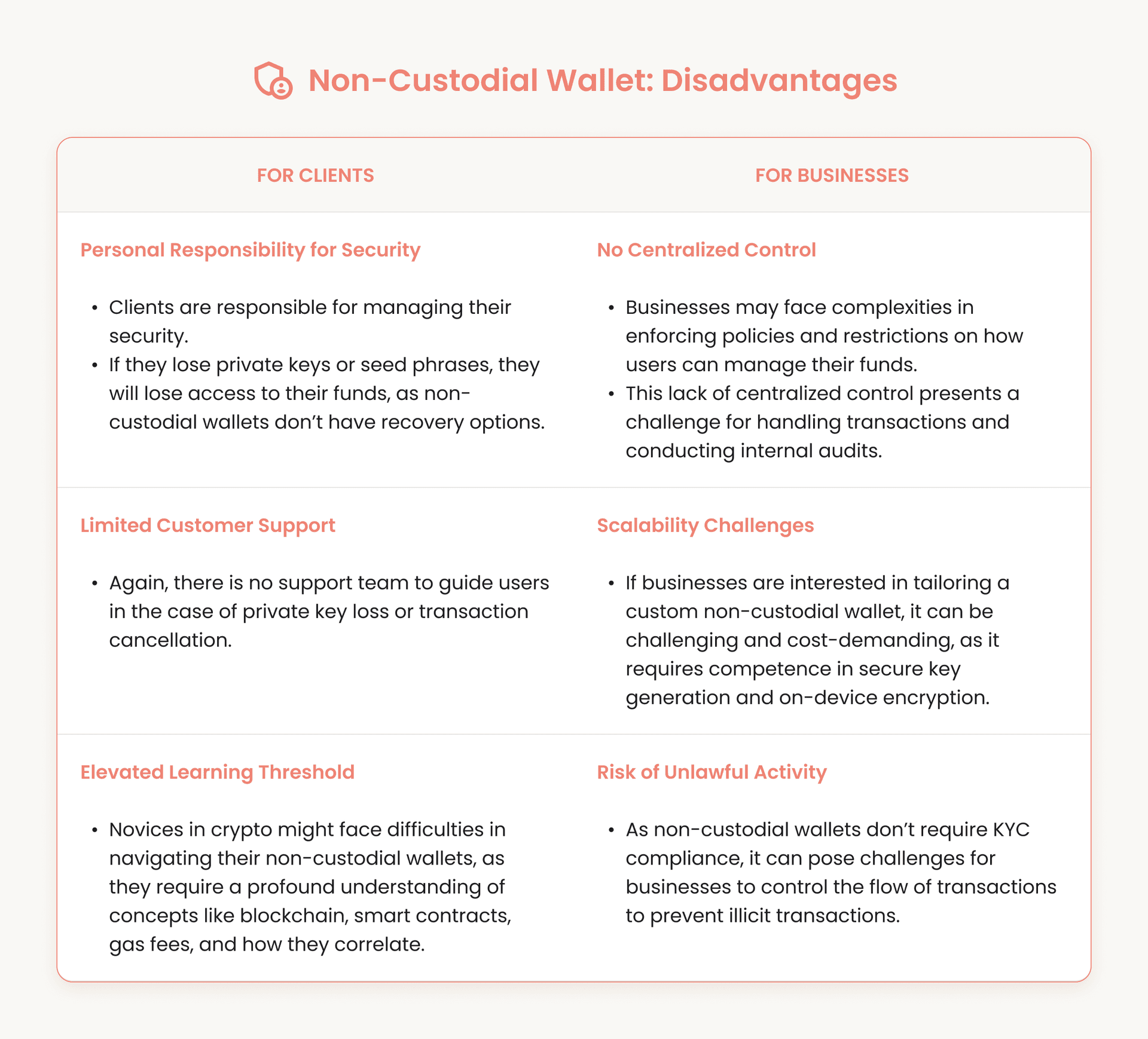

Non-Custodial Digital Wallet

Non-custodial wallets are the opposite of custodial wallets, as clients don’t rely on a third party. Clients have full ownership of their digital assets. There are the following examples of non-custodial wallets:

-

Trust Wallet: a non-custodial mobile crypto wallet that enables clients to store, send, and receive digital assets, as well as keep their private keys.

Trust supports multiple cryptocurrencies across various blockchain networks.

It offers an in-built dApp browser and NFT support.

-

Atomic Wallet: a non-custodial multi-currency wallet that offers clients various ways to hold, exchange, and stake their digital assets - over 500 of them, to be precise. Users hold their private keys and seed phrases, thereby enjoying true ownership of their holdings. The wallet facilitates built-in atomic swaps and integrates with 3rd-party exchanges for trading with the best pricing and pairing options.

Non-Custodial Wallet: How Does It Work?

-

Account Creation

Non-custodial wallets depend upon cryptography rather than personal identification to establish an account. When a user downloads a wallet app, the software will generate a secure cryptographic key pair, including a public key (wallet address) and a private key.

The seed phrase is a sequence of 12-24 words and serves as a master key to the wallet, requiring solid protection. Accounts are tied to cryptographic keys, not to real-world identities, and operate solely on the blockchain.

-

Account Operation

Once created, a non-custodial wallet provides users with direct and independent control over their funds. Private keys are stored locally on the user’s device (encrypted) or on an offline hardware device. The user has to be fully responsible for their security.

When sending and receiving funds, the wallet’s interface communicates with the blockchain, and the user’s private key signs the transaction to prove ownership, without being exposed to the public.

B2C vs. B2B vs. P2P Wallets

There are other types of fiat wallets, including B2C, B2B, and P2P. B2C promotes customer loyalty and retail payments. B2B optimizes corporate transactions and cross-border settlements. P2P facilitates rapid, cost-friendly transfers between individual users.

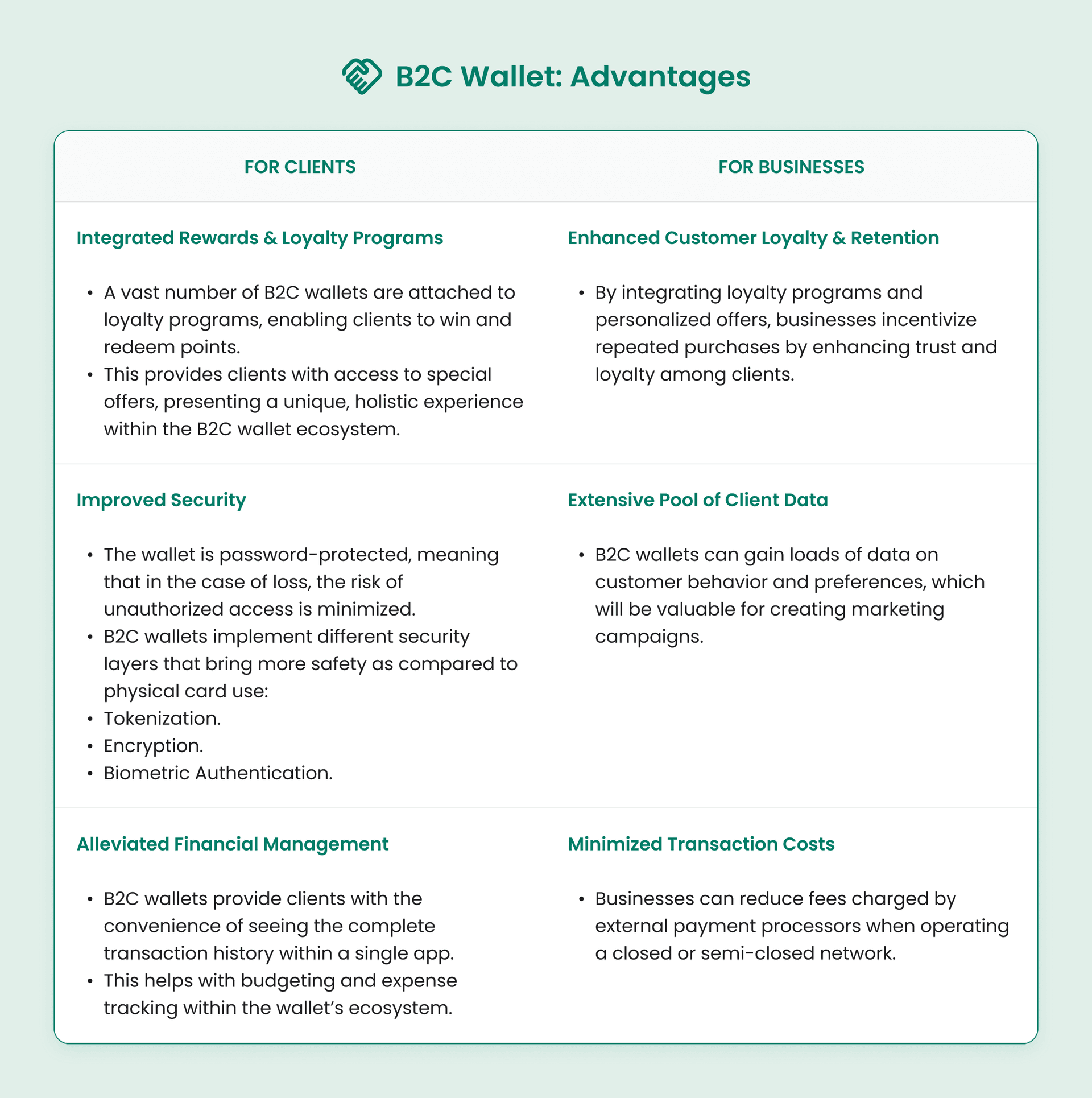

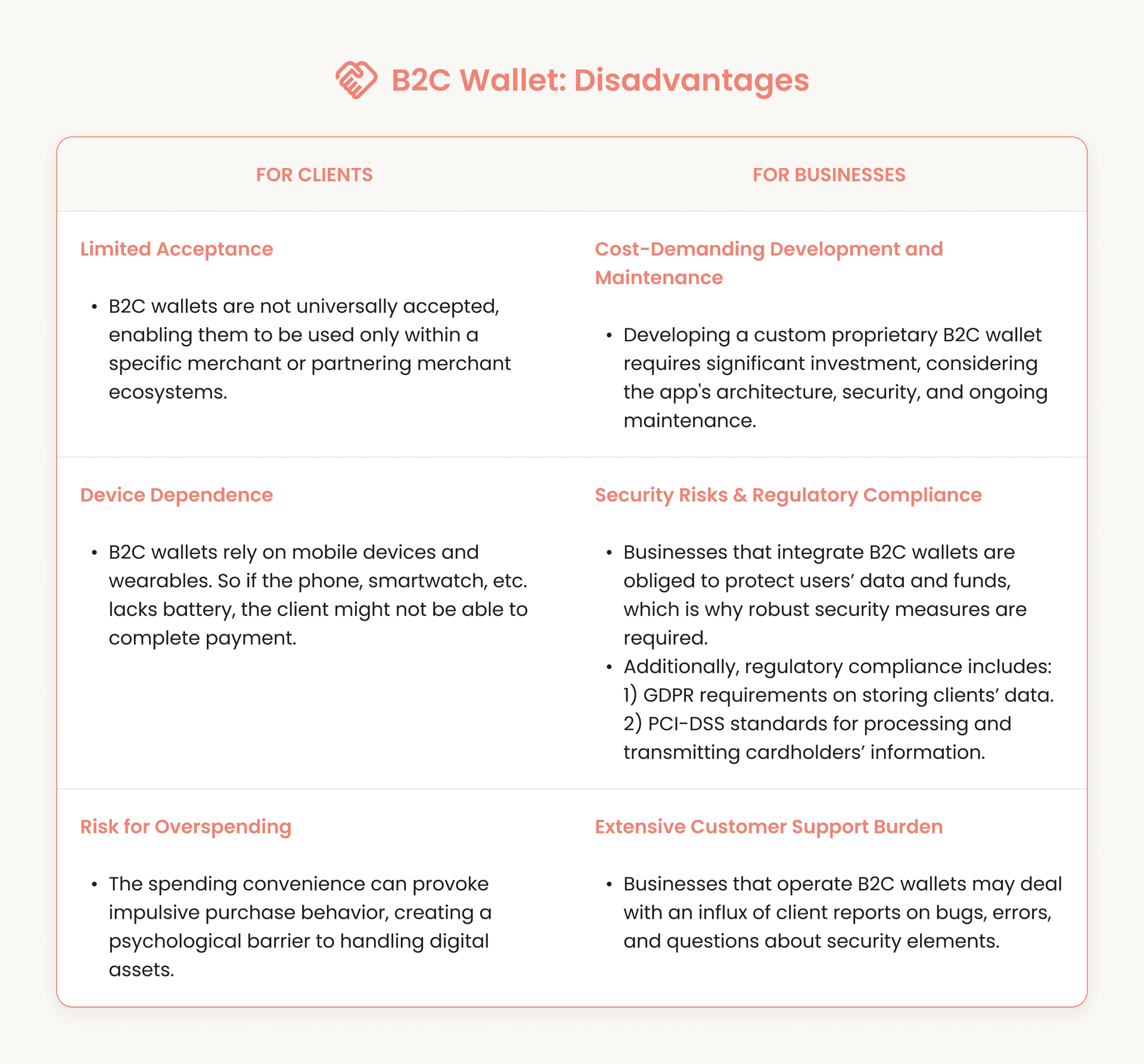

Business-to-Client Wallets

Business-to-Client (B2C) wallets represent a form of digital wallets that businesses can adopt to support clients in making payments for goods and services. B2C wallets can be closed-loop and semi-closed. They are intended to facilitate payment processing and ease for end-users while providing benefits for businesses. There are the following examples of B2C wallets:

-

Alipay: run by Ant Group (Alibaba’s fintech arm), Alipay is a semi-closed digital wallet operated within the network of partners. Users can make in-store QR code payments, online payments, take microloans, book taxis, etc.

-

Uber Cash: a closed-loop B2C digital wallet that is applied within Uber’s network and can be used to pay for Uber Eats and Uber rides. The clients can top up the balance, pay for services, get rewards, and spend them only via the Uber ecosystem.

B2C Wallet: How Does It Work?

-

Account Setup & Funding

Customer will download the app provided by a business or fintech company, usually from an app store. They will create an account, normally connected to a mobile phone or email account. Users can fund the wallet from the debit/credit cards, and some wallets allow you to preload value for a future transaction.

-

Payment Process

The app connects and communicates with the merchant's payment terminal via NFC for an in-store payment or secure APIs for an online payment flow. Clients’ sensitive data is protected using tokenization and encryption in transit and at rest, minimizing the interception risk. Transactions require authentication, such as entering a PIN or using biometric authentication. Payments are authorized in real time, promoting fast checkout.

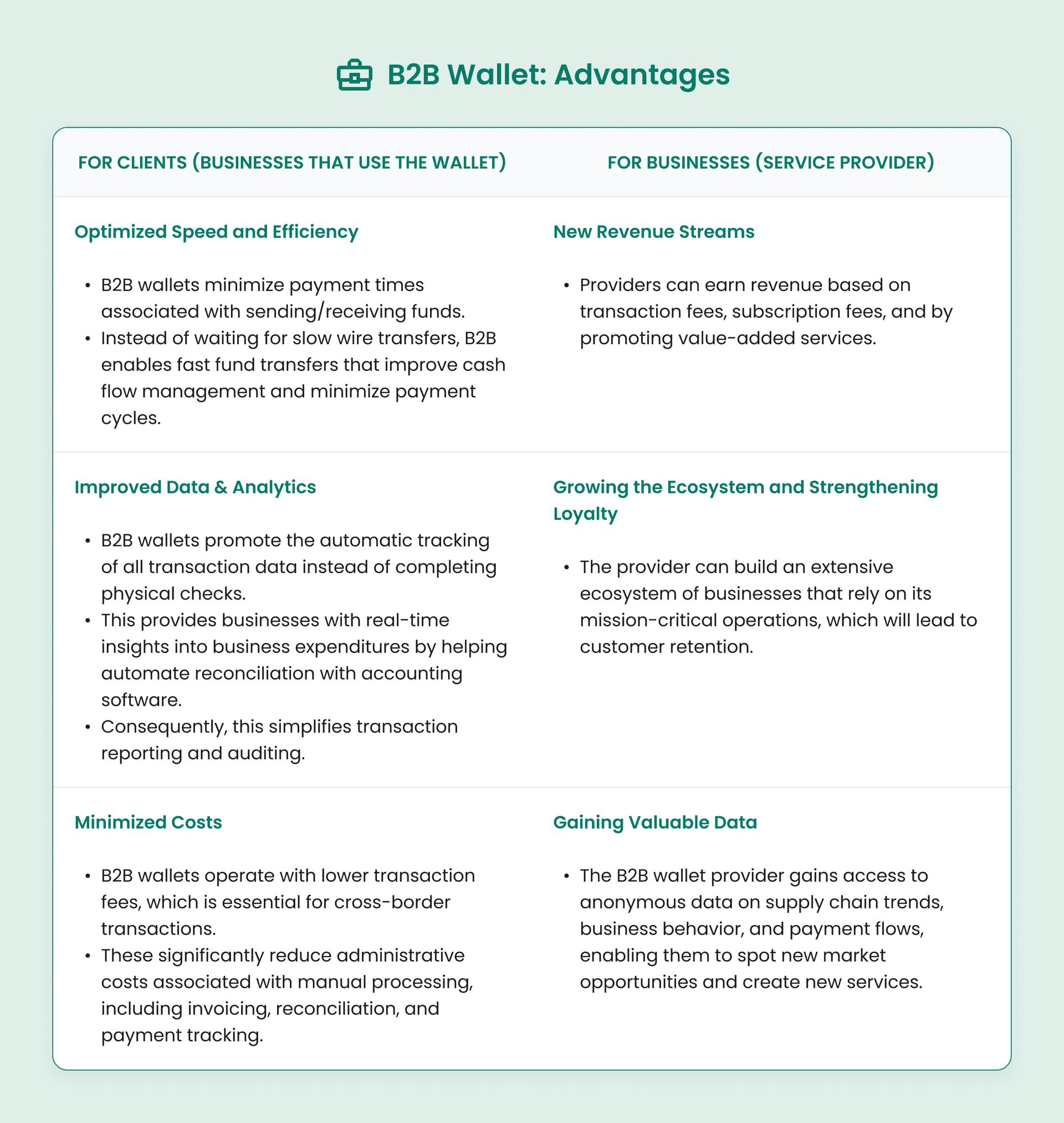

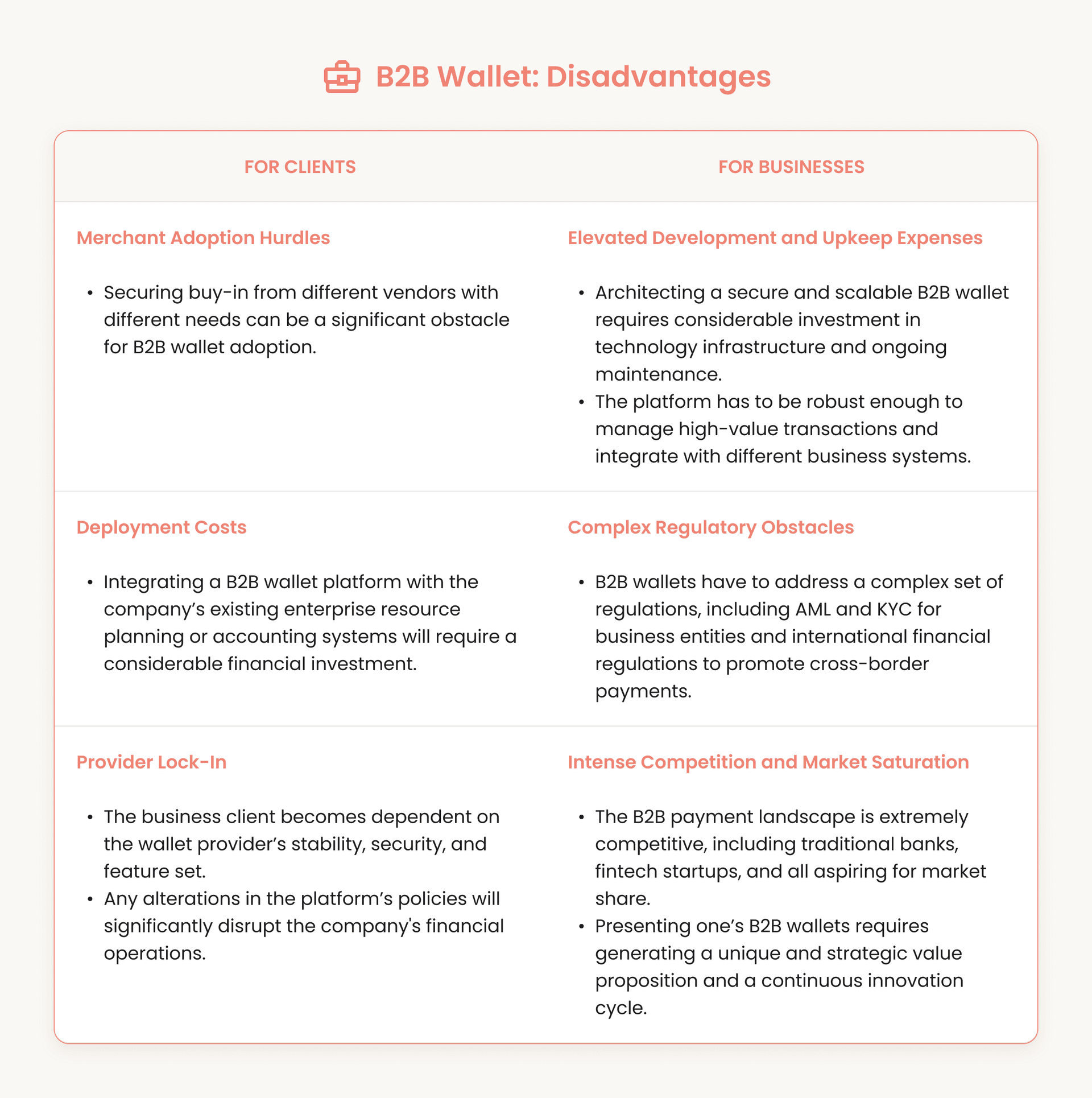

Business-to-Business Wallets

A B2B (Business-to-Business) wallet is a digital payment method built for businesses to pay their suppliers and track expenses. This kind of digital wallet is designed to simplify the complexities of B2B payments; in other words, it generally replaces manual payment solutions like checks or wire transfers. This could include the following B2B wallet providers:

-

Payoneer: a B2B wallet designed specifically for online sellers, freelancers, and businesses who want to receive and send cross-border payments. Payoneer allows businesses to receive payments in multicurrency accounts (e.g., EUR, USD, GBP) directly to the platform, connect global platforms (e.g., Fiverr, Amazon), support mass payouts, and more.

-

Veem: another B2B wallet that allows small and medium businesses to send and receive cross-border payments. Businesses can maintain a balance in multiple currencies or connect their bank account withdrawal or funding. While using Veem, businesses can utilize account features including payment tracking & invoicing, local settlement, and around a 100+ currencies.

B2B Wallet: How Does It Work?

-

Creating an Account

Businesses register for B-to-B wallet solutions, which must include KYC & AML which requires submission of the company's registration documents and corporate tax IDs to prove the company identity and legal status. B-to-B wallets also allow for multiple users under role-based permissions, such as one employee to initiate payment and another employee to approve.

Also part of the setup is making sure the wallet can integrate with the business's existing system, such as accounting software or ERP (Enterprise Resource Planning) systems or accounting systems. This allows for data to be shared automatically, and the correct people can then access invoices and payments without the unnecessary delays.

-

Payment Processes

The wallet can automatically read the invoice data from the business's accounting system, the payments will pass through the company's internal approval process for examples, it may be required for multiple managers to authorize before moving forward.

Once the approval is complete, the wallet will initiate the payment through options such as ACH, virtual credit cards, or even wallet-to-wallet transfer within the same system. The wallet will automatically document the transaction and keep a full digital trail, which can also be matched with invoices in the accounting system; that matched entry would eliminate manual data entry and the risk of human error for both businesses that send and receive payment.

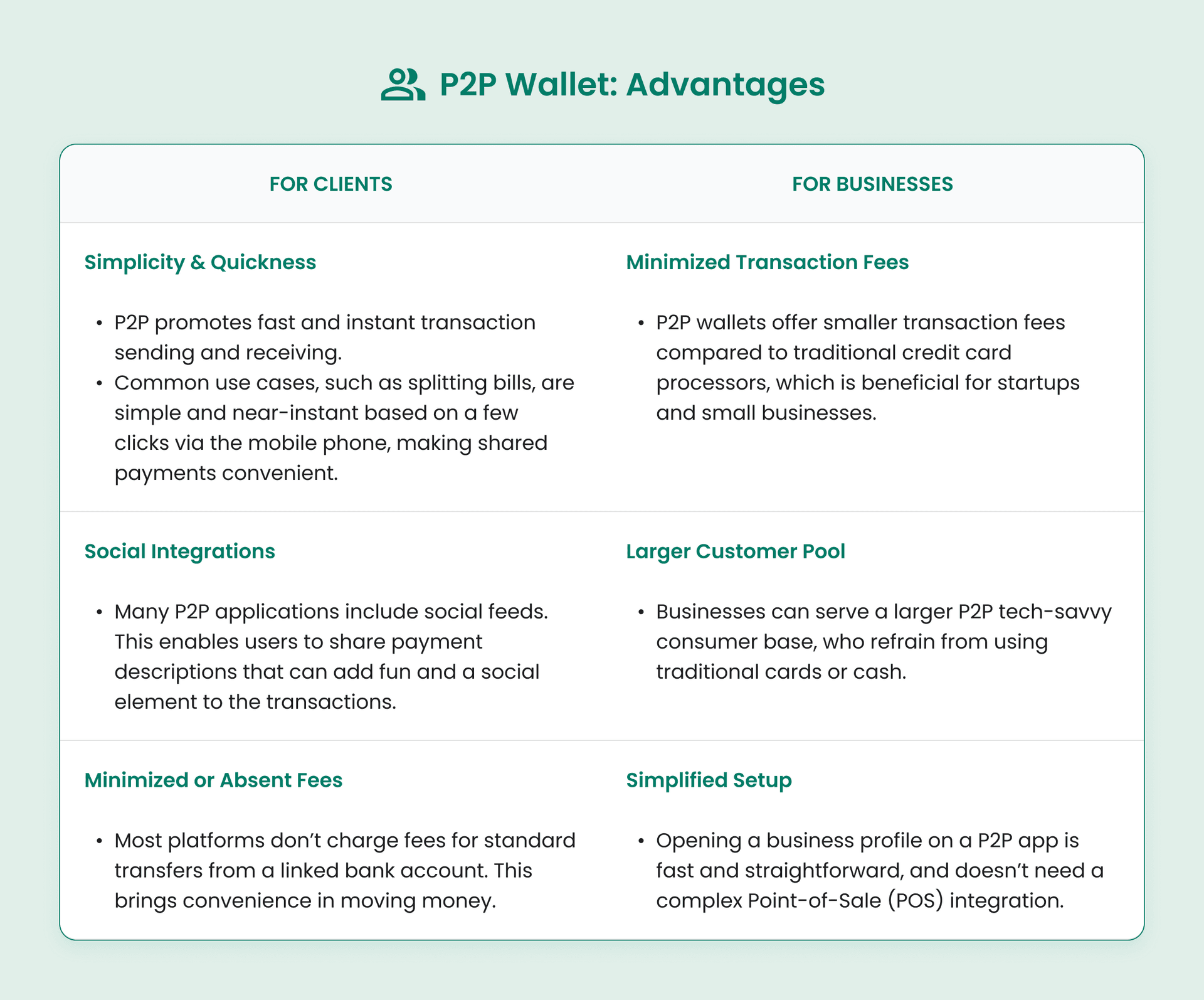

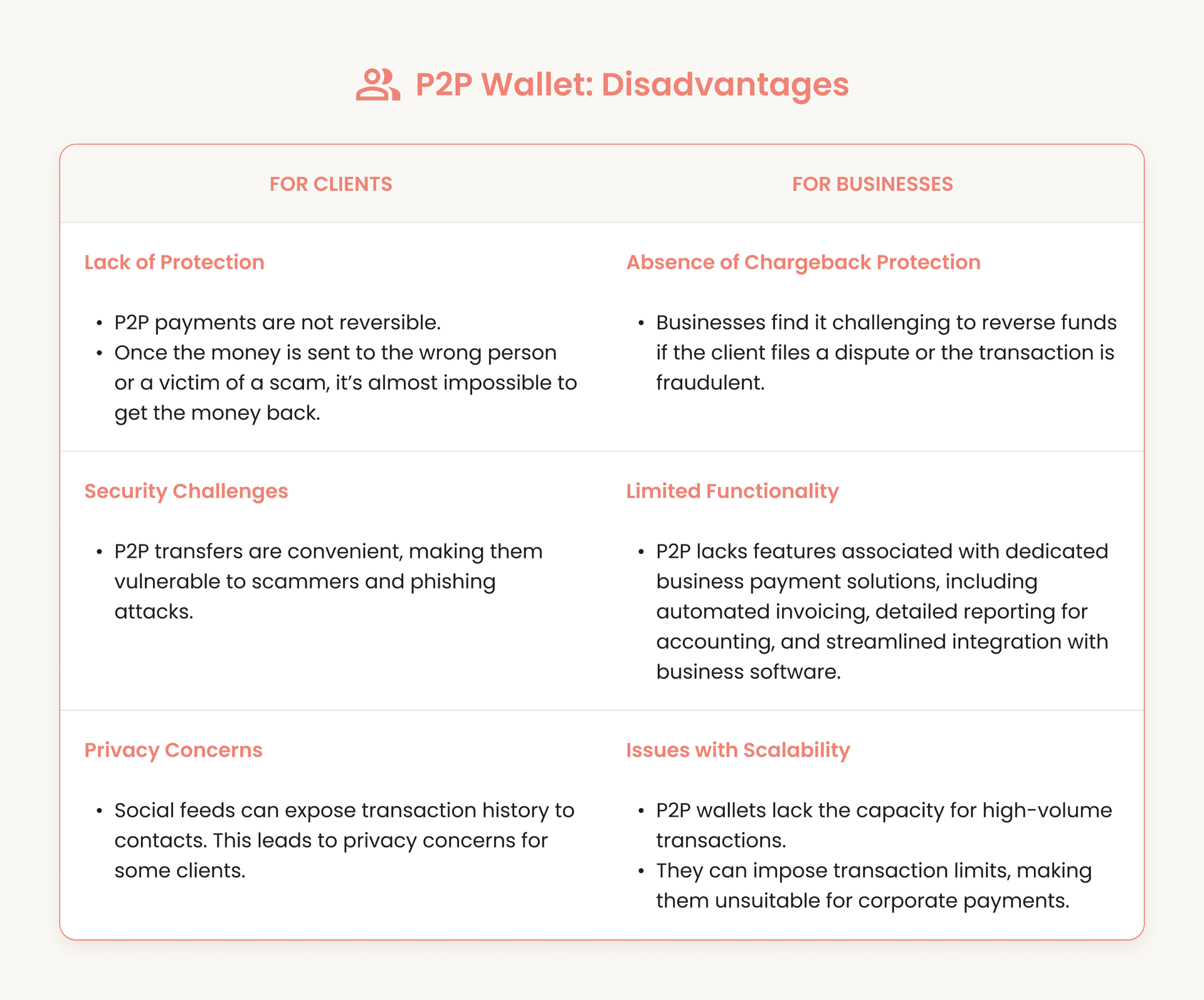

Peer-to-Peer Wallets

Peer-to-Peer (P2P) wallets are digital payment solutions that prioritize personal use to encourage transactions directly between people. While they are intended for personal use, businesses are utilizing P2P wallets to make payments more efficient, and there are advantages and disadvantages for the business. Examples of P2P wallets include:

-

Zelle: a P2P wallet integrated into the user’s existing bank app. Clients can send money directly from their bank account to another person’s bank account using an email or phone number.

-

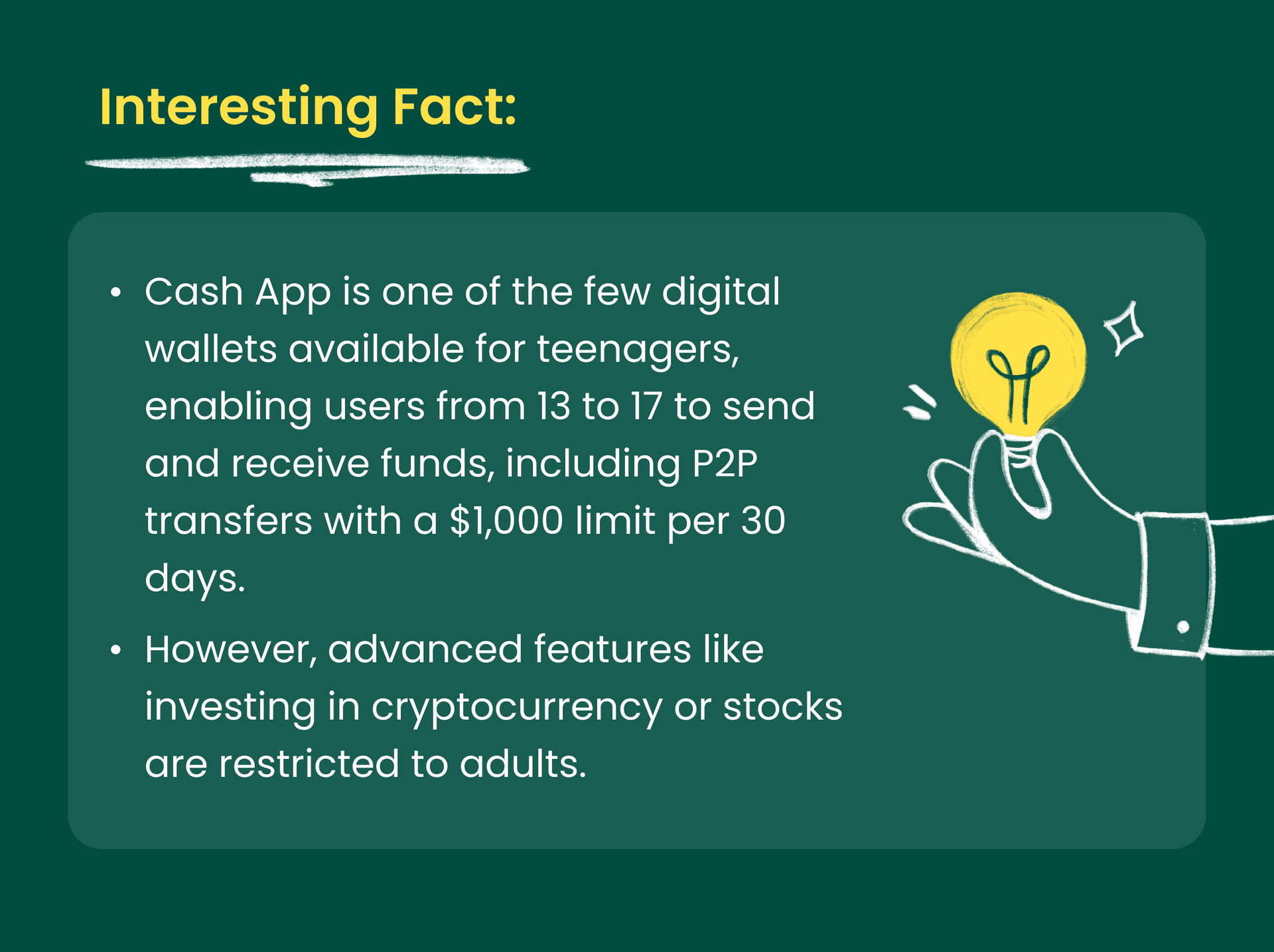

Cash App: a P2P wallet that allows the client to send and receive money simply using a phone number, email, and the unique ID $Cashtag. The user can keep a balance in the app to spend, withdraw, transfer money, and even split bills. Cash App also has a direct deposit feature.

P2P Wallet: How Does It Work?

-

Account Setup

The client downloads the wallet from the business or a third-party provider. Next, the user adds a payment method, which could be a credit or debit card or a bank account. Users can add funds to their balance, which can be used for future payments. The wallet provider will encrypt and store the financial information. Clients will be required to set a PIN and create a facial or fingerprint scan as a secure authentication check.

-

Payment Process

Based on the technology that is attacking time both in-app and online, the client initiates a transaction by tapping the payment system on a mobile device (NFC) for in-store purchases or accepts payments through secure online checkout. The wallet uses tokenization to replace real debit/credit card information with a token instead. For in-person payments, the token is sent via NFC to the merchant's device over an encrypted channel. For the online transaction, it is sent through APIs.

The user accepts the transaction using security features such as Face ID, confirming authorization to the wallet. The payment processor is now deliver the token submit back to the client's bank. Once approved, the business receives a confirmation of payment, and the customer is provided with a digital receipt.

Hot vs. Cold Wallets

Hot wallets relate mainly to cryptocurrencies; however, they can replicate the work of fiat-relevant applications. Cold wallets focus on cryptocurrencies only.

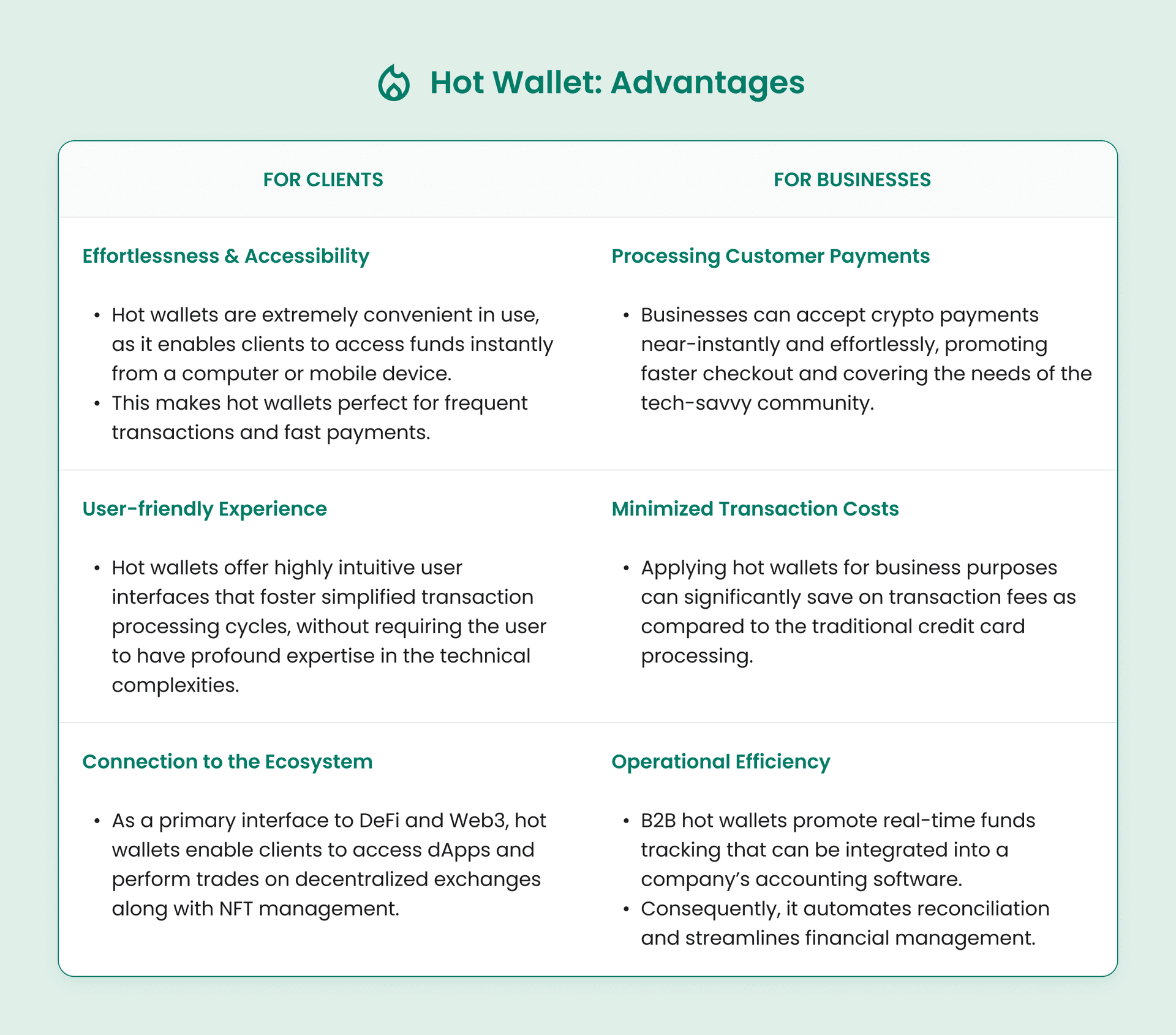

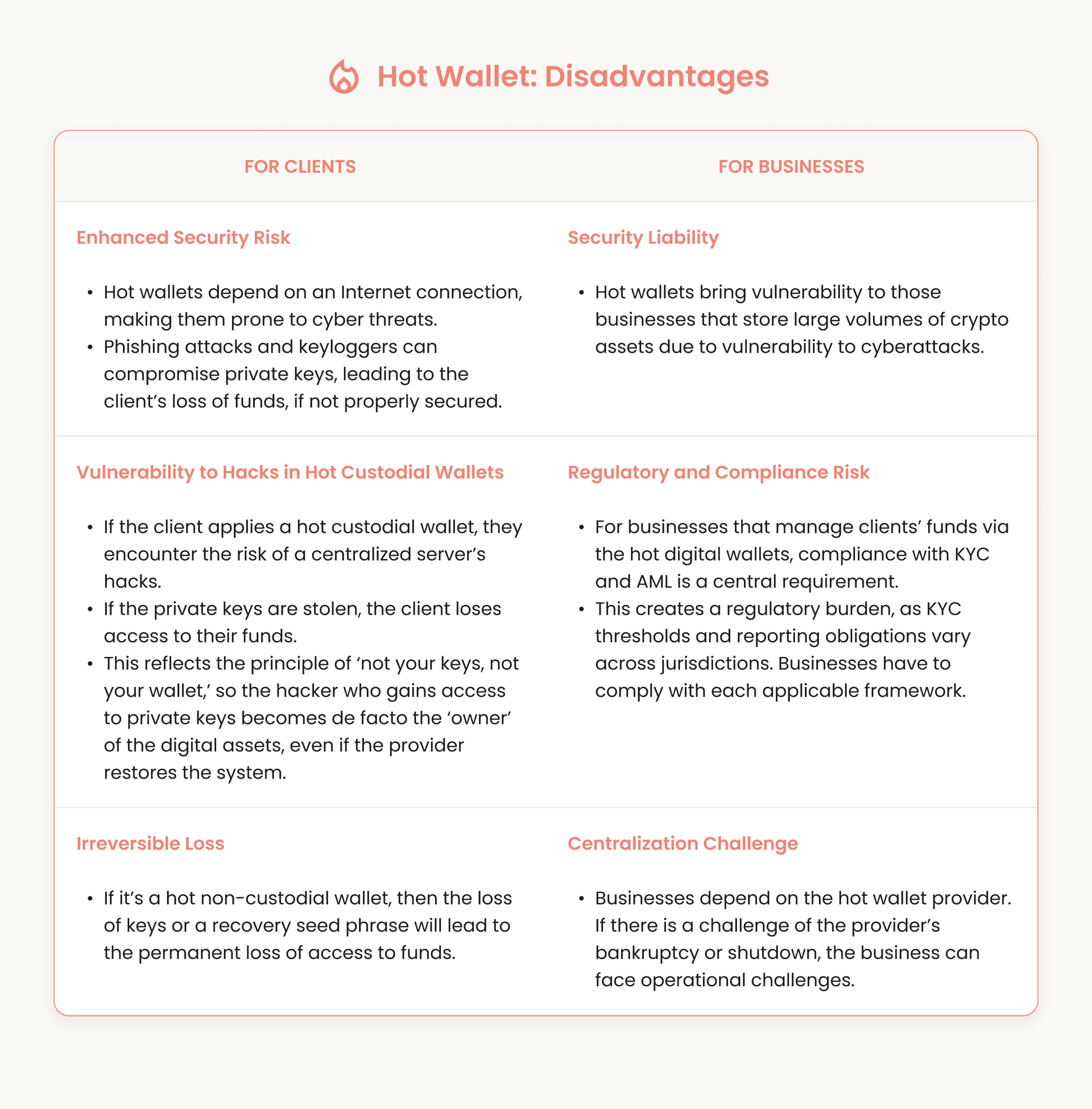

Hot Wallets

A hot wallet is any cryptocurrency wallet that is connected to the Internet, which includes both wallets on exchanges and desktop, web, and mobile wallets. Their online presence provides high convenience in operability but imposes a range of security risks.

-

Exodus: a software wallet available for desktop and mobile. It stores private keys locally on the client’s device, not a centralized server. The wallet is non-custodial, as users hold their private keys and funds. The wallet operates via 300+ cryptocurrencies and tokens and enables real-time portfolio charts and balance tracking.

-

Electrum: a Bitcoin-only desktop wallet, known for its advanced features and robust security measures. A non-custodial wallet that supports multi-signature authorization and integrates with the hardware wallets (Ledger & Trezor), promoting cold storage when paired.

Hot Wallet: How Does It Work?

-

Account Creation

When downloading and setting up the hot wallet, the software generates a unique pair of cryptographic keys: public & private. To simplify backup, the wallet also creates a seed phrase. The phrase can be used to restore the user's entire wallet on a compatible device.

-

Transaction Processing

The client applies the digital wallet’s user-friendly interface to initiate the transaction process by providing the public address of the recipient and the amount of crypto they wish to transact. The wallet then applies private keys to digitally ‘sign’ the transaction. This signature is based in cryptographic proof that the client “owns” the funds and has authorized the payment.

The signed transaction is broadcast to the blockchain’s network, where nodes relay it to the miners or validators, depending on the consensus mechanism. The network verifies the transaction’s validity by checking the digital signature and ensuring the sender has sufficient funds. Once validated, the transaction is added to the new block. After confirmation, the funds are transferred.

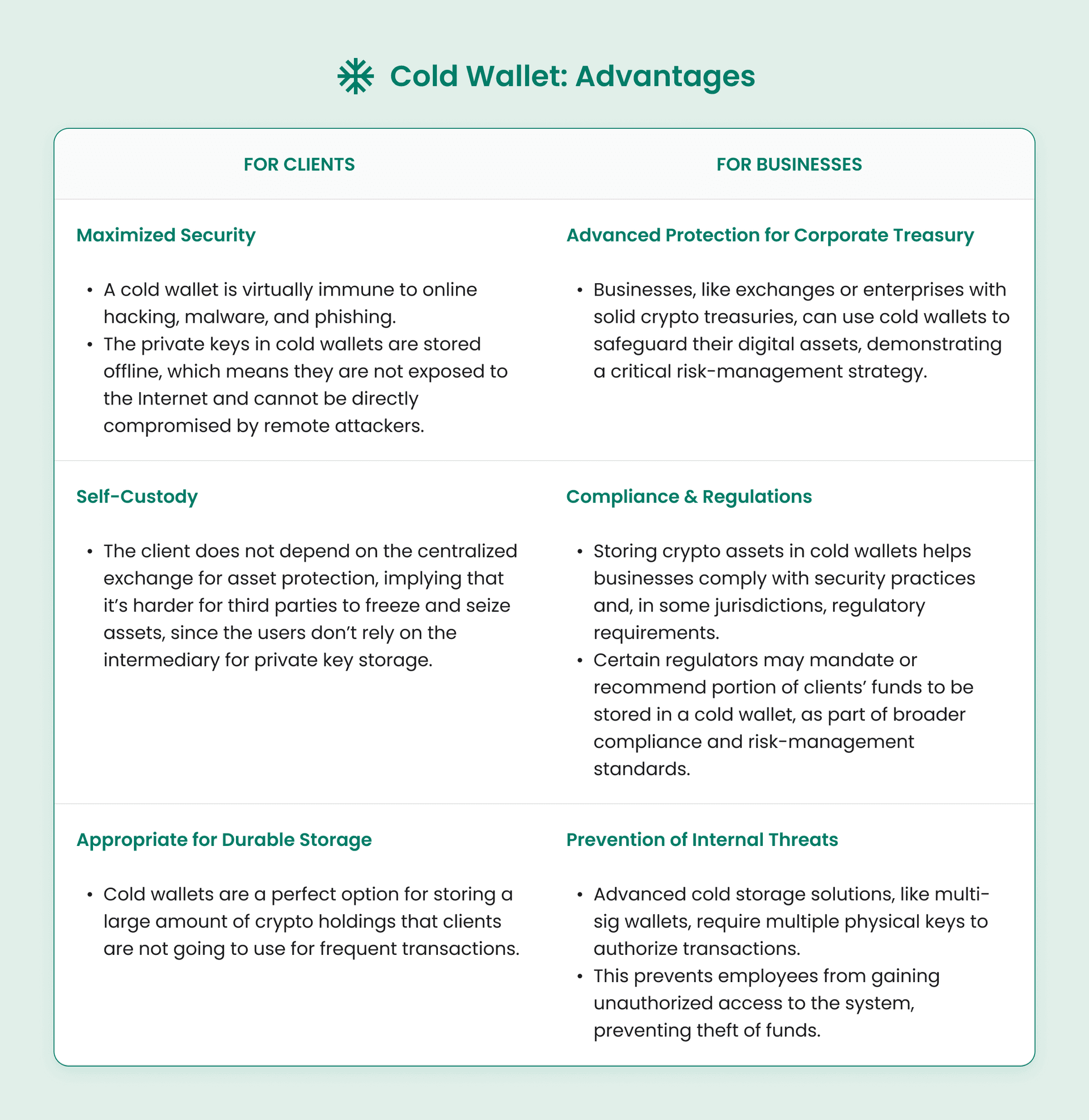

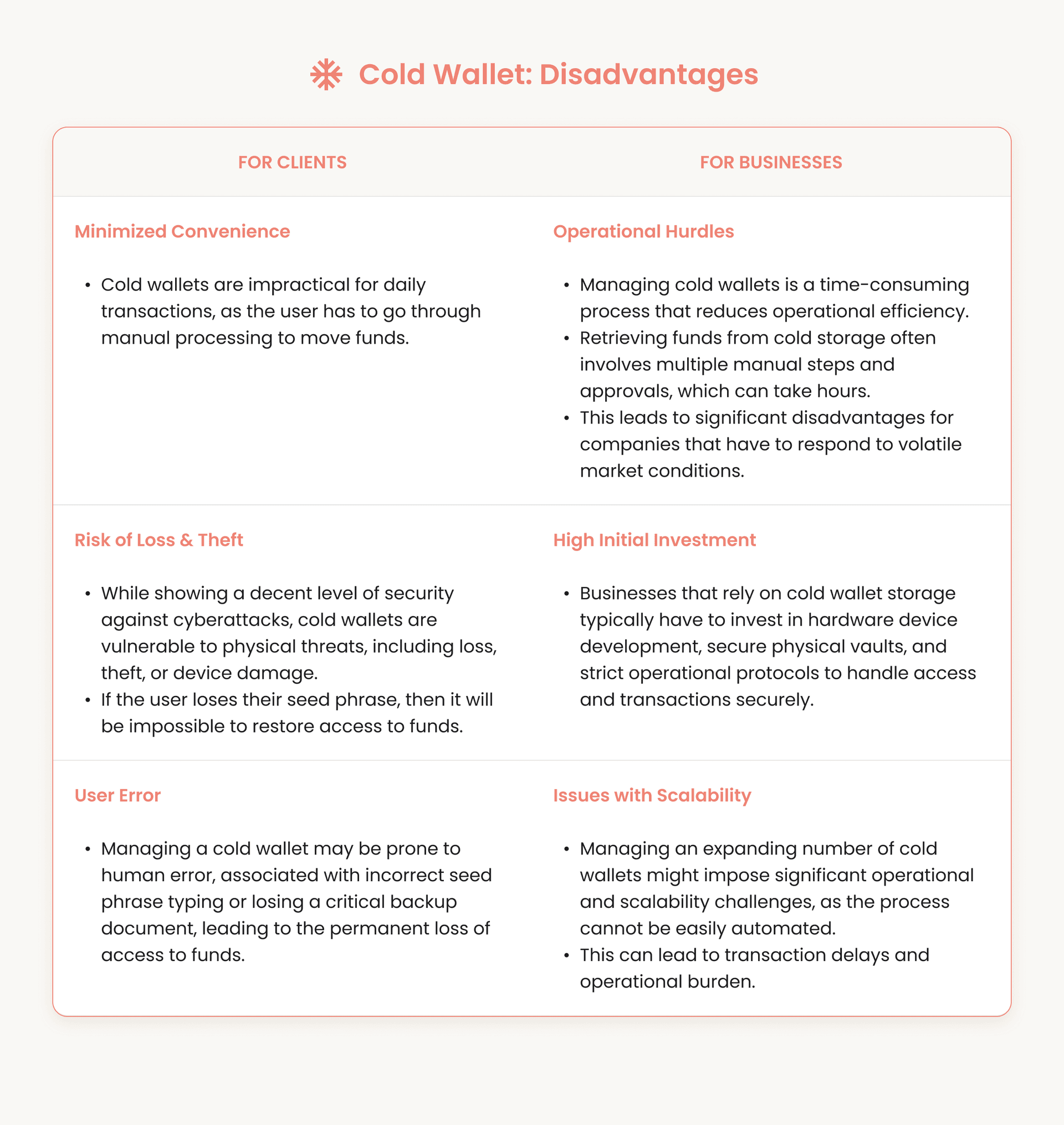

Cold Wallets

A cold wallet is a cryptocurrency wallet that is not linked to the Internet. This physical separation from online networks makes a cold wallet the most secure alternative for storing cryptocurrencies. However, decent security compromises convenience. Examples include:

-

Ledger: the Ledger Nano S Plus and Ledger Nano X are examples of hardware-based cold wallets. The devices resemble USB drives and the private keys are securely stored on a certified Secure Element chip. Transactions are signed by pressing a button on the device. Ledger supports around 5000+ cryptocurrencies and tokens, and through Ledger Live and integrated apps, also enables staking and NFT management.

-

Trezor: just like Ledger, Trezor is a physical device that stores private keys securely within the device, ensuring they never leave it. Trezor Suite is the companion desktop and browser application that allows users to manage assets, send, and receive crypto, and track their portfolio.

Cold Wallet: How Does It Work?

-

Account Setup & Key Generation

When the client sets up the hardware wallet, it generates a unique public key (the wallet’s address) and private key entirely offline on the device. Then, the device creates a seed phrase to recover funds in the case of device loss or damage.

-

Transaction Process

The client uses the companion software on their Internet-connected computer to create a transaction. The unsigned transaction includes details such as the recipient's address and the amount that is not yet authorized. The unsigned transaction information will be securely sent to the hardware wallet via a USB cable, microSD card, etc.

The user then sees the transaction details on the wallet’s screen and must physically confirm the transaction by pressing the button. The cold wallet applies the private key to sign the transaction, but it does not leave the security chip.

The signed transaction is sent back to the online computer and then broadcast to the blockchain peer-to-peer network. The transaction is verified by nodes and, once confirmed, added to the blockchain. The private key remains securely stored throughout the complete transaction cycle.

Must-Have Features vs Nice-to-Have Features

When it comes to digital wallet functionality, regardless of whether it’s crypto or fiat-based, the application must include a set of essential features to support the functions digital wallets are used for.

Must-Have Features for Crypto Wallets

These features are the core of any secure crypto wallet, as without them, it will be an inapplicable tool for managing digital assets. Here’s the list of must-have features for crypto wallets.

Secure Key Management

This is the core security requirement of any crypto wallet, as it must securely generate and store private keys. If it’s a non-custodial wallet, the keys are stored on the user’s device in encrypted form, while the custodial variant manages them on behalf of users.

Crypto Sending/Reception Functionality

A crypto wallet must support sending crypto to another user’s public address and receiving funds through its own public address.

Backup & Recovery

A secure wallet provides users with a way to back up their private keys. The industry standard is a seed phrase, which allows them to recover their wallet and regain access to funds on a new or compatible device if the original is lost or damaged.

Transaction History

A clear, detailed record of all incoming and outgoing transactions. This enables users to track their spending, portfolio growth, and verify that transactions are successful.

A crypto wallet must provide a clear, detailed record of all incoming and outgoing transactions. This helps clients track their spending, verify transactions, and monitor their asset growth over time if the wallet embeds portfolio features.

Basic Security Measures

The wallet must have foundational security features to protect the wallet against unauthorized access. These measures include PIN, password, along with support for biometric authentication.

Multi-Chain Support

A crypto wallet application should be able to manage assets across different blockchain networks, including Bitcoin, Ethereum, and others, which distinguishes it from single-chain wallets.

Check out the seven best crypto wallets.

Check out the seven best crypto wallets.

Nice-to-Have Features for Crypto Wallets

Nice-to-have features are to elevate a basic wallet into a comprehensive platform, presenting new opportunities for modern crypto users.

Embedded Swaps

This is about the ability to trade crypto for crypto directly within the wallet, without referring to a third-party exchange.

DApp Browser

This means that the wallet has an integrated browser for clients to engage with and interact with decentralized applications and smart contracts directly from their wallets. This is important for easy involvement in the ecosystem of Web3 and DeFi.

Integrated Fiat Gateway

This feature enables customers to buy crypto using fiat directly with debit/credit cards or bank transfers, aiding in lowering certain aspects of the entry hurdles for new users.

Must-Have Features for Fiat Wallets

These are the principal functions a fiat wallet has to provide to ensure a secure and reliable fulfillment of its primary purpose of handling finances.

Secure Authentication

A fiat wallet has to employ different layers of security to prevent unauthorized access and illicit fund activities. This includes robust password protections, PIN, and the support of biometric authentication (including facial recognition and fingerprint).

Sending/Reception of Fiat Money

A wallet should provide a simple and intuitive way for users and businesses to send and receive funds for personal and commercial purposes. Most wallets rely on public addresses or QR codes. Some support transfers via phone numbers, email addresses, or usernames for effortless usability.

Source: FinTech Magazine.

Bank and Card Integration

Adding and withdrawing funds are critical functions for the fiat digital wallets. Bank & card integration must allow users to securely link their bank accounts and payment cards to transfer money in and out of the wallet.

Transaction History

This is an essential element of a fiat digital wallet, as users need full visibility into their financial activity. A clear and detailed record of all deposits, transfers, and spending effortlessly.

Compliance & Regulations

Each fiat digital wallet must have built-in systems to comply with strict financial laws. These include compliance with the KYC thresholds to verify user and business identities and AML measures to monitor and report suspicious activities.

Nice-to-Have Features for Fiat Wallets

These features add extra value to the user experience, driving engagement and helping the wallet stand out in the market. Here are the following nice-to-have features for fiat-based digital wallets:

Peer-to-Peer Functionality

This relates to the ability to send and receive funds with added social components such as emojis and comments. Applications like Cash App have integrated such features to modernize digital wallets and improve transaction engagement.

Integrated Bill Pay

This feature is becoming increasingly popular, as wallets integrate the capability to pay bills and manage subscriptions directly from the app. Users can configure recurring payments, receive reminders of due dates to prevent late fees, and track payment history all within one interface.

Physical or Virtual Debit Card

If the wallet provider issues virtual and digital cards, this creates a strategic advantage in payment processing by bridging the gap between online and traditional commerce. Linking a wallet to the card enables consumers to make payments in stores that accept only cards (alongside cash), thereby promoting financial inclusivity.

Budgeting & Analytics Tools

These functions can allow users to manage their finances by automatically sorting transactions into categories such as utilities, entertainment, transport, etc. The wallet also can create visual summaries, spending charts, or monthly reports that highlight trends in their financial activity. This means users can track their expenses, establish budgets, and make informed decisions, effectively making the wallet a helper for payment.

Digital Wallets for Business and Startups

With the continuous growth of fintech, digital wallets provide businesses and startups with the opportunity to craft new services, build customer loyalty, and generate revenue. When entering this market, there are two strategic decisions: choosing a white-label solution and defining a monetization model.

White-Label Solutions

White-label solutions are pre-built and ready-to-use digital wallet platforms that businesses can license and rebrand with their own logos, colors, and user experience. This plug-and-play option allows companies to offer their digital wallet services to their customers without the time, cost, and complexity of building from scratch.

Companies inherit key functions, such as account management, fund transfers, spending history/reports, KYC/AML compliance, and access to payment networks when using white-label wallets. Many of these providers have additional modules and services such as bill payments, loyalty programs, card issuance, and cryptocurrency support.

For startups and large enterprises, white-label options offer the benefit of reduced technical and legal risk, shorter time-to-market timeframes, and increased scalability as their clients' needs grow. The white-label option provides companies with the ability to focus on customer acquisition and brand positioning based on a trusted technology platform.

Monetization Options

Businesses and startups must plan for revenue streams once the wallet is launched on the market. A digital wallet, whether crypto or fiat, can be an excellent tool for monetizing through various models:

Transaction Fees

Transaction fees are the simplest and easiest ways for monetizing a wallet service. This can a simple percentage fee on a crypto transaction or fixed costs on fiat services like peer-to-peer transfers, merchant payment, and bill payment, all of which are a great way to generate revenue.

Subscription Fees

Businesses can provide a free basic wallet alongside a premium, subscription-based tier that provides advanced features. The premium package can include benefits like higher transaction limits within KYC/AML thresholds, detailed analytics, or cashback rewards.

Interchange Fees

Wallets that support linked debit and credit cards can earn a share of the interchange fees collected by card networks (such as Visa or Mastercard) on each transaction performed with the card.

Value-Added Services

Revenue can be generated by integrating and promoting additional financial offerings, which include micro-loans, insurance, or investment options.

The Future of Digital Wallets

The advancement of digital wallets is re-inventing how people and companies use and access funding. This disruption of technology consigns the landscape on user experience by improving access through financial services.

The Impact of Web3, CBDC, NFC & Biometric-First UX

The next iterations of digital wallets will converge the unique technology while continuing to prioritize secure app functionality.

Web3

The core focus of digital wallets in the Web3 is about self-sovereignty and interoperability. Web3 wallets are projected to become hubs for a user’s entire digital identity evolving beyond simple currency storage. They enable self-custody of assets, meaning users have direct control over their private keys and do not need to depend on centralized entities, like an exchange.

Digital wallets also serve as gateways to the Web3 ecosystem, allowing users to interact directly with decentralized applications, manage NFTs, and take part in Decentralized Finance (DeFi).

CBDCs (Central Bank Digital Currencies)

Digital wallets are becoming the primary way citizens can hold and transfer a digital version of their national currencies, as central banks explore the potential in CBDCs. Wallets would likely store those digital currencies by offering instant, low-cost, P2P cross-border payments.

CBDCs and digital wallets are about merging the security of traditional government-backed money with the effectiveness of digital payments. Enabling CBDCs is about creating a resilient and transparent payment system, while supporting innovation and competition.

NFC (Near Field Communication) and Biometric-First UX

These technologies are about accelerating payments by intensifying security. NFC promotes ‘tap-to-pay’ functionality, which has become a more and more widely accepted feature among digital wallets.

The biometric-first UX enables users to authorize a payment simply by using their face or fingerprint scan, minimizing the need for passwords or PINs. User experience will be designed around those seamless interactions, with security processes like encryption and tokenization operating in the background.

Global Accessibility and the Digitization of Finance

Digital wallets can significantly contribute to the global financial landscape by directly affecting the gap in financial institutions’ accessibility.

Serving the Unbanked

Many communities in the world remain unbanked. This makes payment processes cumbersome and troublesome, and many citizens do not have bank accounts. Therefore, a digital wallet that is linked to a smartphone can be revolutionary, allowing access to digital finance, and critical financial services such as sending and receiving money. Based on the structure of the wallet, micro-loans can also be included to further increase the overall financial inclusion.

Streamlining Cross-Border Payments

The traditional method of international remittances can be a slow and expensive process. Digital wallets are about lower transaction costs and quicker transfer times. Digital wallets enable near-instant financial transfers to any location in the world, which can be valuable for the global workforce.

Eliminating Barriers to Trade

Digital wallets break through traditional limitations associated with trade to enforce payment or receipt of payment for services anytime and anywhere in the world, even without physical infrastructure.

Summary

There are different types of digital wallet apps, each offering distinct benefits and drawbacks for business entities and end users. Crypto wallets enable simplified and accelerated crypto trade, sending/receiving, which cannot be recovered if the private keys are lost (non-custodial wallet). The simplified recovery in the custodial wallets is compromised by the fund ownership among the custodians.

Fiat-based wallets provide convenience, speed, and perks like cashback or loyalty programs that are often limited by merchant acceptance and reliance on vendor technology. Choosing the right fiat or crypto digital wallet requires understanding these advantages and disadvantages to identify the most suitable option or to design a custom fintech solution.

Looking to build a digital wallet, crypto, or fiat? Get in touch with us today!

Looking to build a digital wallet, crypto, or fiat? Get in touch with us today!