Did you know that digital wallets hit the spot, considering fast transactions and optimized security, to mention Apple Pay, Google Pay, and PayPal? This all-in-one payment option can significantly reduce time with its one-click contactless payments, bypassing the card-relevant PIN code entry.

Suitable for micro-transactions, digital wallets operate with a lower commission than traditional banking ones, motivating businesses to create ones to meet their needs. According to Capital One Shopping research, digital wallets account for 39% of online transactions among US citizens. This comprehensive guide describes an in-depth process of how to make a digital wallet app, underlining the essence of security and bringing notable tips to analytics.

-

Digital wallets, regardless of fiat or crypto type, offer convenient and accelerated alternatives to the traditional payments by preserving data and presenting on-click transactions.

-

Efficient digital wallet development prioritizes robust security measures and compliance with regulations, including AML/KYC and GDPR.

-

The MVP launch and subsequent scaling of a digital wallet heavily rely on rigorous beta testing, comprehensive feedback collection, and data-driven analytics to promote product-market fit and continuous improvement.

What is a Digital Wallet, and How Does It Work?

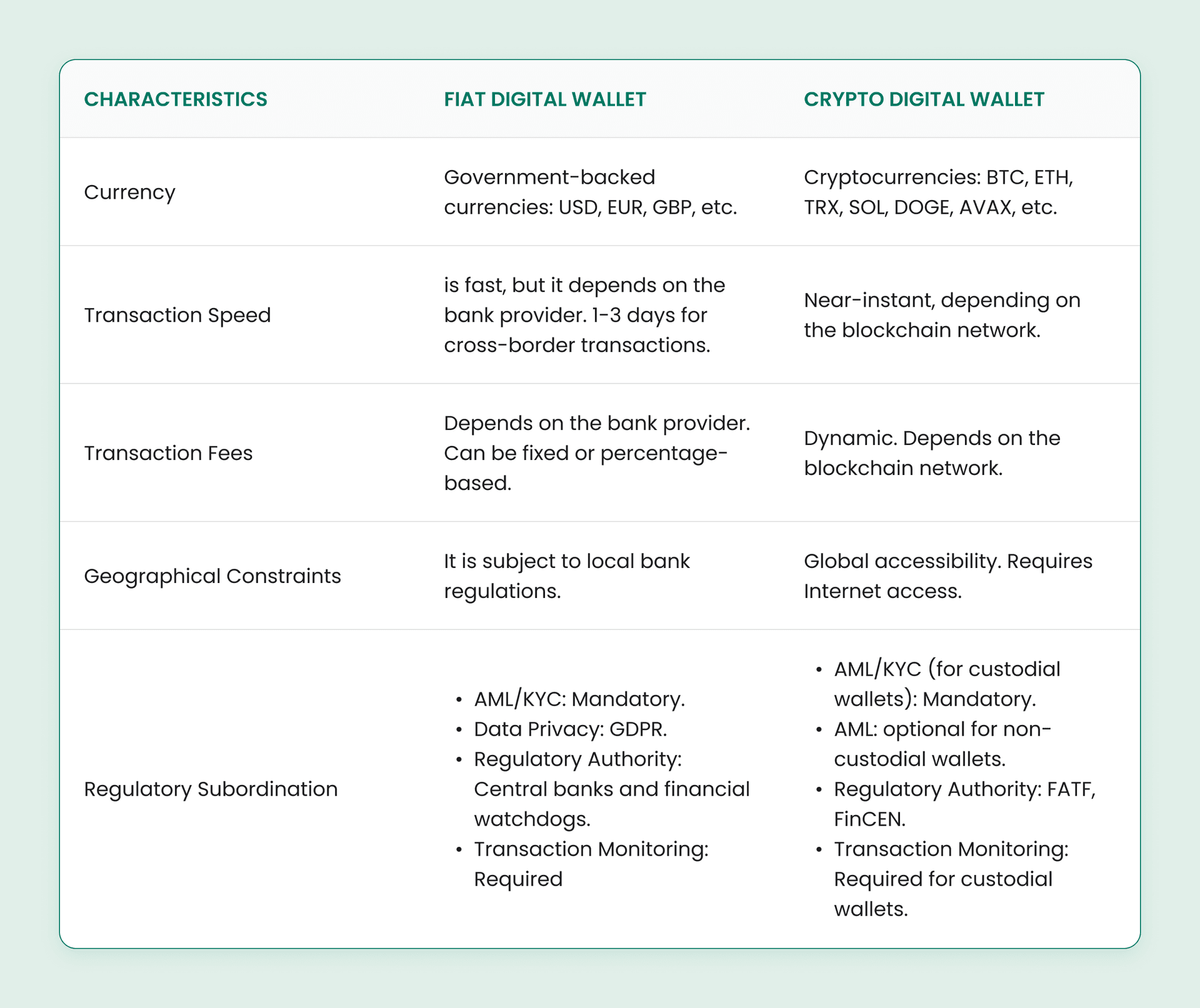

A digital wallet is a payment method that enables clients to make payments without presenting a physical card or fiat money. Instead, they securely store the client’s payment data to streamline real-world or web-based purchases. There are the following types of digital wallets: fiat and crypto wallets.

Fiat Digital Wallets

Fiat wallets operate via traditional currencies linked to the user’s bank account, such as Revolut, PayPal, Wise, etc. Here’s how the Fiat digital wallet works. The client tops up their wallet with funds from their card. They initiate the transaction through a web application. The provider settles the payment via the traditional banking rails. The balance status is updated in real-time after the transaction is completed.

Crypto Digital Wallets

Unlike fiat-operated wallets, cryptocurrency ones function within blockchain networks and hold crypto as the currency. There are two types of crypto digital wallets: custodial and non-custodial.

Custodial Wallet

In the custodial wallet (Kraken Wallet, Coinbase), the third party holds the client's private keys, stored on the centralized server. Although it requires less tech expertise, the clients can access their funds, yet they don’t control their private keys. However, it has recovery mechanisms to help users regain wallet access if they lose their private keys.

Non-Custodial Wallet

In the non-custodial wallets (MetaMask, Trust Wallet), the users have complete ownership of their private keys and funds and can run their transactions pseudonymously. Nevertheless, the non-custodial wallets don’t have recovery mechanisms. Once the private key is lost, the client won’t be able to access their wallet.

Explore the differences between custodial and non-custodial wallets.

Explore the differences between custodial and non-custodial wallets.

How to Create a Digital Wallet App Step-by-Step

Digital wallet app development is a complex and time-demanding process that requires an in-depth approach to planning the overall theoretical feature set, its practical engineering, and post-launch maintenance. Here is a list of the major steps in constructing a functional, efficient, and secure digital wallet.

Step 1 – Conduct Market and Competitor Research

Marketing and competitor research depend on decoding the key players in the market, their strong and weak points, and evaluating their marketing approaches and techniques for customer engagement and retention.

-

Competitor Analysis

Regardless of the feature set evaluation, competitor analysis will involve the identification of their security protocols and authentication methods, analysis of the user interface and functionality, assessment of their unique selling proposition, and evaluation of the technology stack used.

-

User Expectation

This sub-step collects data on user security concerns, preferred payment approaches, favored features, and pain points. These can be covered by conducting questionnaires and surveys, and setting up focus groups for discussion. User expectation analysis promotes better market fit and stimulates improved client adoption rates after the wallet launch.

Regional Requirements Analysis

Analyzing regional requirements is essential to creating a culturally fit product that reflects behavioral, technological, and regulatory elements. Evaluating preferred local payment methods, region-based interface peculiarities, and currency/exchange requirements can boost product adaptation to user expectations.

Step 2 – Define Product Goals and Required Features

At this stage, you need to determine the platform type and your monetization strategy.

Select the Platform Type

The Mobile Wallet: Is designed exclusively for mobile use, optimized for a touch interface, can include QR code payment support, and integrates payment features like NFC.

Web Wallet: This wallet type is better suited to desktop management and is accessible through a web browser. Web wallets can contain advanced reporting features.

Cross-Platform: this solution promotes the creation of bespoke applications, whether web, mobile, or both.

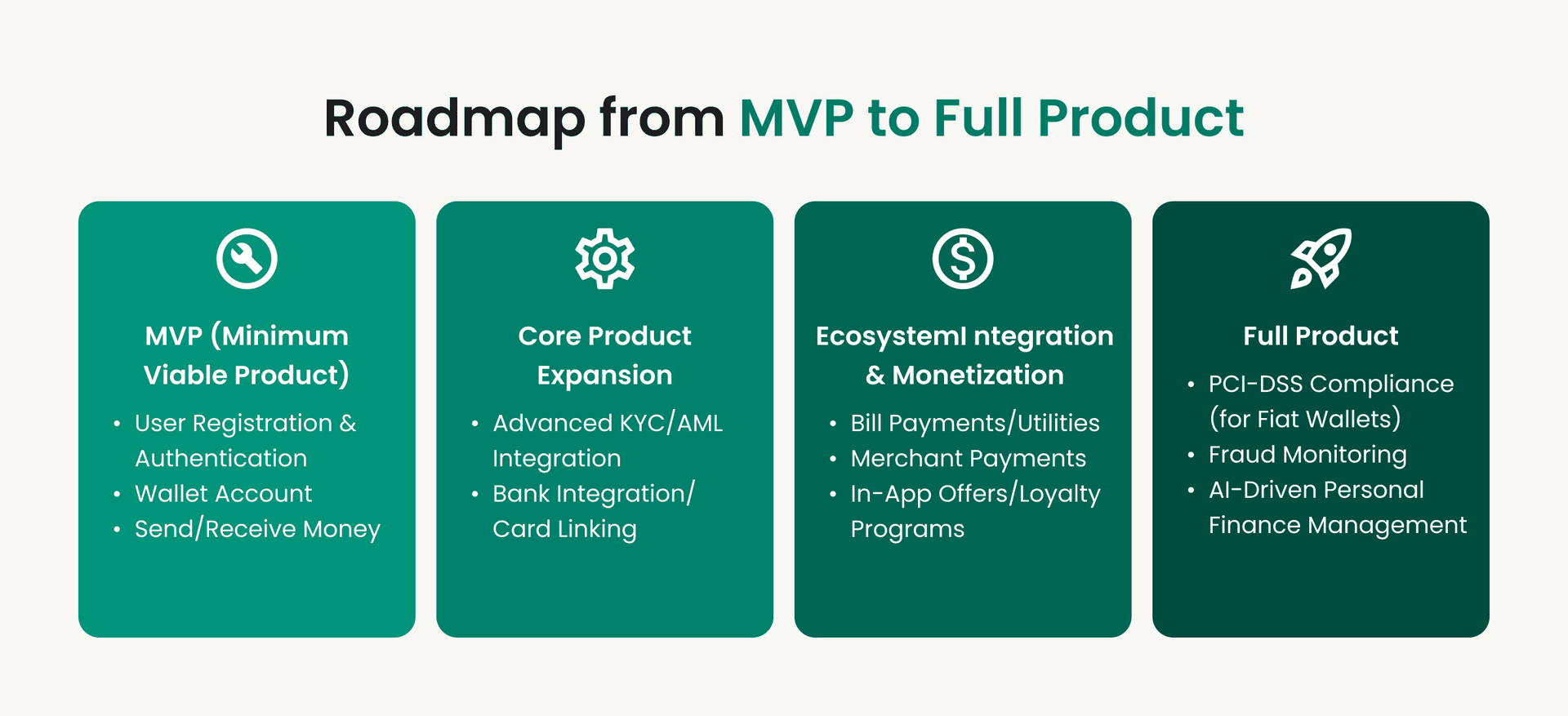

MVP vs Full Product

Note that when developing a digital wallet, you can start with an MVP or a full project, each of which will have a different time frame.

MVP: Or a minimum viable product will cover the aspects of basic registration, authentication, simple payment transaction capabilities, standard encryption protocols, basic fraud detection measures, standard send/receive functionality, and a simplified dashboard for balance analysis. The approximate development time will be 3-6 months.

Full Product: Will tailor the fully-fledged digital wallet version, maintaining advanced functionality, like multi-currency support, automated recurring payments, investment elements, multi-signature support, biometric authentication, advanced encryption methods, and real-time fraud detection, cross-border transaction abilities, third-party integrations, and AI-driven personal management. The development time is about 12-18 months.

Select Monetization Model

To bring an extra revenue layer, you can consider the following monetization strategies:

-

Transaction Fees

These can be percentage-based fees on transactions or fixed fees for a specific service. You can implement these through charges, for instant financial transfers or fees for premium services.

-

White-Label Solutions

This monetization model implies setting the license fees for platform use and integrating custom development charges. You can embody these based on the one-time setting costs.

-

Subscription

Digital wallets can be monetized through subscription thresholds, which the app can maintain through custom recurring payments. The basic tier can include a limited feature spectrum. The premium threshold can cover advanced elements. The enterprise tiers can incorporate customized elements.

Step 3 – Choose the Right Tech Stack

Technology stack plays a central role in developing an effective fiat or crypto digital wallet, as the combination of frameworks, programming languages, and infrastructures will affect each aspect of wallet architecture from UX design to security layer, etc.

Here is a short presentation on the importance of tech stack for security, blockchain integration, scalability, and user experience.

Security

The tech stack has to grant secure key management and robust encryption to keep crypto holdings safe and prevent a man-in-the-middle attack. If it comes to a fiat wallet, the tech stack has to maintain secure card data preservation.

Blockchain/Payment System Integration

The selected stack will determine the simplicity of scaling across chains and cryptocurrencies and affect the ability to customize wallet functions or transaction flows.

Scalability/Performance

Another essential factor that the tech stack will affect is scalability. As the transaction volume growth, the tech stack is important to promote a smooth scaling to minimize lags or downtime.

Step 4 – Design UI/UX for Trust and Ease-of-Use

Crafting a seamless UX/UI design is central to the digital wallet functionalities, as prioritizing the major features will promote better resource allocation, generating a decent user experience.

Fintech Design Principles

A simplistic yet well-organized layout with minimal clicks can:

-

Reduce cognitive load, as users don’t have to shift between multiple screens to perform the necessary actions.

-

Minimize the probabilities of errors during the transaction processes based on the clear hierarchy of information and actions.

The intuitive navigation has to make sure the elements work cohesively with minimized tech interruptions and within a clear hierarchical structure to minimize the perceptual load.

-

The visual hierarchy should display the frequently applied functions and keep secondary elements accessible for convenient use.

-

The standardized placement of the required elements, such as transfer buttons and balance display, preserves layout consistency.

-

Applying progressive showcasing can underline the digital wallet's advanced version by showing its sophisticated elements, but only when needed in order to avoid interface clutter.

The minimalistic color palette can promote brand recognition and enhance the digital wallet’s accessibility significantly.

A neutral color palette (blue, grey, white) for the background promotes cognitive effort simplification, boosting brand recognition and in-app functional intuitiveness.

Step 5 – Integrate Payment Gateways and APIs

This stage will cover the digital wallet's interoperability, funding, and withdrawal functions.

Fiat

Fiat payment gateways enable users to interact with their bank accounts and debit/credit cards. Let’s check the most prominent fiat payment gateways:

-

Stripe/PayPal

These payment gateways are suitable for performing top-up, withdrawal operations, and merchant payments. Stipe and PayPal are favorable options based on their global reach and relatively fast implementation.

-

Plaid

Plaid is beneficial for the Canadian and US markets. This payment gateway promotes a secure linkage with users' bank accounts. Plaid is a suitable option for the bank-to-wallet transfers.

-

Payoneer/Wise

These options suit perfectly wallets with cross-border payments due to the efficient handling of international transfers. Payoneer and Wise are the appropriate fiat payment gateways for freelancers who provide their services to international markets.

Crypto

The crypto wallet APIs, in particular, the blockchain integration, can significantly increase the wallet’s functionality within the Web3 and crypto economy.

-

WalletConnect

WalletConnect provides users with the ability to connect with external wallets, such as MetaMask, and promotes direct DeFi access within the application.

-

Coinbase API

Coinbase API is applied to the in-wallet portfolio display, purchasing, and crypto trading, and it empowers Coinbase’s regulated infrastructure.

-

Alchemy

Alchemy suits for engineering custom dApps and token-relevant experiences as it provides access to blockchain nodes and smart contract interaction.

-

Chainalysis KYT

It is essential for KYT compliance in crypto-relevant activities and helps identify suspicious activity.

Bank APIs (Open Banking)

These APIs promote secure access to client bank data.

-

Yodlee

It promotes financial data aggregation and risk scoring.

-

TrueLayer

TrueLayer promotes instant bank payment experiences. This bank API enables businesses of various segments to send/receive payments based on the open banking rails.

Currency Exchange APIs

Currency exchange APIs are applied to multi-currency and cross-border wallets due to the real-time conversion rates of crypto and fiat.

-

OpenExchangeRates

Promotes real-time foreign exchange rates for fiat money, providing a sophisticated feature such as ‘conversion before sending.’

-

CryptoCompare

It provides real-time prices and crypto-based exchange data. CryptoCompare is mostly suitable for investment tracking.

Step 6 – Implement KYC/AML Compliance

A reliable identity verification provider can boost digital wallet regulatory compliance and reliability.

Sumsub

Sumsub provides in-depth identity verification pertaining to both user identity analysis and streamlining the corporate flow of identity verification. With its decent coverage in global compliance, Sumsub incorporates ID, address, and non-doc verification, integrates face & liveness match, and known face search to guarantee the highest level of user identification and identity theft prevention.

Onfido

With its Atlas-powered orchestration platform, Onfido’s end-to-end solution provides robust, accelerated, and precise AI-driven identity verification. Onfido Studio enables businesses to craft tailored verification flows that abide by KYC, AML, and geographically specific regulations, routing through the fraud detection signals.

Jumio

Jumio has strong identity verification that spans the entire customer lifecycle - from ID verification and AML screening to selfies and liveness checks. Jumio’s automated onboarding empowers businesses to take action and make smart, real-time decisions based on the customer’s risk score.

The main steps for implementing AML/KYC compliance:

-

ID verification

The purpose of ID verification is to prove that the identity is legitimate by checking the user’s government-released document, such as an ID and driver’s license (issue/expiration date).

-

Liveness check

Liveness check aims to prevent user identity impersonation, so the client has to take a selfie or record a few-second video, where AI liveness detection systems will further decode mimic expressions and facial movements.

-

Proof of address

The purpose of checking the address is to ensure AML compliance and the digital wallet’s compliance with specific country laws. The user can integrate utility bills, where the system will check whether the name matches the one mentioned in the ID.

Role of KYT (Know Your Transaction) for Cryptocurrency

Unlike KYT’s focus on identity analysis, Know Your Transaction analyzes the practical transaction to spot and decode suspicious behavior within the transaction to determine the possibility of phishing. KYT will bring extra security to the digital crypto wallet, maximizing transaction security.

Storage/Private Data Processing (GDPR, CCPA)

To be a trusted custom digital wallet solution, it must ensure secure retention and processing of user data to avoid negative brand impact as mandated by GDPR and CCPA.

The General Data Protection Regulation represents a set of rules established by the European Union to limit data processing to specific purposes on behalf of clients, to let them make data alterations if needed.

CCPA, or California Consumer Privacy Act, obliges enterprises to increase user control over their personal data, especially to gain awareness of how enterprises utilize their data, as well as have the ability to delete info.

Step 7 – Add Core Functionalities

During this stage of digital wallet development, the IT professionals craft principal functionalities that will support financial activities within the application.

Top-Up Options

Any digital wallet has to provide users with the ability to deposit funds into their account. Let’s break down the core funding methods.

- ACH (Automated Clearing House)

Applied to the American context, ACH enables users to interlink their bank accounts to deposit funds; however, it requires connectivity with US-specific bank APIs such as Plaid or Yodlee. Mainly, ACH has low or no fees with an expected top-up time of 1-3 business days.

- SEPA (Single Euro Payments Area)

Managed by European banking systems or partners, such as TrueLayer, SEPA promotes euro transfers via 36 European countries. The transfer time is relatively instant, as the transfer is completed via the same or the next day.

- Cards (Visa, Mastercard, etc.)

This top-up option promotes near-instant funding using a debit or credit card. However, it charges higher fees, ranging from 2% to 4%, depending on the instant fund deposit.

- Crypto

With support for wallet addresses, crypto top-ups promote funding based on cryptocurrency transfers (BTC, ETH, etc.). The procedure time is nearly instant, around 5-30 minutes, with gas fees.

P2P Transfers

P2P transfers are one of the principal elements in the digital wallet, which supports user-to-user direct transfers through versatile approaches.

- Username

The username-based P2P transfers are simplistic and pseudonymous, as the user does not share their personal info, such as phone and email, yet can disclose their real user name.

- Phone Number

Perfect for address book synchronization, phone number-based P2P transfers use OTP verification or multifactor authentication to prevent identity impersonation.

- QR Code

With its scan-to-send and scan-to-receive functionality, the QR code payment process can contain the pre-filled amount or currency, which supports split-the-bill logic and is great for in-person payments.

Currency Exchange

Digital wallets can play the role of a so-called mini-exchange by offering the following capabilities:

- Internal Exchange (Fiat-to-Fiat)

Complying with AML/KYC for currency exchange, the internal exchange enables conversion between traditional currencies such as USD to EUR.

- DEX Integration (Crypto Swaps)

DEX integration promotes token swaps, such as ETH to USDT, based on the decentralized exchange, through aggregators like Uniswap SDKs.

Push Notifications

Push notifications help users stay informed about transaction-relevant processes and security status.

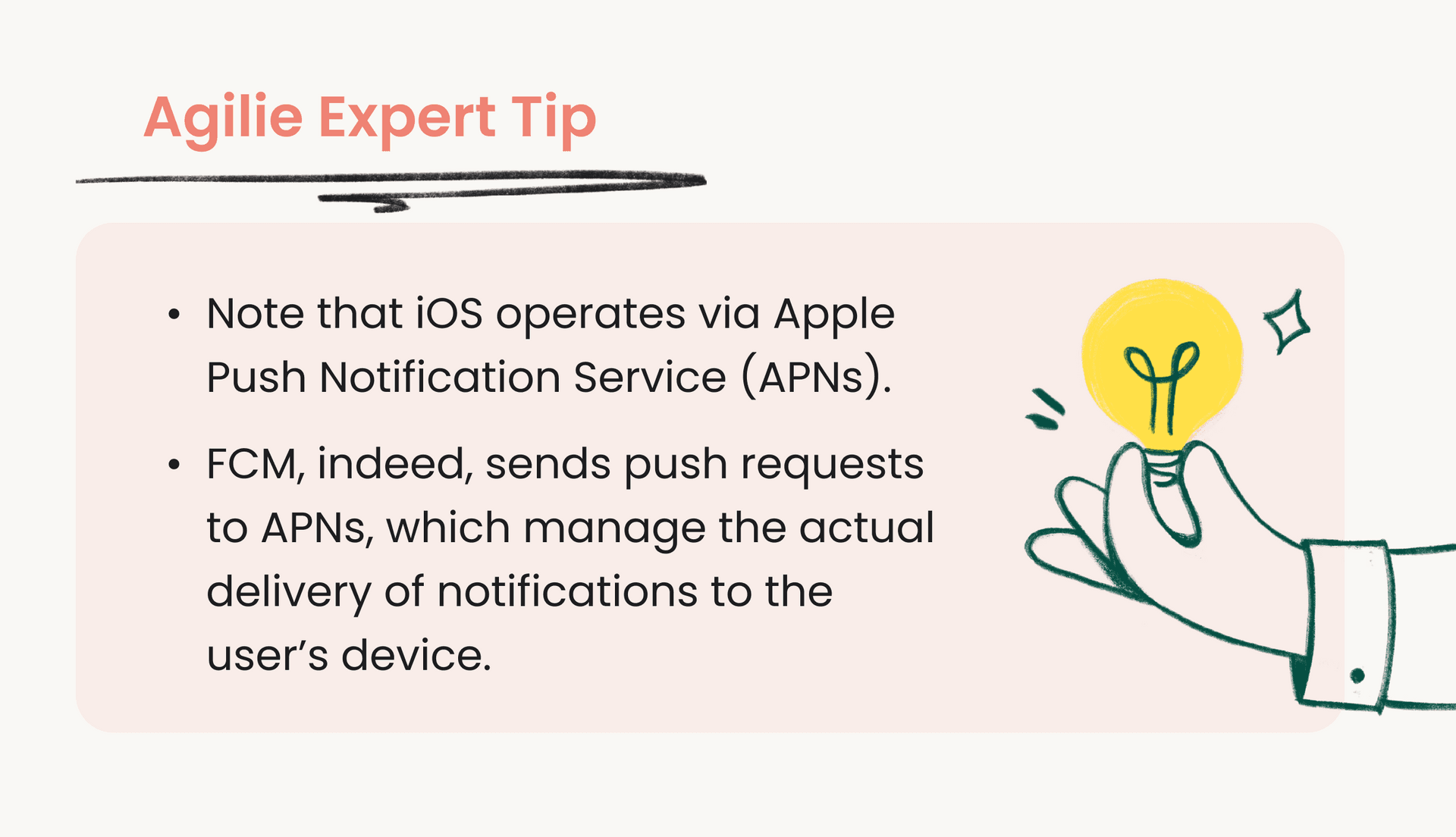

- Firebase Cloud Messaging (FCM)

As Google’s solution for Android and iOS (limited), FCM provides scalable and robust messaging for security alerts and transaction confirmation.

- OneSignal

OneSignal is a convenient push notification system that operates via behavioral triggers, such as a low balance reminder, and is convenient based on the multichannel notification support. The client can be informed via push, SMS, and email.

Transaction History

Transaction history is a journal-like presentation of the user’s spending behavior, which can help them track their expenses. The essential sub-elements of transaction history include:

-

Categories (based on interlinking the spent item to the wallet’s embedded auto-tags, such as ‘Transport, ‘Bills,’ etc.).

-

Tags (user-based labels, such as ‘#business,’ ‘#vacation’).

-

Filters and search (category, date, sender, etc.).

-

Receipts (ability to attach receipts).

Step 8 – Implement Security Measures

Implementing bank-level security measures is essential to proving the reliability and trustworthiness of the digital wallet’s safety. Below is a list of some of the security approaches.

-

Data Encryption

AES-256 or Advanced Encryption Standard with a 256-bit key length is one of the strongest symmetric encryption algorithms that ciphers personal data, wallet balances, and transaction records in transit and at rest.

As protocols for protecting data transmission over the Internet, Secure Socket Layer / Transport Layer Security imply that all API and third-party integrations have to use HTTPS, TLS 1.2 or higher.

-

Secure Key Storage

HSM or Hardware Security Module is a hardware device used for the storage, creation, and management of cryptographic keys. One of the critical advantages of HSM is its tamper-resistance, making it a suitable option for enterprise-level wallets.

AWS KMS is a cloud-based key management system that supports encryption key rotation and policy-based access.

-

HashiCorp Vault

HashiCorp Vault is an identity-based secrets management tool to authenticate and authorize access to secrets and other sensitive data. It stores API keys and encryption keys in a secure and centralized vault and can be applied to enterprise-grade wallets.

-

Biometric Authentication

Integrate biometric authentication as an additional option for promoting the digital wallet’s security. Face ID/Touch ID (iOS) and BiometricPrompt (Android) can be applied to authenticate into the wallet and confirm transactions by minimizing the risks of identity impersonation.

-

Multifactor Authentication

Multifactor authentication boosts the digital wallet’s security based on two methods of identity verification, including factors like something the client knows (pins), something they have (device), and something they are (biometrics). Multifactor authentication can implement time-based OTP, email OTP, or SMS to authenticate into the digital wallet securely.

-

Fraud Detection Modules

Rule-based systems apply a set of prewritten rules to render decisions relevant to problem-solving. For instance, if an unusually large withdrawal or high-frequency transfers occur, the rule-based system triggers alerts as the pre-set thresholds are breached. Another example is an account freeze based on repeated failed attempts to log in.

Machine Learning Models evaluate users’ behavior in real-time by flagging anomalies, such as location or transaction size, that help detect suspicious activities.

-

Session & Device Management

Monitoring client sessions can increase the security of digital wallets by invalidating them after suspicious activities. Token rotation can be implemented as a preventive measure against replay attacks.

Device fingerprinting can help detect and respond to unfamiliar logins, such as sending alert notifications or requiring reauthentication when a new device is detected.

Source: Business Perspectives.

Step 9 – MVP Launch & Scale

The MVP launch phase focuses on delivering a well-functioning production-grade digital wallet on the market to validate its customer-product fit. The MVP launch phase includes beta testing and feedback collection. The scaling phase will focus on further product development and adding new features.

-

Beta Testing

Beta testing is crucial for further feedback collection as it will touch on the elements of the digital wallet’s functionality, UX/UI intuitiveness, and security. TestFlight is an official platform for beta testing designed to distribute pre-released products on iOS. Google Play Beta enables developers to configure open or closed testing tracks by using the Google Play Console. Beta testing enables developers to get feedback on the digital wallet’s functionality, excluding extensive public exposure.

-

Feedback Collection

Hotjar is an essential tool for Web/PWA MVPs' feedback evaluation, as it checks behavioral analytics by offering session recording, heatmaps, and in-app surveys. Hotjar is mostly suited to collecting UX feedback by analyzing frustration points, such as rage clicks, and initiating a micro-survey after the client uses the feature.

Amplitude is used for mobile and web assessments of user journeys and feature adoption, including retention assessments and onboarding cycles.

-

Setting Up Analytics

Apply Mixpanel and Firebase to scale digital wallet development. Mixpanel focuses on analyzing clients' actions and app-relevant behavior. This event-based analytics tool analyzes clients' specific actions, their frequency, and order.

Integrate Mixpanel to streamline onboarding. Identify friction points when assessing the onboarding process. This can help decode unnecessary elements, such as an abundance of onboarding steps, and prevent clients from dropping off.

Firebase, or specifically, Firebase Analytics, provides an encompassing analysis of application performance and client engagement. Apply this analytics tool to address crashes and performance bottlenecks. Intertwine Firebase Analytics and Google Ads to boost marketing campaigns and check user engagement.

Step 10 – Post-Launch Growth & Feature Expansion

The final step of digital wallet app development is considering its further extension. This can include expanding functionality by adding new currencies, scaling with new markets, and continuous monitoring to check on the product’s growth.

Partnering with a Fintech App Development Company

Digital wallet app development requires considerable financial input, which motivates enterprise representatives to search for options for optimizing resource allocation while preserving the highest quality of the application. Fintech development outsourcing represents such an option by presenting the following benefits:

-

Minimized overhead.

-

Reduced prices for narrowly specialized services (as compared to the local IT market).

-

Access to proficient IT talents all over the world.

-

Access to top-tier technologies (the outsourcing company provides the team with all the required tech stack).

Why Choose Agilie

Agilie is a pioneer software development company that can be an indispensable partner in your digital wallet development process. Result-oriented, we are committed to the security and quality of any bespoke digital solution or web service.

With a complete SDLC, Agilie engineers custom software options within fintech, payment processing, blockchain technologies, and mobile banking domains. Focusing on the iterative development process, our dedicated developers are flexible to time-sensitive alterations, crafting the highest quality product afterward.

Focusing on three models of outsourcing: dedicated team, staff augmentation, and project-based outsourcing, Agilie can help you construct a top-tier digital wallet due to the following services:

Chameleon Pay

Agilie worked on Chameleon Pay, a digital crypto wallet that provides users with the ability to perform versatile crypto manipulations: buying, selling, exchanging, etc. One of the challenges we encountered was approaching the variable blockchain network, as each had its own data structure, transaction signing specificity, and key generation. Our dedicated developers engineered a solution in blockchain network universification, which involved the design patterns (adapter, decorator, etc.) and describing universal interfaces and abstract classes.

Another challenge was to provide the highest level of private keys and passwords. The app uses the Advanced Encryption Standard technology to implement encryption as the keys are stored and encrypted on the device. The decryption emerges only in the case that the user has to sign the transaction, which requires them to insert the password. The SHA256 algorithm is applied to check the password’s correctness. Additionally, to bring an extra layer of key/password safety, we integrated the function of blocking access to online wallets by TouchID and FaceID.

Summary

Digital wallet app development is a long-term investment in an innovative product that expands the business reach of tech-savvy consumers. Whether it’s fiat or crypto type, you have to keep in mind its step-by-step development process to prioritize the essential features from the beginning to produce notable deliverables by the post-launch expansion phase. Finally, don’t forget about cooperating with dedicated developers to craft a bespoke, cost-effective, and efficient digital wallet.

Transform your vision into a custom digital wallet with Agilie!

Transform your vision into a custom digital wallet with Agilie!